Monthly Market Update | November 2023

November 2023

Monthly Market Update

Macro Update

-

- Asset returns were broadly positive in November as cooling inflation, continued economic resilience, and increasing confidence that the Fed was done hiking rates sent treasury yields falling and boosted equity sentiment.

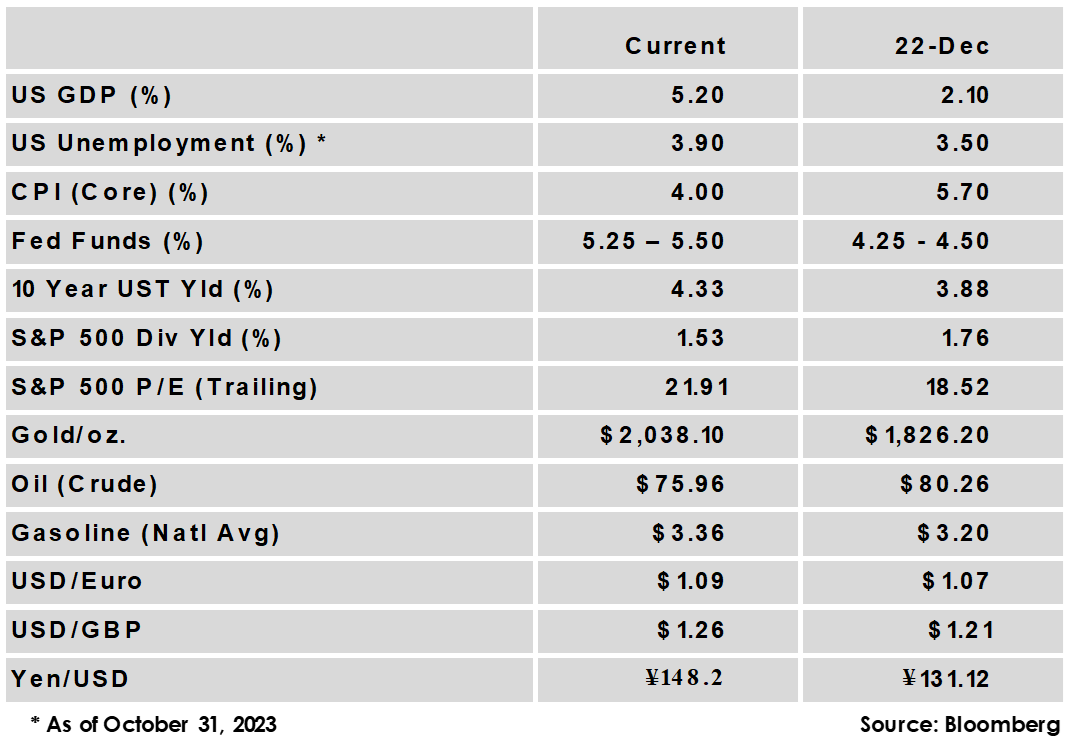

- An updated estimate of 3rd quarter GDP showed the US economy grew at a 5.2% pace, even faster than the initial estimate of 4.9%.

- Economic data was mixed, with a softening labor market leading unemployment to rise to 3.9%, the highest level in nearly two years. Meanwhile, inflation continued cooling with headline CPI showing a flat monthly reading while the year-over-year rate fell to 3.2%, and core CPI hit a two year low of 4%.

- The Eurozone’s latest inflation reading also cooled more than expected with a 2.4% year-over-year change, down from 2.9% in the prior month.

- China’s economy appears to be slowing to end the year after staging a modest rebound over the summer, with manufacturing activity contracting for a second month in a row in November, and the country’s huge real estate sector remaining in a protracted downturn.

- Asset returns were broadly positive in November as cooling inflation, continued economic resilience, and increasing confidence that the Fed was done hiking rates sent treasury yields falling and boosted equity sentiment.

