Monthly Market Update | March 2024

March 2024

Monthly Market Update

Macro Update

-

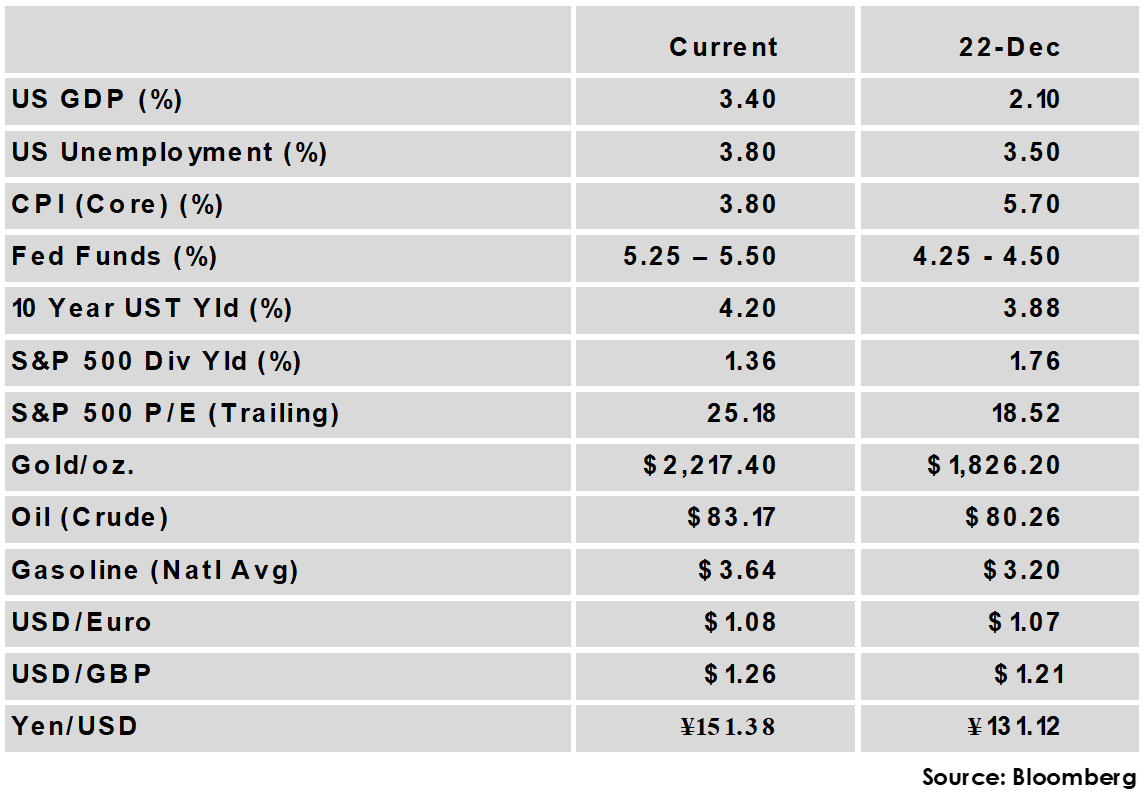

- The Federal reserve held its benchmark rate steady at 5.25%-5.5%, as expected. The Fed’s forward guidance continued to show expectations for three rate cuts this year, despite progress towards the Fed’s inflation goal proving stickier than hoped so far in 2024.

- Inflation results were roughly in-line with expectations in March, with Core CPI’s year-over-year increase falling from 3.9% to 3.8% and Core PCE, the Fed’s preferred gauge, falling from 2.9% to 2.8%. The results suggest inflation continues to moderate, albeit at a slow pace.

- Job creation exceeded expectations in February, but labor market growth and downward revisions to prior months saw unemployment climb from 3.7% to 3.9%.

- In another sign of resilience from the US economy, the Conference Board’s Leading Economic Indicators index rose in February, the first increase in two years.

- The Bank of Japan ended its negative interest rate policy with its first rate hike in 17 years as strong wage growth has pushed inflation in Japan to healthy levels. However the BoJ cautioned that this was not the beginning of an aggressive hiking campaign, which sent the Yen lower vs. the USD.

- The Federal reserve held its benchmark rate steady at 5.25%-5.5%, as expected. The Fed’s forward guidance continued to show expectations for three rate cuts this year, despite progress towards the Fed’s inflation goal proving stickier than hoped so far in 2024.

