Monthly Market Update | May 2026

May 2026

Monthly Market Update

Macro Update

-

-

The US-Iran ceasefire became increasingly fragile through May, with multiple exchanges of strikes near the Strait of Hormuz. Despite the volatility, the US and Iran remain in negotiations to reopen Hormuz, and markets have largely looked through the noise.

-

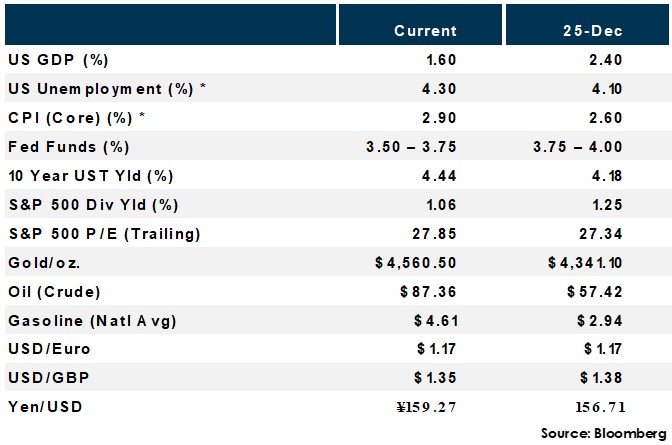

Q1 2026 GDP was revised down to 1.6% annualized from 2.0%, marking a meaningful deceleration from late 2025 as softer consumption partly offset the AI investment boom.

-

Kevin Warsh was confirmed as Fed chair in May in a near party-line Senate vote, succeeding Jerome Powell, who is staying on as a governor. Warsh's first meeting as chair is on June 17.

-

The April jobs report showed nonfarm payrolls rose 115,000, exceeding the 62,000 consensus, while the unemployment rate held steady at 4.3%. The solid gains suggest that the ongoing energy price shock has so far had little impact on the US job market.

-

Headline CPI accelerated to 3.8% year over year in April from 3.3% in March, the highest reading since May 2023, as Iran-related energy and goods price pressures broadened.

-

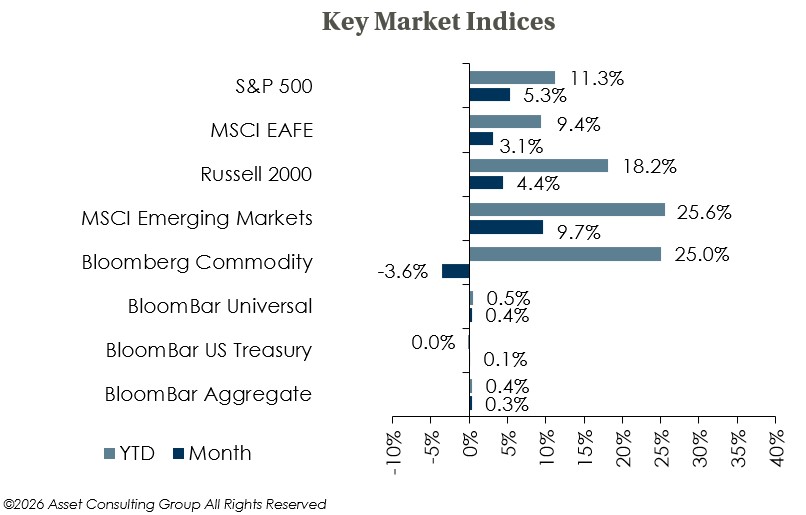

Global Equity

-

-

Equities extended their rally in May, but market breadth was narrow, with the tech sector providing most of the gains while non-US developed markets lagged.

-

Earnings momentum remains the equity rally's primary engine, with AI capex beneficiaries driving forward-estimate revisions higher even as oil-driven margin pressure has begun to surface for energy-sensitive sectors.

-

Equity valuations remain elevated, particularly for US large caps, but AI-driven earnings growth continues to support multiples. The key risk remains a re-escalation of the Iran conflict that sustains energy price pressures and further weighs on corporate margins.

-

Global Fixed Income

-

-

US Treasury yields were volatile in May and moved higher across the curve before easing into month-end on oil price relief and ceasefire-extension reports.

-

The Warsh-led Fed is widely expected to favor lower short-term rates, a reduced balance sheet, and reform-oriented communication changes, but the April minutes' hike-leaning bias has tempered expectations that he can engineer near-term cuts, and markets have largely priced out cuts for 2026.

-

Credit spreads remain near historical tights despite the bond market turmoil, supported by a still-constructive growth outlook and ceasefire hopes. Cash yields look likely to maintain current levels near-term, and absolute return strategies remain attractive as alternatives to duration-heavy portfolios.

-

Global Real Estate

-

-

Core real estate returns stayed consistent in early 2026, with returns continuing to be primarily income-based as appreciation remains flat. The office sector's stabilization from its trough continued as it performed in-line with the broader index.

-

The elimination of near-term rate cut expectations represents a headwind for the sector, as higher-for-longer financing costs weigh on valuations.

-

|

|

Disclosures and Legal Notice | © 2026 Asset Consulting Group. All Rights Reserved.