Monthly Market Update | October 2025

October 2025

Monthly Market Update

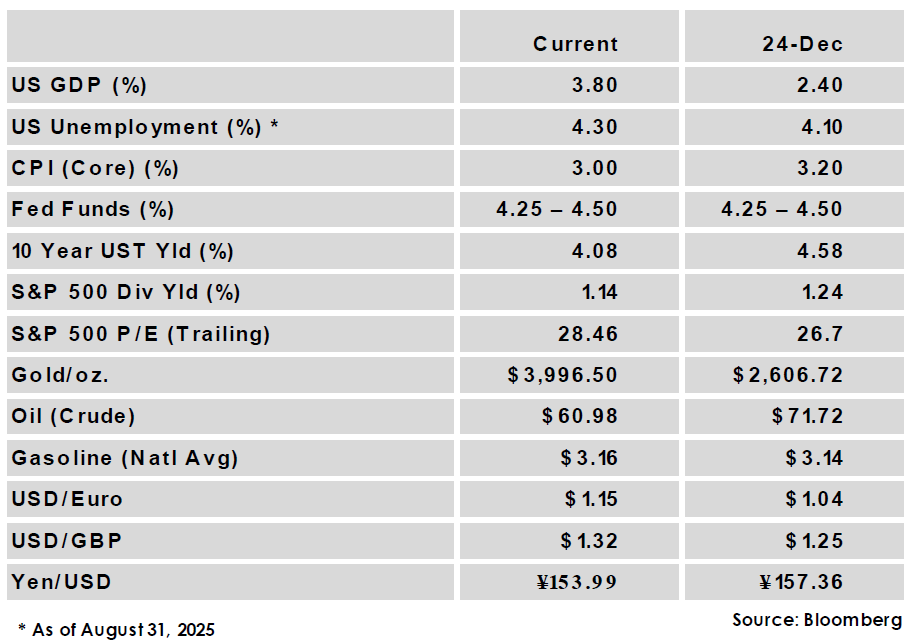

Macro Update

-

-

The US government shutdown continued through the month, and while signs of decay in consumer sentiment have begun, financial markets have largely ignored the impasse for now.

-

The FOMC made its second consecutive rate cut in October when it lowered the Federal Funds target rate by 25 bps to a range of 3.75% - 4.00%. Fed chair Powell’s post meeting remarks leaned hawkish, and market expectations for another cut before year-end have declined.

-

Data was limited in the month due to the government shutdown, and there was no labor market report. CPI was an exception due to its use in calculating Social Security payments, and the report showed inflation rose slightly to remain well above the Fed’s 2% target, with CPI rising from 2.9% to 3.0%.

-

On-and-off trade tensions between the US and China appeared to ease notably in October after a face-to-face meeting between Trump and Xi. An ensuing agreement eased US tariffs on Chinese goods in exchange for a crackdown on fentanyl producing chemicals and an easing of rare earth exports.

-

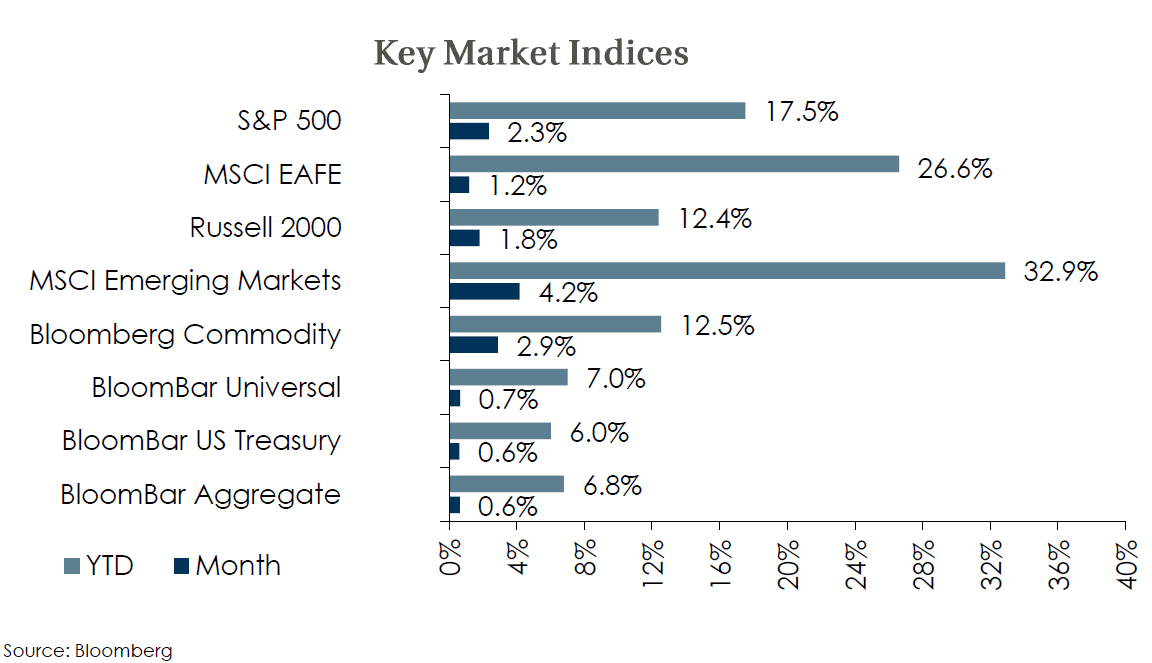

Global Equity

-

-

Global equities were mostly positive in October as momentum from the AI trade continued and the third quarter earnings season got off to a strong start.

-

While earnings continue to be solid, elevated valuations suggest strong growth expectations are already largely priced in, leaving markets vulnerable to correction if high expectations are not met.

-

AI spending has been a key contributor to US growth, and third quarter earnings results have included guidance for even higher spending on the AI buildout. However, investor reaction to these reports was somewhat mixed as questions grew about the availability of revenue to cover such extravagant spending.

-

Global Fixed Income

-

-

US treasury yields fell across the curve in October as the Fed carried out a second consecutive rate cut. Yields reversed some of their decline following hawkish Fed remarks and the 10-year US treasury yield finished just 7 bps lower for the month.

-

Market based forecasts still anticipate a December rate cut, but the odds have declined, while forecasts call for about three more total cuts by year-end 2026. The FOMC also decided to end its quantitative tightening program as of Dec. 1, ending balance sheet normalization that began in mid-2022.

-

Credit spreads widened modestly in October, and while spreads remain near all-time lows, total income remains attractive. Cash yields look set to fall if rate cuts continue as expected, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate returns were positive for a 5th consecutive quarter. Returns were broad-based as all property sectors were positive in the quarter, however the return remains largely income based as property price appreciation was again flat.

-

Property transaction volume has improved, and the office sector appears to have passed through its trough. Economic uncertainty around tariffs and job growth could impact dealmaking, but additional rate cutting in 2026 would be a positive for the real estate sector.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.