Global Equity

-

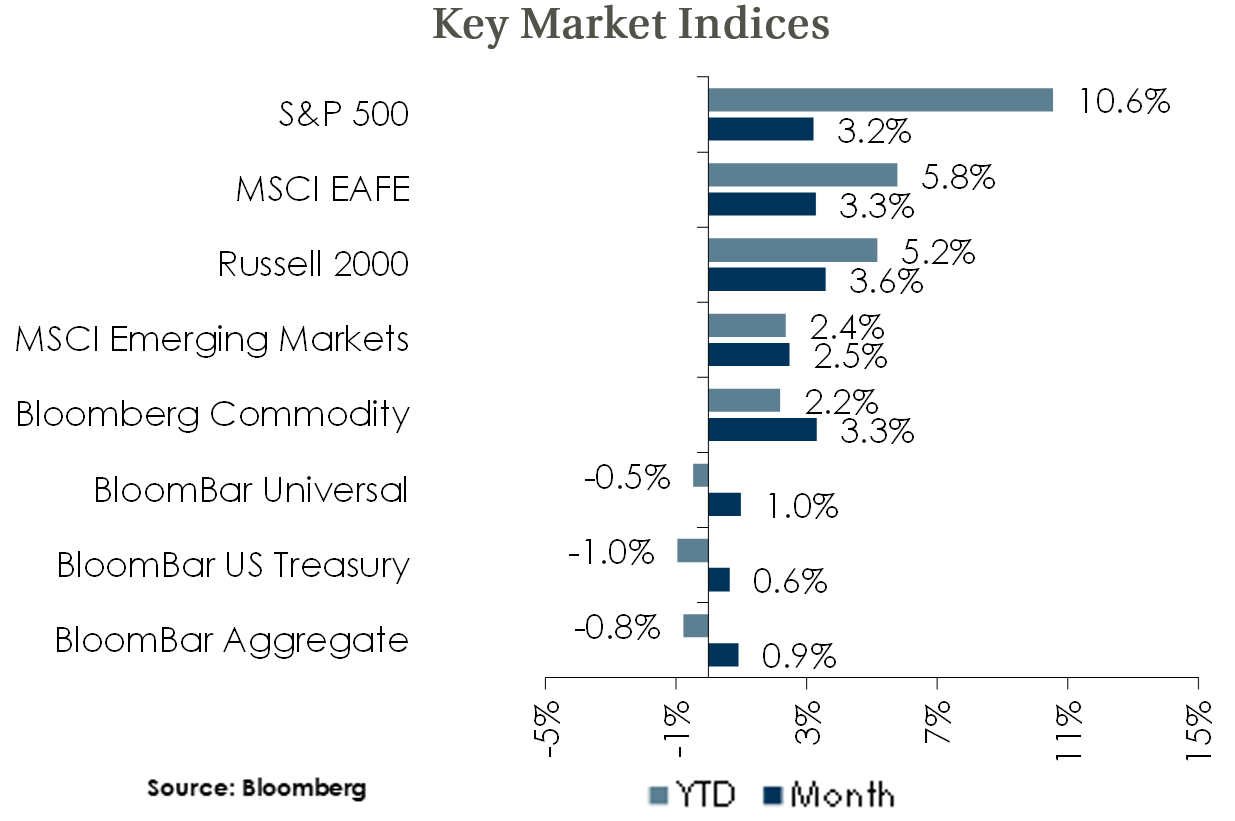

- Equity markets continued a strong start to the year with all major indices positive for the month and the S&P 500 ending on a five month winning streak.

- Contributions from the Tech sector are still a major driver of US Large Cap performance, but returns have broadened out so far this year with 203 members of the S&P 500 outperforming the broader index year-to-date. All sectors were positive in March, and the two best performing sectors were Energy and Utilities.

- Falling inflation and impending central bank policy easing have created a favorable backdrop for equities. The US large cap rally may persist while earnings growth looks robust and the Fed continues to project cuts, but stretched valuations leave a thin margin for error and tilts risks towards the downside.

- Equity markets continued a strong start to the year with all major indices positive for the month and the S&P 500 ending on a five month winning streak.

Global Fixed Income

-

- US Treasury yields fell modestly across the curve in March, with no maturity falling more than 7 bps. The 10-year US Treasury yield declined 5 bps to 4.20%.

- Inflation results and resilient economic growth have cooled rate cut expectations in recent months. Market pricing now forecasts about three cuts on the year, in-line with Fed guidance, with the first expected in June. The European Central Bank and Bank of England are also on track to start easing by mid-year.

- Credit spreads continued to tighten amid strong economic data with investment grade credit moving 6 bps tighter and high yield 13 bps tighter. Both measures are near the bottom of their historic ranges, but the economic backdrop remains supportive of credit and all-in yields are attractive relative to recent history.

- US Treasury yields fell modestly across the curve in March, with no maturity falling more than 7 bps. The 10-year US Treasury yield declined 5 bps to 4.20%.

Global Real Estate

-

- Core real estate performance was negative for a 5th straight quarter to end 2023, with property values declining for a 6th straight quarter. The office sector had by far the worst returns in the quarter, but all sectors were negative with the exception of hotels, which constitutes a very small part of the index.

- Cap rates have risen across property types but can likely rise further as they remain low relative to bond yields. Office continues to be the most troubled sector and the full effect of post-pandemic work arrangements will continue to play out as office leases come up for renewal.

- Core real estate performance was negative for a 5th straight quarter to end 2023, with property values declining for a 6th straight quarter. The office sector had by far the worst returns in the quarter, but all sectors were negative with the exception of hotels, which constitutes a very small part of the index.

|

|

Disclosures and Legal Notice | © 2024 Asset Consulting Group. All Rights Reserved.