Monthly Market Update | September 2023

September 2023

Monthly Market Update

Macro Update

-

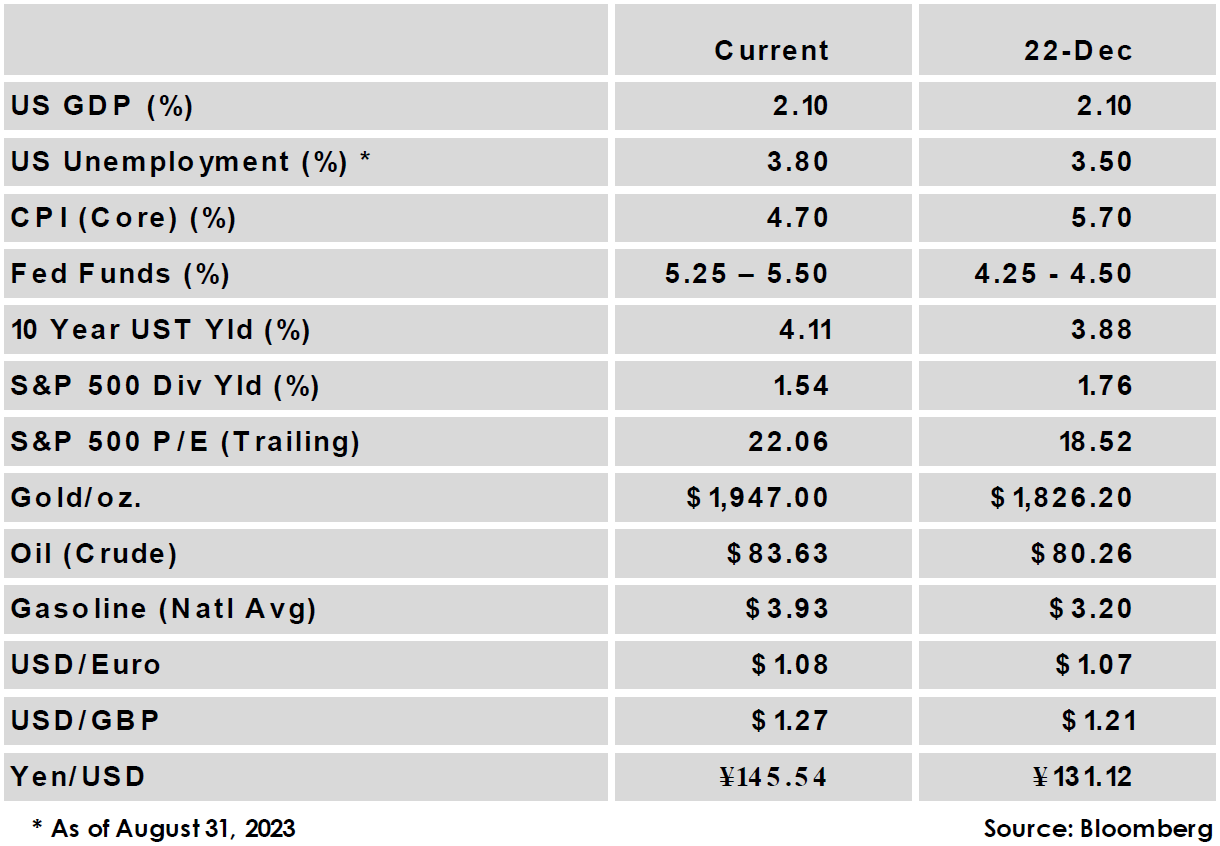

- A hawkish Fed weighed on markets in September. While the target rate remained unchanged at 5.25% - 5.50%, the decision was accompanied by upward revisions for growth forecasts and a reiteration of the Fed’s ‘higher-for-longer’ messaging, which sent Treasury yields higher and stock markets lower.

- Higher oil prices stemming from recent OPEC+ production cuts have also hurt sentiment, as rising gas prices pressure consumer spending and contribute upside risk to inflation.

- Headline inflation surprised to the upside with its largest monthly gain of the year, fed by higher energy prices. Core CPI still eased with the year-over-year change falling from 4.7% to 4.3% while core PCE, the Fed’s preferred gauge, declined to a 3.9% annual rate after its smallest monthly increase since 2020.

- The US government narrowly avoided a shutdown with a last-minute deal to fund the government. However, that potential economic headwind was only delayed for now, with the deal extending funding to November 17th.

- A hawkish Fed weighed on markets in September. While the target rate remained unchanged at 5.25% - 5.50%, the decision was accompanied by upward revisions for growth forecasts and a reiteration of the Fed’s ‘higher-for-longer’ messaging, which sent Treasury yields higher and stock markets lower.