Global Equity

-

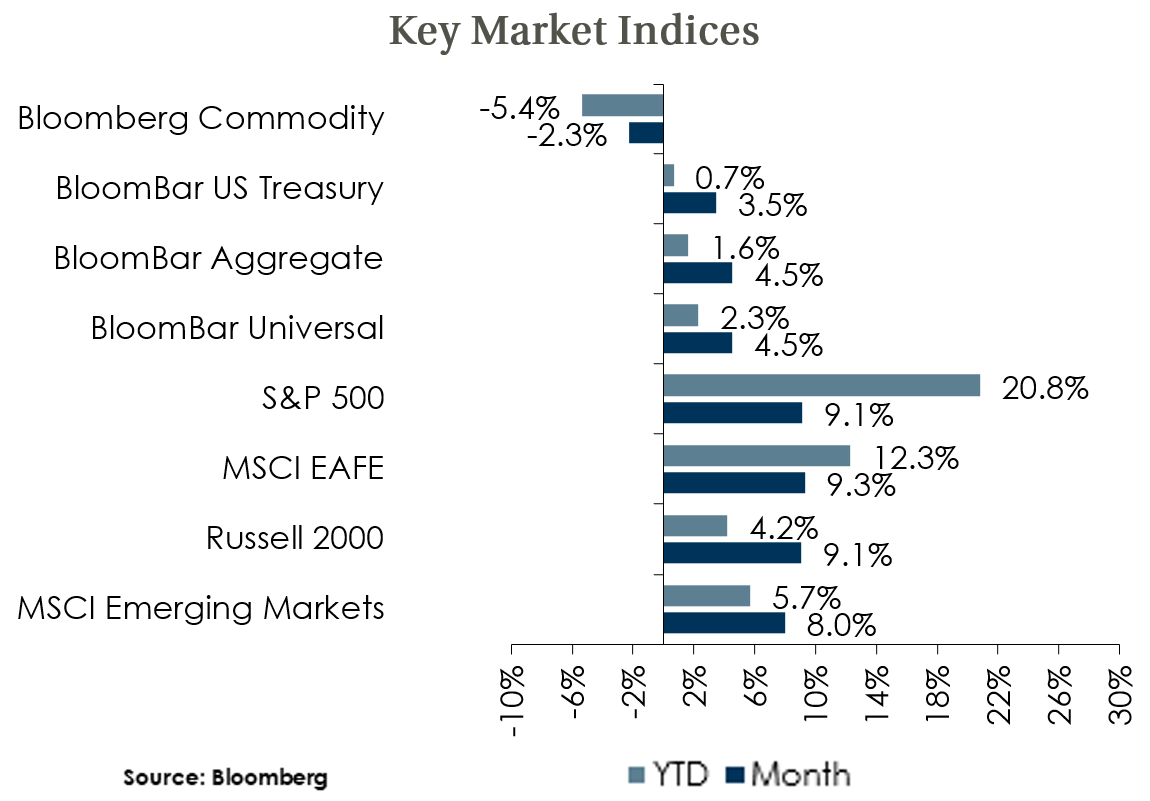

- Equities staged a remarkable rally in November to end a three month losing streak, with broad market indices up 8-10%.

- Valuations on forward earnings rose sharply following the strong month of performance and are now near or, in the case of US large caps, well above their average. The USD weakened as the market priced in 2024 Fed rate cuts, adding an additional tailwind to non-US market performance.

- Equity markets, particularly in the US, are pricing in a ‘Goldilocks’ scenario of falling inflation, a dovish Fed, and continued economic growth. Risks are skewed to the downside if inflation stalls in its descent, earnings weaken, or rate cuts don’t come as soon as currently anticipated.

- Equities staged a remarkable rally in November to end a three month losing streak, with broad market indices up 8-10%.

Global Fixed Income

-

- Falling inflation and easing Fed rate hike expectations sent 10-Year US Treasury yields tumbling 60 bps, the largest monthly decline since 2008.

- The Fed is expected to hold rates steady at its December policy meeting, and the market is now pricing in a high likelihood of a cut in the first half of 2024. The Bank of England and European Central Bank have also held rates steady in recent months, and non-US sovereign yields declined sharply in November.

- Credit spreads narrowed in November, with investment grade falling 25 bps and high yield falling 67 bps. Both measures are near the bottom of their historic ranges, but all-in yields remain attractive and would help weather potential economic deterioration.

- Falling inflation and easing Fed rate hike expectations sent 10-Year US Treasury yields tumbling 60 bps, the largest monthly decline since 2008.

Global Real Estate

-

- Core real estate returns delivered a fourth consecutive quarter of negative returns in Q3. The office sector continues to be by far the worst performer, as the space suffers from work-at-home trends.

- While cap rates have risen from recent lows, real estate returns could continue to be challenged amid higher interest rates, tighter lending conditions, and reduced demand for office space.

- Core real estate returns delivered a fourth consecutive quarter of negative returns in Q3. The office sector continues to be by far the worst performer, as the space suffers from work-at-home trends.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.