Monthly Market Update | March 2023

March 2023

Monthly Market Update

Macro Update

- Market volatility surged after the sudden collapse of Silicon Valley Bank and Signature Bank, and fears around systemic risk to the banking sector weighed on market sentiment. However, by month-end, market volatility had declined as concerns around bank stress eased.

- Issues were not limited to the US banking system as doubts around the profitability of Credit Suisse led to that bank’s acquisition by UBS Group in coordination with Swiss regulators.

- Despite the volatility central banks continued their hiking campaign, with the US Fed hiking 25 bps, the Bank of England hiking 25 bps, and the ECB hiking 50 bps.

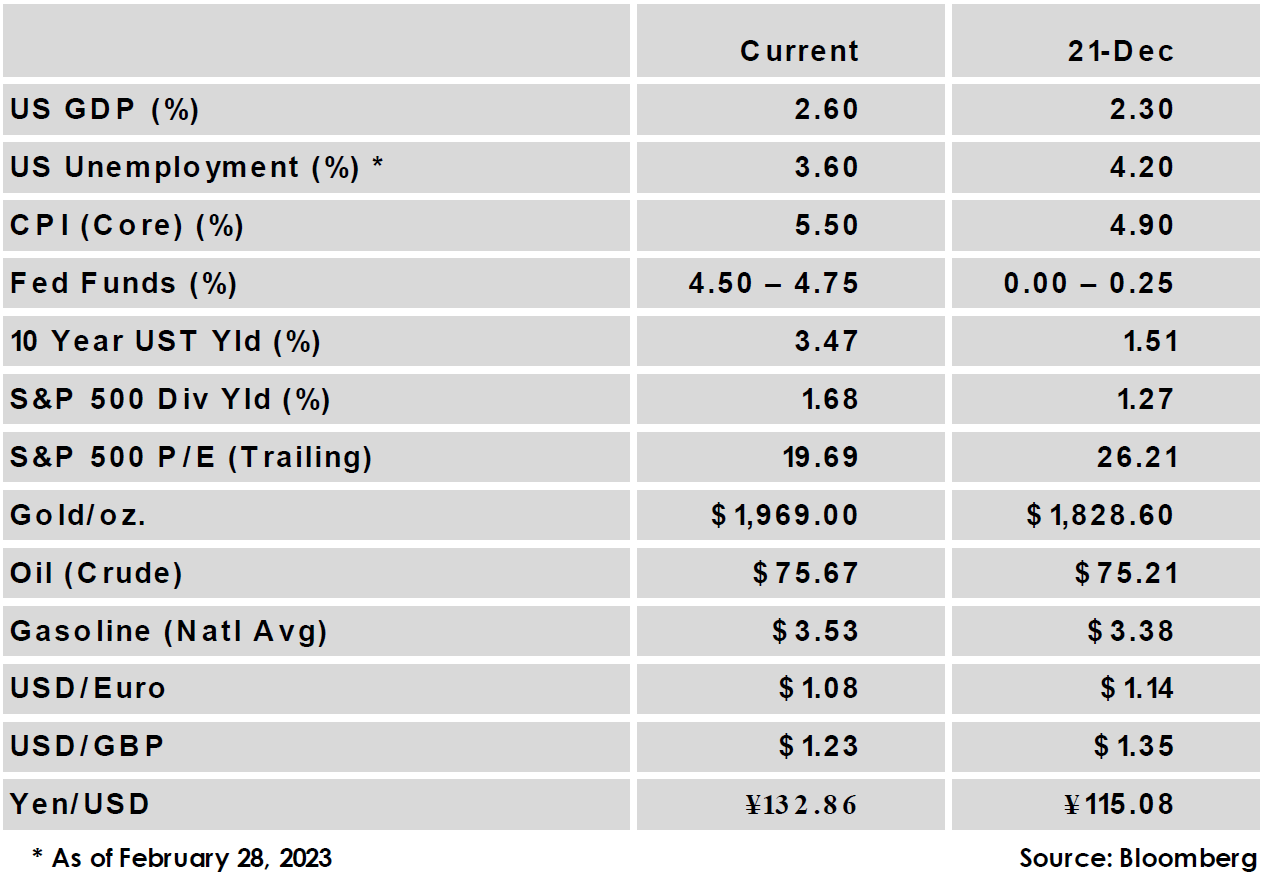

- US CPI fell from 6.4% to a 6.0% year-over-year increase, in-line with expectations. The US labor market remained robust with a stronger than expected increase to payrolls of 311,000.

