Monthly Market Update | October 2023

October 2023

Monthly Market Update

Macro Update

-

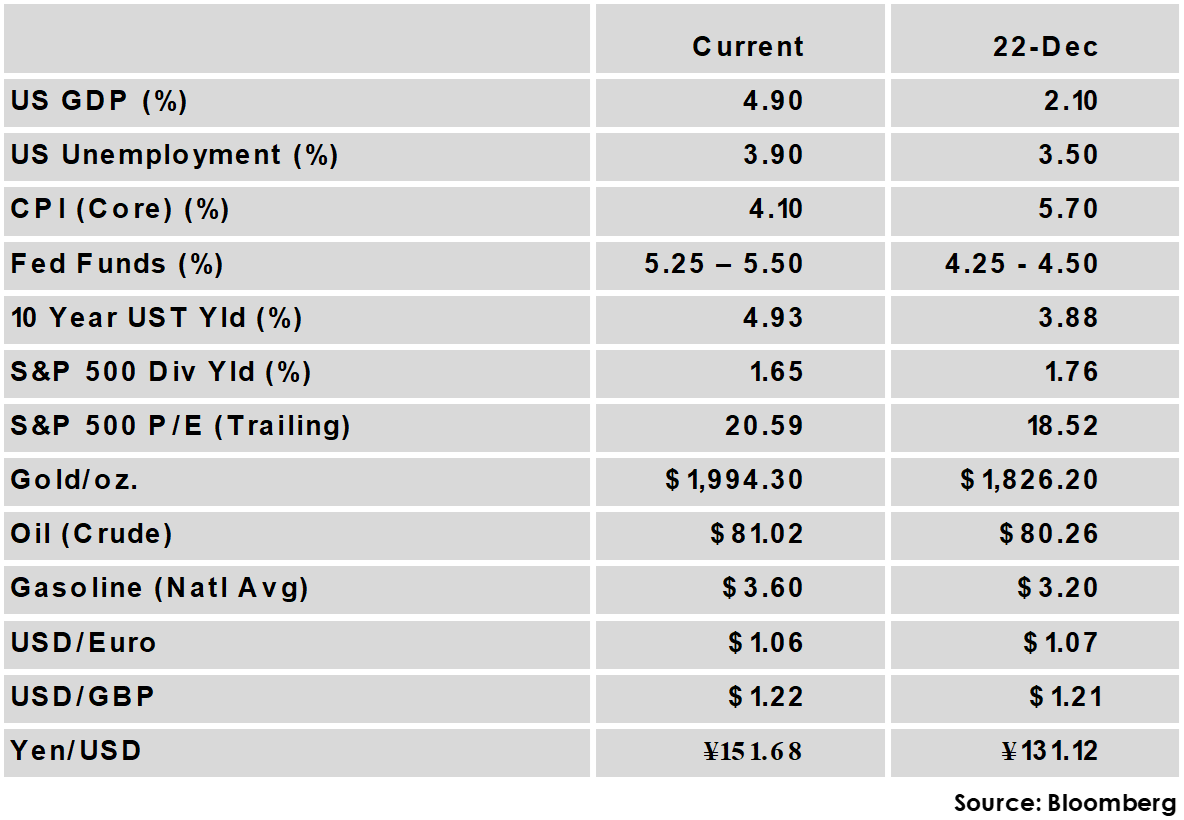

- Higher rates continued to weigh on asset prices, with the 10-year US treasury yield approaching the 5% mark for the first time in 16 years. Political issues also added to volatility, particularly the selection of a new Speaker of the House and speculation that the government could again face a shutdown in November.

- The tragic events unfolding in Israel also impacted markets, briefly causing a safe-haven rally in treasuries as concerns of expansion into a regional conflict added upside risk to oil prices.

- Core CPI increased 0.3% on the month for a 4.1% year-over-year rise, in-line with expectations and down from last month’s 4.3% rate, while headline CPI exceeded expectations at a 3.7% increase from a year ago, the same as last month.

- Economic data in the US remained broadly positive, with 3rd quarter GDP growing at a better-than-expected 4.9% rate and consumer spending remaining robust with a 0.4% increase. Meanwhile, Eurozone GDP had a slight decline in 3Q, while China’s economy exceeded expectations with a 4.9% growth rate.

- Higher rates continued to weigh on asset prices, with the 10-year US treasury yield approaching the 5% mark for the first time in 16 years. Political issues also added to volatility, particularly the selection of a new Speaker of the House and speculation that the government could again face a shutdown in November.