Global Equity

-

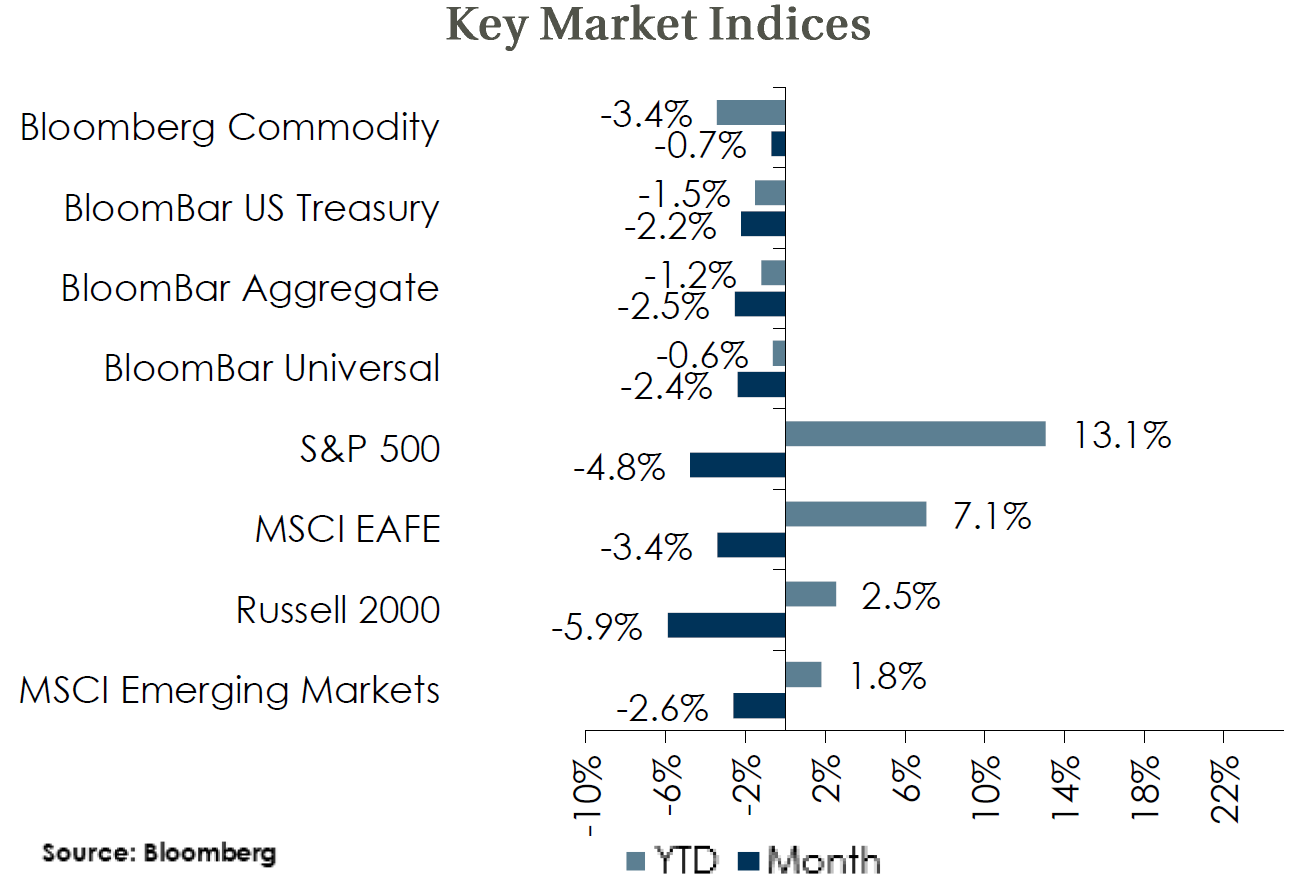

- Higher rate expectations, rising oil prices, and uncertainty over the UAW strike and government shutdown combined to drag equities to their worst month of the year.

- Valuations on forward earnings declined and are now very near their averages across equity indices, with the exception of US large caps where valuations remain elevated.

- US dollar strength reemerged as a headwind for Non-US equity, with USD returns trailing their local currency counterpart by over 200 bps in September for developed markets. The possibility of an additional hike from the Fed could limit currency tailwinds for non-US equities in the near-term.

- Higher rate expectations, rising oil prices, and uncertainty over the UAW strike and government shutdown combined to drag equities to their worst month of the year.

Global Fixed Income

-

- US Treasury yields rose sharply across the curve in response to a hawkish Fed and higher than expected inflation, with the 10-yr UST yield rising 46 bps to its highest level in 16 years.

- Sovereign yields moved higher around the world. While central bank rates are thought to be near their peak, investors have come around to the idea that rates could remain high for some time. The ECB raised its rate but signaled that the hike was likely the last, while the Bank of England paused after 14 straight hikes.

- Credit spreads rose in September, with investment grade rising 3 bps and high yield 22 bps higher, though both measures remain well below their averages.

- US Treasury yields rose sharply across the curve in response to a hawkish Fed and higher than expected inflation, with the 10-yr UST yield rising 46 bps to its highest level in 16 years.

Global Real Estate

-

- Core real estate returns delivered a third consecutive quarter of negative returns in Q2, while the appreciation component of returns had its fourth consecutive negative quarter.

- Real estate returns could continue to be challenged amid higher interest rates, tighter lending conditions, and reduced demand for office space.

- Core real estate returns delivered a third consecutive quarter of negative returns in Q2, while the appreciation component of returns had its fourth consecutive negative quarter.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.