2nd Quarter 2020 Shareholder Newsletter

Unprecedented. It is an often-used word these days. The Cambridge Dictionary defines “unprecedented” as something never having happened or existed in the past. While we believe the word “unprecedented” is overused, it is also the appropriate word to describe the last four months. The crisis we experienced beginning in March is truly unprecedented. We have never experienced a global pandemic of this magnitude. We have never seen the government shut down entire industries, causing the most rapid economic decline in our country’s history.

Parkside entered 2020 expecting a slight economic slowdown but still projecting $8 million in net income, $500 thousand more than we earned in 2019. We began the year with excellent capital levels, strong loan loss reserves and robust core earnings. Then, the world changed. COVID-19 hit and the economic outlook deteriorated virtually overnight. Even the most optimistic prognosticators do not see the U.S. economy getting back to late 2019 levels for at least a couple years. The most pessimistic economists speak of a much grimmer outlook, one akin to The Great Depression. Experience tells me reality will most likely be somewhere between these two extremes.

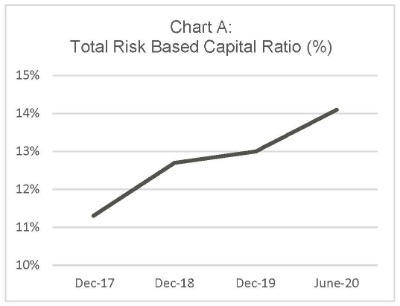

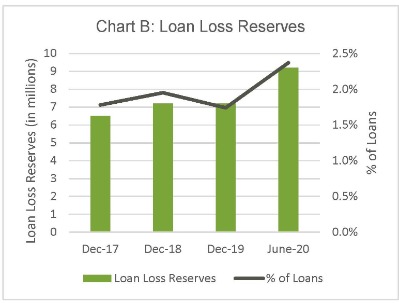

Our own economic outlook is no more clairvoyant than anyone else’s – which means we do not know either. What does all that mean for Parkside? It means we prepare for the worst, while positioning your company to continue expanding its client base and building long-term value.First, we built our capital and loan loss reserves to all-time highs. Our balance sheet has never been stronger and more capable of handling the unknown; everything from a severe downturn with increased loan losses to a strong rebound resulting in unusually rapid loan and client growth. Either way, we are ready. Charts A and B show how we further strengthened our balance sheet to prepare for the uncertainty ahead.

Chart A illustrates how we increased our total risk-based capital to above 14%, a record high for Parkside, nearly 50% above levels considered well-capitalized by the regulators.

Chart A illustrates how we increased our total risk-based capital to above 14%, a record high for Parkside, nearly 50% above levels considered well-capitalized by the regulators.  Chart B illustrates the rapid increase in loan loss reserves to record highs from both a dollar and percentage of loans perspective, providing a substantial cushion to absorb potential future loan losses.

Chart B illustrates the rapid increase in loan loss reserves to record highs from both a dollar and percentage of loans perspective, providing a substantial cushion to absorb potential future loan losses. Expanding Our Team

With so many talented individuals out of work, or re-evaluating career opportunities, Parkside considers this an opportunity to recruit valuable, top-tier team members. Therefore, we accelerated our hiring plans by recruiting for positions originally planned as hires for late 2020 and 2021. Expanding our team now will ensure we have the capacity to serve existing clients who may require extra attention during these challenging times, while also continuing to add new relationships with those who may not be receiving the attention they deserve from their current financial providers. Either way, the extra support will be well-utilized helping clients and creating value for our shareholders.

Performance Outlook

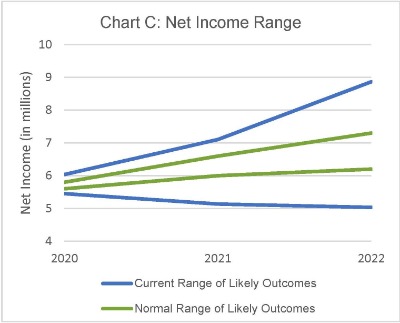

At past annual shareholder meetings we provided high-level earnings guidance for future years. We

were able to do this because we were confident in our ability to provide net income forecasts within a tight range of likely outcomes. Nothing was guaranteed; however, the odds of achieving results close to those forecasts were reasonably high. Unfortunately, we are not afforded that certainty today. The range of possible outcomes is much wider. Chart C provides an illustration of the gap between our historical and current confidence levels for future profitability, whereby the green lines represent our historic range of likely outcomes and the blues lines represent our currently predicted range of future outcomes.

were able to do this because we were confident in our ability to provide net income forecasts within a tight range of likely outcomes. Nothing was guaranteed; however, the odds of achieving results close to those forecasts were reasonably high. Unfortunately, we are not afforded that certainty today. The range of possible outcomes is much wider. Chart C provides an illustration of the gap between our historical and current confidence levels for future profitability, whereby the green lines represent our historic range of likely outcomes and the blues lines represent our currently predicted range of future outcomes.