Global Equity

-

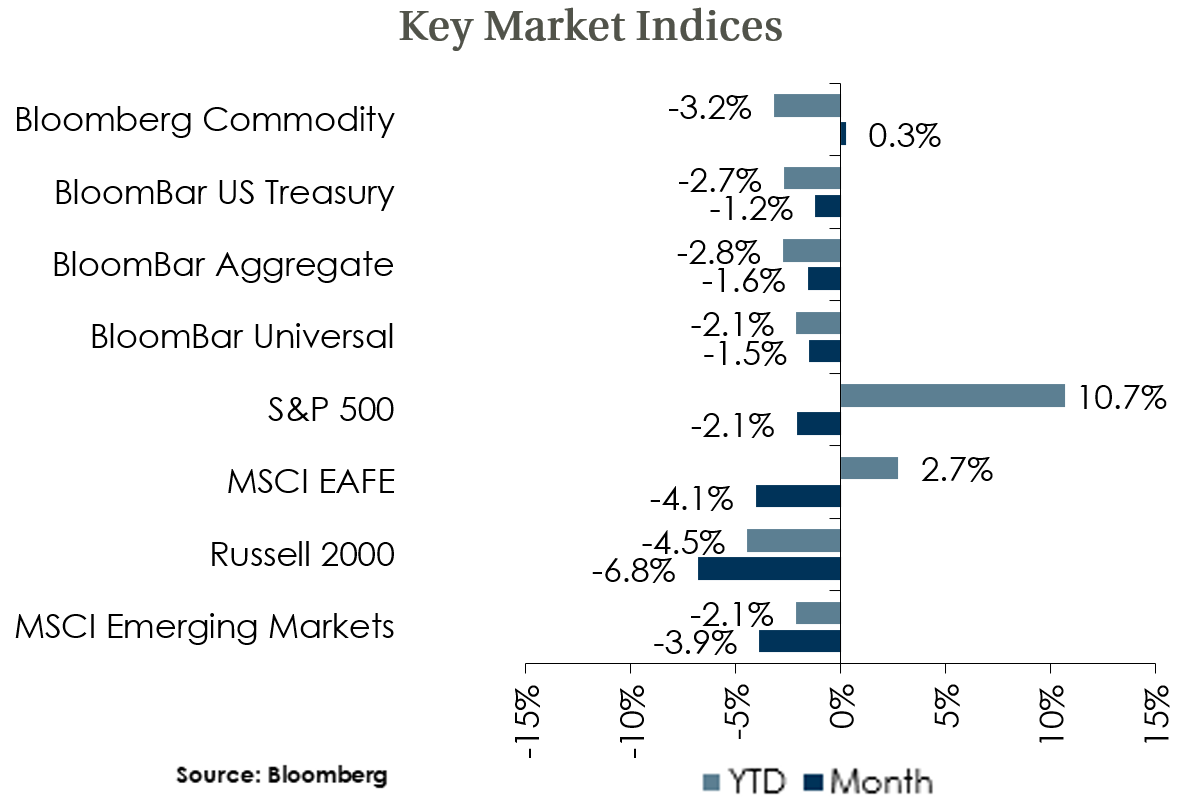

- Equities declined in the month as the rapid rise in treasury yields continued to pressure equity prices, with the S&P 500 notching its third straight negative month.

- Valuations on forward earnings declined and are now well below their averages across most equity indices. US large caps are an exception, primarily due to the valuation premium on the “Magnificent 7” stocks that have driven large cap returns YTD.

- With about half of S&P 500 companies reporting 3rd quarter results so far, 78% of companies have reported a positive earnings surprise. Year-over-year earnings growth is currently trending towards a modestly positive outcome, which would mark the first positive year-over-year growth since Q3 2022.

- Equities declined in the month as the rapid rise in treasury yields continued to pressure equity prices, with the S&P 500 notching its third straight negative month.

Global Fixed Income

-

- Longer duration US Treasury yields rose sharply as economic growth continued to exceed expectations, with the 10-yr UST yield rising 36 bps. The 10-year minus the 2-year yield spread is now only 16 bps inverted as shorter duration yields stayed steady, down from a peak of over 100 bps of inversion.

- Sovereign yields were mixed but generally less volatile than US yields, as the ECB held its rate steady after 10 consecutive hikes. Economic data out of Europe suggests rate cuts could come there sooner than in the US.

- Credit spreads widened in October, with investment grade rising 8 bps and high yield 43 bps higher, though both measures remain well below their averages.

- Longer duration US Treasury yields rose sharply as economic growth continued to exceed expectations, with the 10-yr UST yield rising 36 bps. The 10-year minus the 2-year yield spread is now only 16 bps inverted as shorter duration yields stayed steady, down from a peak of over 100 bps of inversion.

Global Real Estate

-

- Core real estate returns delivered a fourth consecutive quarter of negative returns in Q3. The office sector continues to be by far the worst performer, as the space suffers from work-at-home trends.

- While cap rates have risen from recent lows, real estate returns could continue to be challenged amid higher interest rates, tighter lending conditions, and reduced demand for office space.

- Core real estate returns delivered a fourth consecutive quarter of negative returns in Q3. The office sector continues to be by far the worst performer, as the space suffers from work-at-home trends.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.