Monthly Market Update | November 2025

November 2025

Monthly Market Update

Macro Update

-

-

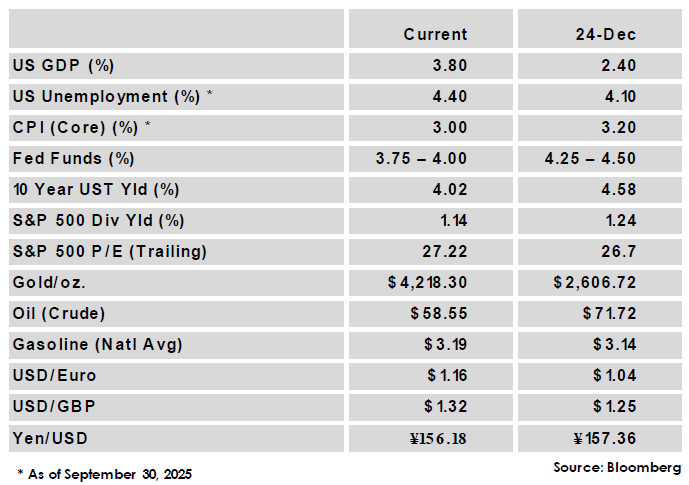

The US government shutdown became the longest in history before ending on November 12th. Markets saw a small relief rally before investor caution returned as ample uncertainty remains for investors including around trade policy, the labor market, monetary policy, and AI profitability.

-

The FOMC did not meet in November but the minutes from October’s meeting highlighted the disagreement within the committee over the upcoming rate decision, with committee members split over whether to cut 25 bps or hold rates steady.

-

The delayed September labor report was mixed, with a better than expected 119,000 jobs added but with unemployment edging higher to 4.4%, the highest since October 2021. October reports for both labor and CPI have been cancelled, and the next updates will be November’s reports released in mid-December.

-

The U.S. Supreme Court began hearing arguments on the legality of President Trump’s tariff policies. The Court often takes months to reach a decision, but analysts expect it could be sooner in this case. Administration officials have said they will turn to other tariff authorities if the court does not rule in its favor.

-

Global Equity

-

-

Global equities were mixed in November with increased volatility, reflecting market uncertainty in the limited data environment produced by the shutdown. Emerging market equities lagged, and growth underperformed value in the month as investors rotated out of tech stocks.

-

US equity earnings continue to be solid, with 3rd quarter S&P 500 earnings finishing with a 4th consecutive quarter of double-digit earnings growth.

-

Technology stocks were the worst performing sector in the month despite continued strong earnings results from companies like Nvidia as elevated valuations and uncertainty over the long-term payoff of AI spending weighed on performance.

-

Global Fixed Income

-

-

US treasury yields were lower in November as dovish comments from FOMC members appeared to win out near month-end, sending the market-based probability of a December Fed rate cut sharply higher to near 85%.

-

The Bank of England held rates steady at 4.0% in November, though it was a tight vote that saw several committee members favor a cut, while the ECB has maintained its 2.0% rate since June and is potentially done cutting.

-

Credit spreads widened modestly intra-month before reversing course following dovish Fed commentary. Cash yields look set to fall if rate cuts continue as expected, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate returns were positive for a 5th consecutive quarter. Returns were broad-based as all property sectors were positive, however returns remain largely income based as property price appreciation was again flat.

-

Property transaction volume has improved, and the office sector appears to have passed through its trough. Economic uncertainty around tariffs and job growth could impact dealmaking, but additional rate cutting in 2026 would be a positive for the real estate sector.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.