Global Equity

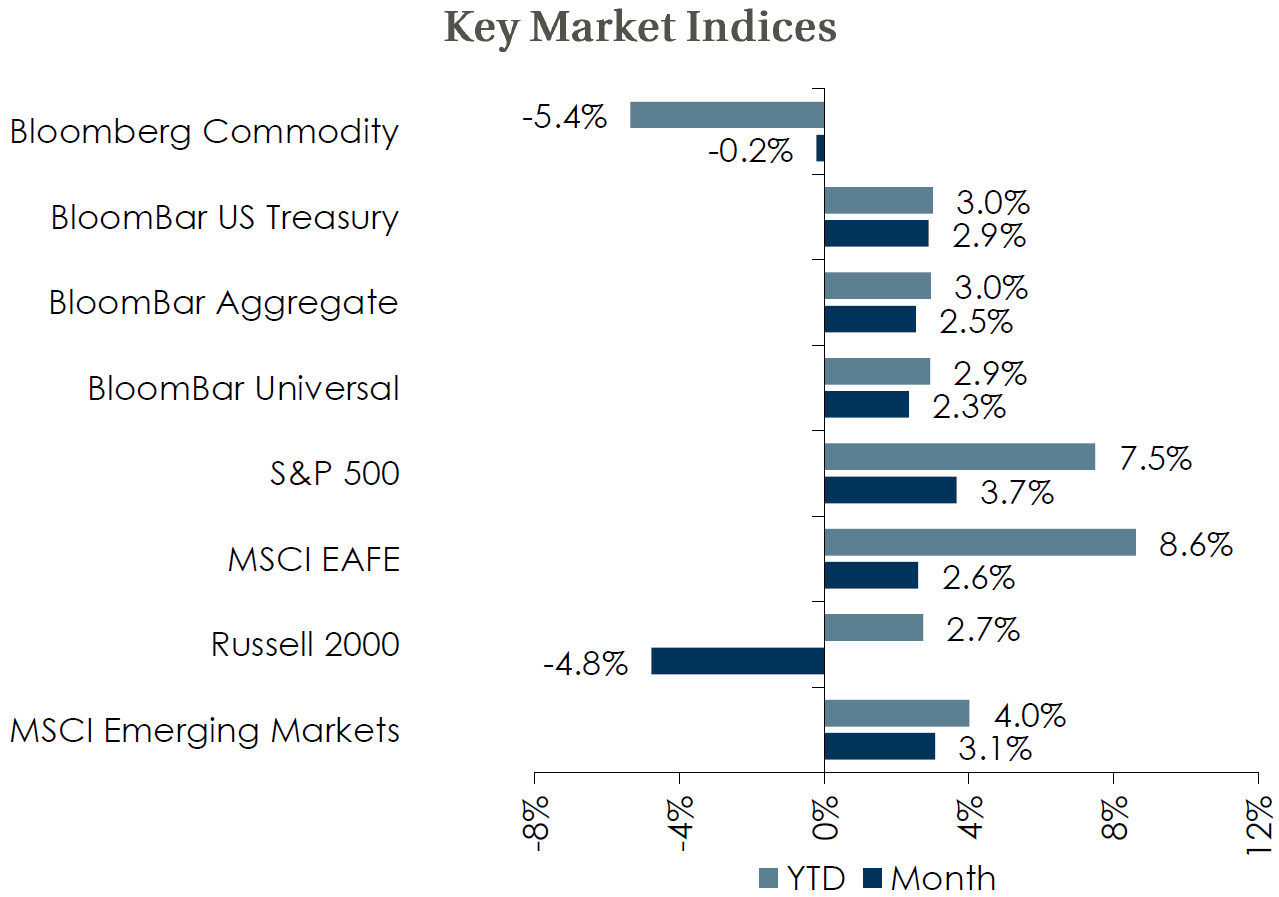

- Equity markets overcame the recent turbulence and were generally positive for the month and quarter.

- US Small Caps were an exception with severe underperformance in the month. The index was dragged down by regional banking concerns as the S&P Small Cap Financials index fell nearly 16%. Smaller companies also typically have a greater reliance on bank funding, which could be constrained.

- Valuations on forward earnings were modestly higher given positive performance and weakness in Small Cap earnings. Forward earnings projections have been under pressure in recent months across indices, and Non-US Developed currently exhibits the strongest recent trend.

Global Fixed Income

- Bond market volatility soared as the MOVE index, which tracks volatility in the government bond market, hit a 15-year high. The 10-year US Treasury yield declined 45 bps.

- Credit spreads widened in the month amid the banking stress as investment grade spreads were 14 bps higher and high yield 43 bps higher. Both measures remain below average, but strong fundamentals should help credit weather a slowing economy.

- Sovereign yields were lower across the globe, as the banking crisis led traders to reassess the likely path of central bank rates.

Global Real Estate

- Core real estate returns continued to decline, turning negative in the 4th quarter for the first time since 2Q 2020.

- Real estate returns could continue to be challenged as higher interest rates put upward pressure on cap rates, which currently sit near historic lows.

- Banking industry stress could put further pressure on the commercial real estate market by constraining lending and raising borrowing costs.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.