Monthly Market Update | September 2025

September 2025

Monthly Market Update

Macro Update

-

-

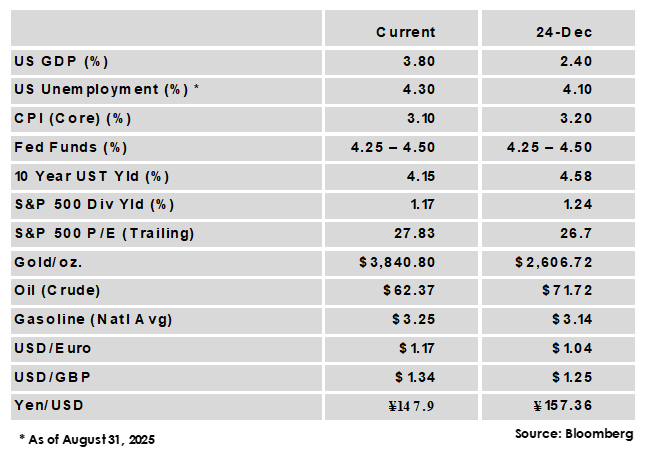

The United States economy grew at a faster pace than earlier thought in the 2nd quarter, expanding at a 3.8% annualized rate, well above the initial 3% estimate.

-

The FOMC made its first policy rate change of 2025 when it lowered the Federal Funds target rate by 25 bps to a range of 4.00% - 4.25%. The committee’s updated dot plot of interest rate forecasts gave guidance for two additional cuts in 2025, one more than in the prior dot plot.

-

The labor market continued to slow in August as the unemployment rate ticked higher to 4.3% and nonfarm payrolls increased by just 22,000 for the month.

-

Inflation remains stuck well above the Fed’s 2% target, with both core CPI and core PCE holding steady at 3.1% and 2.9%, respectively. Overall, inflation’s rise in recent months has not been as severe as feared given the sharp increase in tariffs, giving the Fed room to cut interest rates for now.

-

A government shutdown began as the month ended, the first since 2019. Historically, government shutdowns have had limited impact on financial markets as they rarely last long, but this one could impact the availability of key government data like the monthly jobs report as the Fed considers an October rate cut.

-

Global Equity

-

-

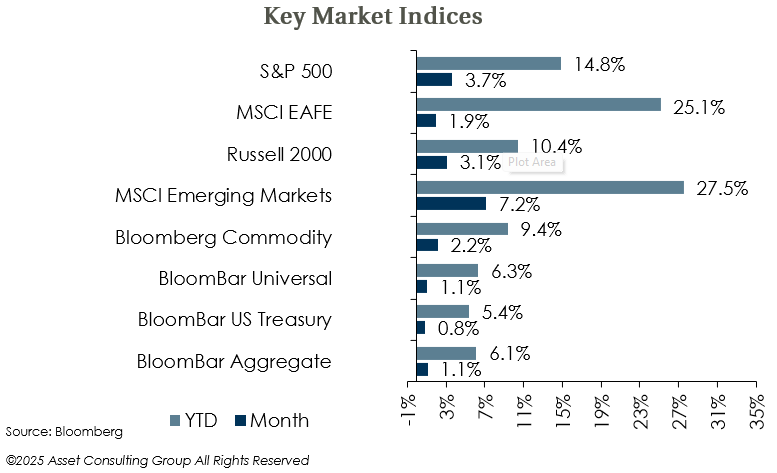

Equities rose in September as solid earnings and central bank policy easing helped sustain the recent rally. The emerging markets index was the top performer, supported by strong returns from Chinese equities where export resilience and higher levels of share buybacks have fueled excellent 2025 performance.

-

Final reported 2Q earnings growth for the S&P 500 was 11.7%, the 3rd consecutive quarter of double-digit growth. Current estimates for 3rd quarter growth are somewhat lower but still solid at 7.9%. Currency impact was muted in September but has been a significant contributor to non-US performance in 2025.

-

AI spending has been a key contributor to US growth, with several more multi-billion dollar deals among AI providers, chipmakers, and data center operators announced in the month. However, this has also raised some concerns about the sustainability of such spending and intensified calls of a bubble in the AI market.

-

Global Fixed Income

-

-

US treasury yields were mostly lower in September as the Fed carried out its widely expected rate cut, and the labor market continued to show weakness.

-

Market based rate forecasts are anticipating two more Fed rate cuts in 2025 and a Fed Funds rate near 3% by the middle of next year. Meanwhile, the Bank of England and European Central Bank held rates steady at their September meetings with the timing of additional cuts uncertain.

-

Investment grade and high yield spreads both tightened in the month, and while spreads remain near all-time lows, total income remains attractive. Cash yields look set to fall with high odds of continued rate cutting in 2025, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate delivered another quarter of positive returns; however, the return was comprised almost entirely of income as price appreciation was flat. All property sectors gained for the second consecutive quarter.

-

Commercial real estate seems to have stabilized overall even as office vacancy rates remain elevated. A resumption of Fed rate cutting could act as a catalyst for transaction volume and price appreciation.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.