Monthly Market Update | March 2026

March 2026

Monthly Market Update

Macro Update

-

-

The Iran War was the key focus for investors in the month, leading to increased market volatility.

-

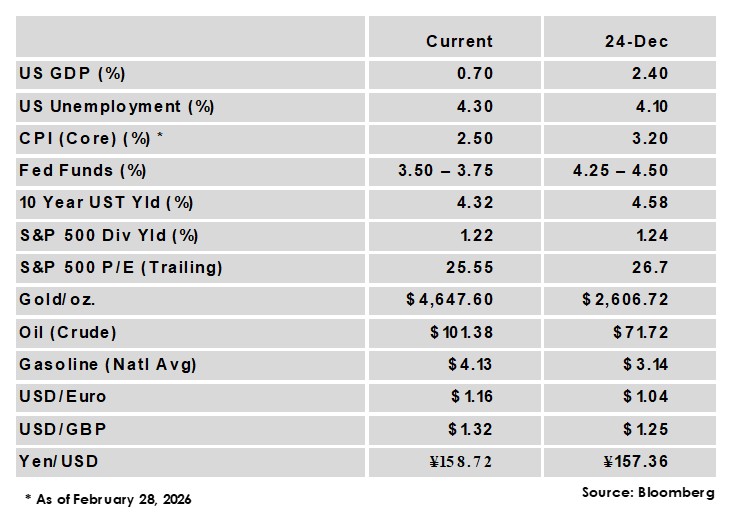

Fourth quarter US GDP growth was revised lower from 1.4% to 0.7% as most components of GDP saw downward revisions.

-

The US Fed held rates steady in the month, and the committee’s forward guidance continued to project one 25 bps cut in 2026.

-

The unemployment rate rose to 4.4%, as nonfarm payrolls fell in February by 92,000 jobs and January’s total was revised lower to 126,000 jobs. It was the third time in five months that the economy lost jobs.

-

Both CPI and core CPI were unchanged from the prior month, holding steady at 2.4% and 2.5%, respectively. The report showed inflation to be stable but still above the Fed’s 2% target, representing the last reading before higher oil prices impact subsequent reports.

-

The global economy is less oil dependent than in past energy crises, but an extended oil supply disruption would still likely be a drag on global growth as price pressures from higher energy costs weigh on consumer spending.

-

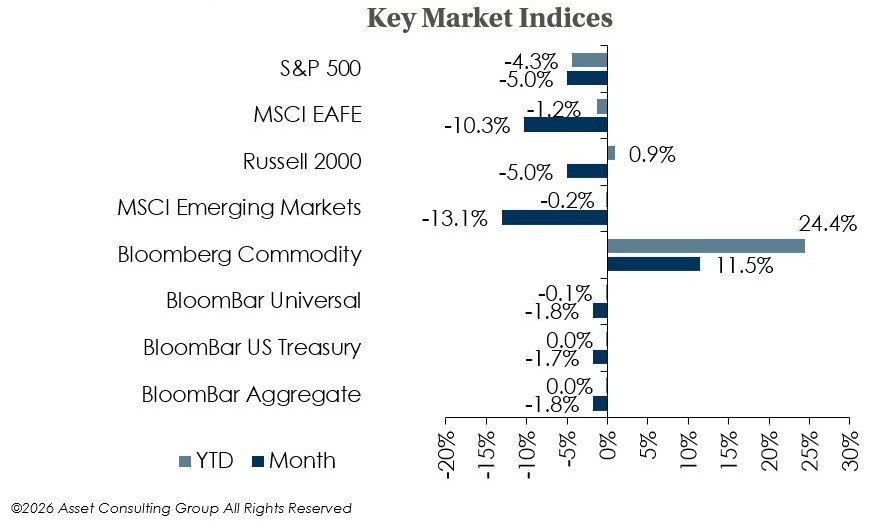

Global Equity

-

-

Broad equity indices fell in March as investors assessed the potential impact of higher oil prices on consumer demand and corporate profit margins. Despite the downturn equity valuations remain above average overall, particularly for US large caps, but growth expectations are supportive for now.

-

The US dollar maintained its status as a safe-haven as it strengthened in the month, reversing dollar weakness that had been a recent tailwind for non-US equities.

-

The duration of the oil shock will be the key factor for markets going forward. As a net exporter of oil, the US economy is more insulated from an oil supply crunch than most major economies in Europe and Asia, although that support is unlikely to fully offset the drag from an extended disruption.

-

Global Fixed Income

-

-

US treasury yields surged as higher energy prices fed inflation fears and diminished expectations of future rate cuts, and the 10-year treasury rose 38 bps to 4.32%.

-

While the FOMC continued to project one rate cut this year, higher inflation expectations raised market-based rate forecasts from two cuts to no cuts over the course of the month. Similar shifts in sentiment occurred across other major central banks.

-

Credit spreads widened in the month but were relatively contained as expectations remained for a short-term conflict that doesn’t derail strong US economic growth. Cash yields have fallen amid ongoing Fed rate cutting, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate returns stayed consistent, earning a modestly positive return for a sixth straight quarter. Returns continue to be primarily income based as appreciation stays flat. All property sectors were positive in the quarter.

-

Property transaction volume has improved, and the office sector appears to have passed through its trough. Economic uncertainty could impact dealmaking, but additional rate cutting in 2026 would be a positive for the real estate sector.

-

|

|

Disclosures and Legal Notice | © 2026 Asset Consulting Group. All Rights Reserved.