Monthly Market Update | May 2023

May 2023

Monthly Market Update

Macro Update

- Progress on the US debt ceiling emerged by month-end, as President Biden and House Speaker Kevin McCarthy struck a deal to suspend the debt ceiling in exchange for caps on discretionary spending. The bill passed in both houses of Congress as the month ended and was signed by the President in early June.

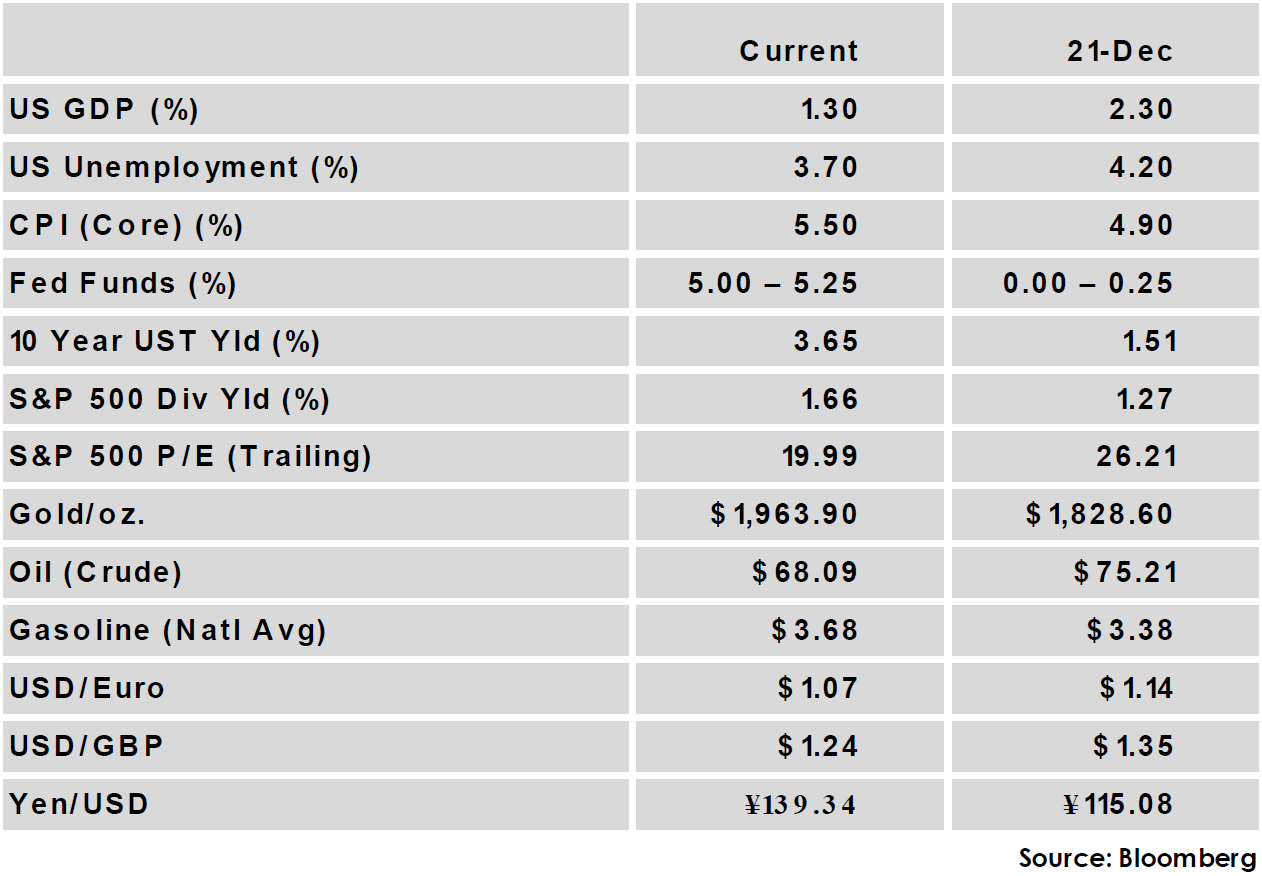

- The U.S. Fed increased the policy rate by 25 basis points, as expected, bringing the target range to 5.00%-5.25%. Messaging from Fed Chairman Jerome Powell emphasized that further hikes will be “data-dependent,” but suggested the potential for a pause ahead.

- US CPI fell to an annual increase of 4.9%, marginally less than the 5% estimate and the smallest increase since April 2021. However core PCE, the Fed’s preferred gauge, rose slightly from 4.6% to 4.7%.