We believe, barring another extreme market disrupter, we will perform somewhere in the area between the blue bars on the chart, with 2020 net income slightly above $5 million to slightly below $6 million. The range of possible net income outcomes becomes wider in subsequent years with the extremes very far apart by 2022. We also believe there is an equal probability we produce net income results near the high end or low end of the range depicted by the blue lines in Chart C. The primary inputs creating the variance in outcomes are the economic forecasts and related loan losses, loan growth, the interest rate environment and the behavior of the stock market and associated revenue generated in our Trust and Family Office division.

Due to the unusually wide range of possible outcomes, it is difficult to determine an appropriate price for our 2020 stock repurchase program. Therefore, we will not offer a stock repurchase program in 2020. We hope to have more clarity and less variability of possible outcomes by early 2021. This would allow us to resume the stock repurchase program in 2021.

There have been a few stock trades in recent months as indicated in the included Financial Summary. Not surprisingly, the price of our stock has declined from the yearend 2019 high of $38 per share. All bank stocks have declined this year as the outlook for the banking industry earnings was downgraded due to the deteriorating economic outlook. Regional bank stocks have declined 35% year-to-date as indicated by the KBW regional bank stock index. We are pleased Parkside stock has only dropped 10-20%. As indicated earlier in Chart C, our own outlook reflects the same uncertainty the entire industry is experiencing.Highlighted above and linked below are our year-to-date financial results. Assets continued to remain inflated through June, ending the month at $660 million, an increase of $155 million from a year ago. We funded $71 million in SBA guaranteed PPP loans as part of the CARES Act stimulus program. Many clients used these loan proceeds to repay outstanding lines of credit, reducing 2020 commercial loan growth by approximately $35 million. With so much liquidity in the system, deposit growth is exceptionally strong with total deposits of $532 million at month end June, a $134 million increase from June 2019. We estimate approximately $75 million of the increase is temporary, due to the stimulus related excess liquidity. Commercial loan growth continues to be a struggle as our commercial clients are reducing their line of credit usage and new loan originations have slowed with the COVID-19 lockdown. We believe this trend will continue into 2021, negatively affecting loan growth and net interest income.

Year-to-date net interest income of $9.3 million is slightly ahead of June 2019 year-to-date net interest income. In June 2020, we earned $1.8 million in loan fees on the $71 million in SBA PPP loans, an unusually large amount. We normally earn $55-60 thousand per month in loan fees. Adjusting for the June one-time PPP loan fees, YTD net interest income would have declined compared to YTD June 2019. The decline is due to two factors. First, the Federal Reserve lowered interest rates to 0% with the onset of the COVID-19 pandemic. Lower interest rates put downward pressure on our net interest margin. Second, the reduced commercial line of credit usage means fewer outstanding loans, which in turn results in less interest earned on loans and lower net interest margin.

Year-to-date noninterest income of $4.6 million is $633 thousand more than YTD June 2019. This is helping offset some of the impact of lower net interest income. As noted earlier, we also put $1.8 million into loan loss reserves on top of the $271 thousand recovery in the first six months of 2020, building our loan loss reserve to $9.2 million in preparation for a possible COVID-19 related economic downturn.

Year-to-date noninterest expense of $8 million reflects an increase of $384 thousand, or 5%, compared to YTD June 2019. We expect noninterest expense to increase in the second half of 2020 as we continue investing in our future by upgrading our core processing system in July and investing in additional personnel.

The bottom line – we earned $3.4 million in net income in the first six months of 2020, $290 thousand less than we earned in the first six months of 2019. As noted above, we expect net income in the second half of 2020 to be less than the first half and to remain low compared to 2018 and 2019 levels for well into 2021 due to the low level of interest rates, slower commercial loan growth and uncertain economic outlook.

In Closing

We appreciate your support during this challenging time, and look forward to working with you as we navigate what's ahead.

Should you have any questions or comments, please feel free to contact us. Stay safe and healthy.Sincerely,

James C. Wagner - CEO

Andrew S. Hereford - President, Bank

Matthew A. Wagner - President, TFO