Monthly Market Update | October 2022

October 2022

Monthly Market Update

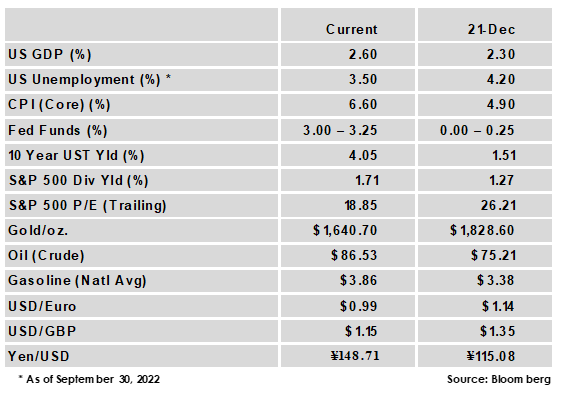

Stocks rallied in October as investors wagered the Fed would begin to slow the aggressive pace of interest rate hikes following an expected 75 bps hike at the early November meeting. The shift in expectations for a Fed pivot came even as inflation continued to surprise to the upside, as Core CPI rose to 6.6%, a new high for the cycle.

The labor market also remained strong, with unemployment falling back to 3.5%. Wage growth moderated slightly but remains well above pre-pandemic levels. US GDP grew at a better than expected 2.6% annual rate following two straight negative quarters, with much of the growth due to a narrowing trade deficit. The underlying data, however, showed some weakness in key areas, with consumer spending slowing and private investment contracting.

The midterm elections will command attention in November, but the outlook for fed policy and key data, such as inflation and labor market strength, will likely be the main drivers of markets. The Fed’s upcoming rate decision is unlikely to surprise, so post-meeting remarks from Fed officials will be closely monitored for hints at future policy.

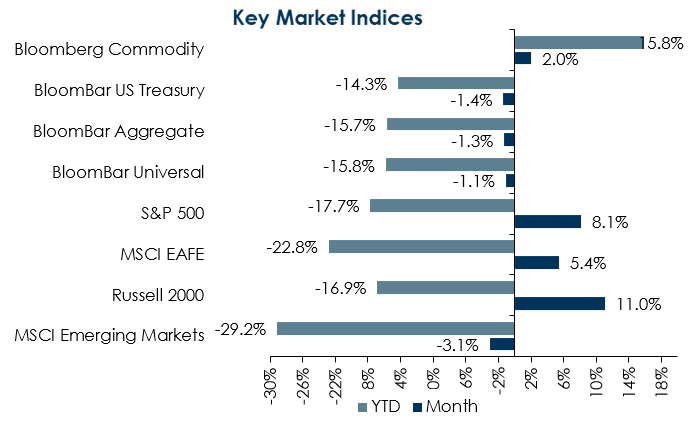

- Global Equity – Most equity markets rebounded off September lows, led by US markets. Emerging markets lagged with negative returns, weighed down by China as markets reacted negatively to President Xi’s tightening grip on power. Index level P/E multiples on forward earnings followed returns, as EM valuations moved lower while other regions moved higher, with US large cap moving narrowly above its historical average. Earnings outlooks continued to soften, but a better than feared start to the 3rd quarter earnings season helped lift markets in October, although the number and magnitude of positive surprises is still below recent averages. Equity market volatility is likely to continue given central bank policy uncertainty, geopolitical conflict, and China’s growth slowdown. Valuations are supportive, but below trend growth and the potential for further downward revisions could limit near-term equity upside.

- Global Fixed Income – Global bond yields were mixed in October, with US rates rising following higher than expected inflation. Interest rate volatility remains elevated, and liquidity has become increasingly constrained, with both approaching levels last seen in March 2020. Maintaining financial stability could influence Fed policy in the coming months, but for now the Fed remains focused on inflation, with another 75 bps hike widely expected. High Yield credit spreads tightened 88 bps to fall below historical averages while IG spreads were flat. An approaching end to the Fed tightening cycle will help limit additional duration downside, and higher yields have improved the outlook for core bonds going forward. Spreads could widen in a recession scenario but strong corporate balance sheets should soften the impact to credit of a growth slowdown. Volatility in rates and currency should provide enhanced opportunities for absolute return strategies, which can also offer downside protection. A cash allocation provides portfolio flexibility while rising front-end yields have improved the asset’s return potential.

- Global Real Assets & Private Markets – Core real estate returns cooled significantly from recent quarterly performance, but maintained a modestly positive return. In a change, Hotels replaced Industrials as the top performing sector in the quarter, and Office was the only sector with negative performance. New deal activity in private equity continues to slow from 2021’s elevated rate but overall remains at healthy levels. The broad commodities index had a positive return in October as an OPEC+ production cut and Russia’s threat to withdraw from the Black Sea Grain Initiative helped put upward pressure on prices. Core CPI rose +6.6% year-over-year, again exceeding expectations and accelerating from last month’s level of 6.3%. Measures of future inflation expectations were sharply higher in a reversal of last month’s decline, with the 10-year inflation breakeven up 36 bps to 2.51%.

|

|

Disclosures and Legal Notice | © 2022 Asset Consulting Group. All Rights Reserved.