- The US labor market exceeded expectations for the 13th consecutive month with payrolls increasing by 253,000 in April vs. a 185,000 estimate.

Global Equity

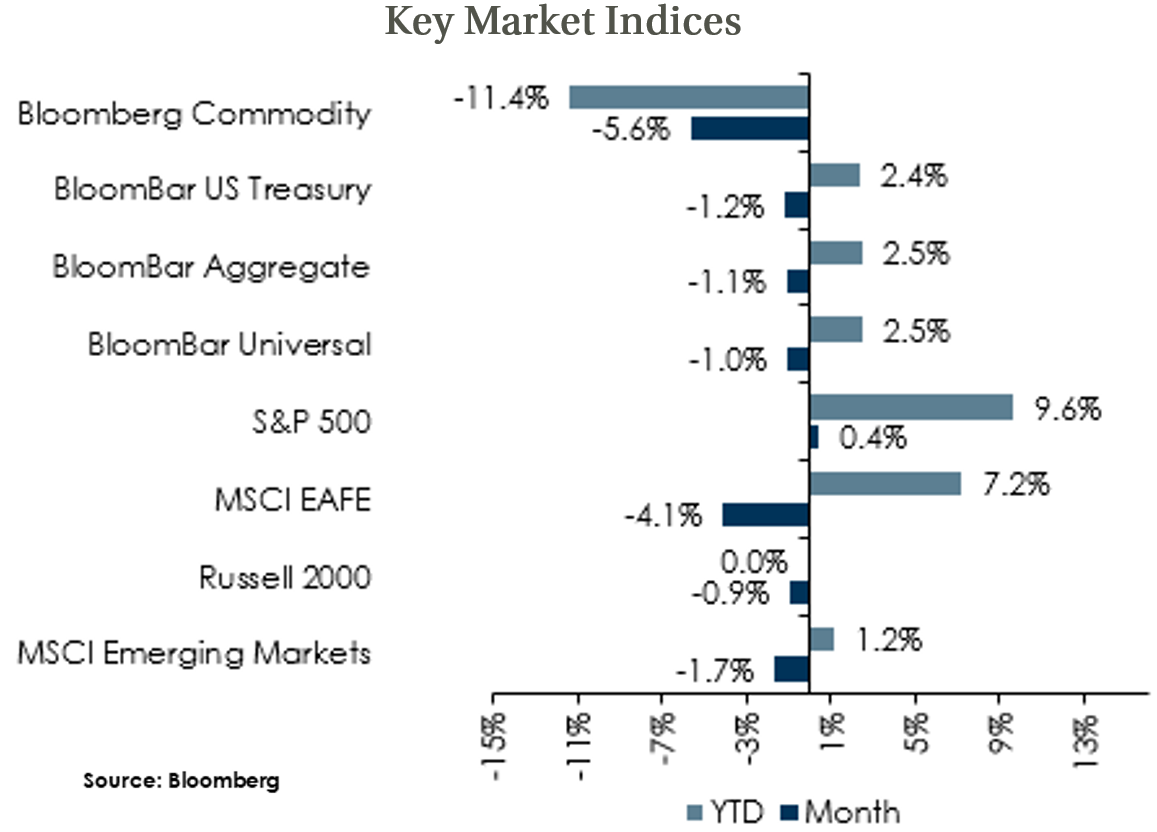

- Equity markets were generally lower in the month as concern over the US debt ceiling drove sentiment. Mega-cap tech stocks were an exception as they surged amid a wave of interest in AI, allowing the S&P 500 to eke out a positive return.

- Earnings surprises have continued to be positive. With the quarterly reporting season nearly finished, 78% of S&P 500 companies have reported a positive EPS surprise.

- The US dollar rebounded and was a key contributor in non-US underperformance, with the US dollar appreciating 3% against the Euro.

Global Fixed Income

- US Treasury yields moved higher amid solid economic data and uncertainty over whether the Fed would pause or continue its rate-hiking campaign.

- Sovereign yields were mixed globally as developed nation banks, including the ECB and BofE, continued their rate hiking campaigns while some emerging market banks have made plans for easing.

- Credit spreads were little changed to end the month with investment grade and high yield spreads 2 bps and 7 bps higher, respectively. However, intramonth saw greater volatility, driven largely by concern over the debt ceiling.

Global Real Estate

- Core real estate returns delivered a second consecutive quarter of negative returns in the first quarter of 2023.

- Real estate returns could continue to be challenged as higher interest rates put upward pressure on cap rates, which currently sit near historic lows.

- Banking industry stress could put further pressure on the commercial real estate market by constraining lending and raising borrowing costs.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.