Monthly Market Update | May 2025

May 2025

Monthly Market Update

Macro Update

-

-

Market sentiment improved as the US and China agreed to suspend most tariffs on each others' goods for 90 days. However, trade policy remained volatile as reciprocal tariffs faced a court challenge, and the US-China trade dispute was at risk of re-escalating by month-end.

-

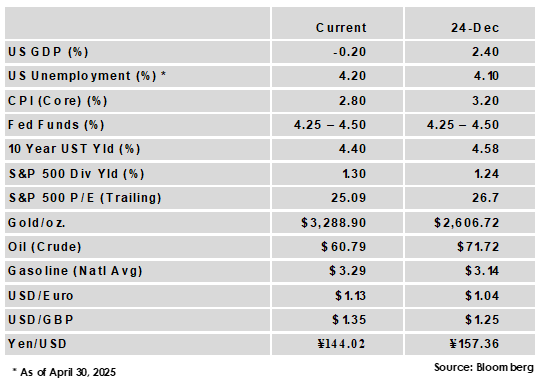

The FOMC held rates steady at 4.25 – 4.50% as Fed officials emphasized a patient approach, citing uncertainty around how tariffs will impact growth and inflation.

-

The US economy added 177,000 jobs in April and the unemployment rate held steady at 4.2%. This was slightly slower than the March pace but a solid figure overall that underscores the labor market’s resilience amidst ongoing tariff uncertainty.

-

The year-over-year rise in core CPI was unchanged from the prior month at 2.8% while core PCE slowed to 2.5% from 2.7%. The readings continued a positive string of inflation reports, but pressure from tariffs could push inflation higher over the next several months.

-

Global Equity

-

-

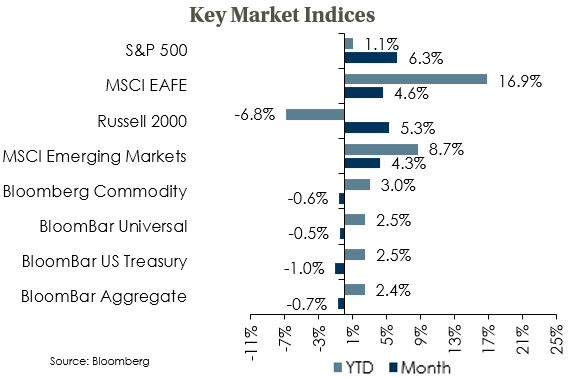

Equity performance was positive in May as investors largely looked past the late-month trade policy confusion. US large caps were the top performing broad equity index for the first time in 2025 but still trail non-US equities by a wide margin YTD.

-

With Q1 earnings reporting nearly complete, the S&P 500 is on track for earnings growth near 13%, the second straight quarter of double-digit growth. Despite strong earnings and lagging performance in recent months, valuations on US large caps are still expensive from a historical perspective.

-

Policy uncertainty is likely to weigh on global growth in the near-term, and trade terms will remain a key focus of equity markets. US growth is still forecast to outpace developed market peers in 2025, but with US forecasts declining and anticipated policy easing in Europe, that gap looks set to narrow.

-

Global Fixed Income

-

-

US treasury yields moved higher in the month as deficit concerns prompted Moody’s to downgrade the US credit rating to Aa1 from Aaa, making it the last of the three major rating agencies to do so. The 10-year US Treasury yield ended 24 bps higher at 4.40% and is now 53 bps above its early April low.

-

Non-US sovereign yields were mixed in May. The Bank of England cut its policy rate 25 bps to 4.25%, while the European Central Bank is widely expected to make another cut in June. Inflation data has largely supported central bank easing, but policy uncertainty has complicated the decision-making process.

-

Credit spreads tightened as trade tensions eased, with investment grade 18 bps tighter and high yield 69 bps tighter. Spreads remain low relative to history, but total income remains attractive, while absolute return strategies often benefit from volatility and can offer downside protection in an uncertain environment.

-

Global Real Estate

-

-

Core real estate returns maintained momentum with a third consecutive quarter of positive returns. All property sectors gained in the quarter as even the much-maligned office sector produced a positive return.

-

Trade policy uncertainty could slow the commercial real estate market as companies put investment and leasing decisions on hold. Potentially higher construction costs raise risks for new developments, but the supply constraint would support valuations on existing properties.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.