Monthly Market Update | June 2026

June 2026

Monthly Market Update

Macro Update

-

-

Investors welcomed progress towards fully reopening the Strait of Hormuz with the signing of the U.S.-Iran memorandum of understanding in June. Oil prices returned to near pre-war levels following the de-escalation, and forward inflation expectations declined.

-

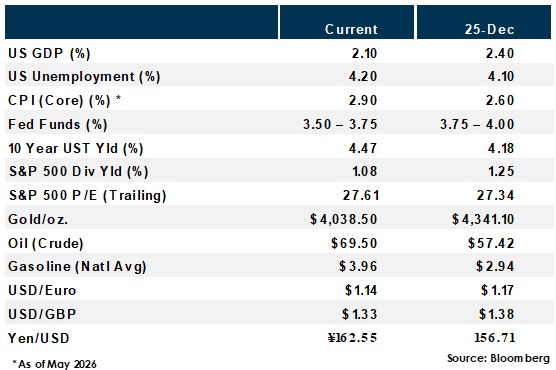

Q1 2026 GDP growth was revised to 2.1%, up from the second estimate of 1.6% and significantly stronger than the 0.5% growth recorded in Q4 2025.

-

In Kevin Warsh's first meeting as chair on June 17th, the Fed held rates steady at 3.50% - 3.75% in a unanimous vote and pared back its statement to remove the prior bias toward cuts. The committee’s forward rate projections tilted hawkish, with nine of 18 members projecting at least one hike by year-end.

-

The May jobs report showed nonfarm payrolls rose 172,000, well above estimates, while the unemployment rate held steady at 4.3%. The report added to momentum for a Fed rate hike in 2026, with a strong jobs market allowing the FOMC to focus on inflation risks.

-

Inflation accelerated in May with headline CPI rising 4.2% year-over-year, the fastest pace since early 2023, driven primarily by energy costs tied to the Iran war. Core CPI rose 2.9% from year-ago levels after rising 2.8% in April, suggesting there has been only modest broadening of energy price increases into core goods.

-

Global Equity

-

-

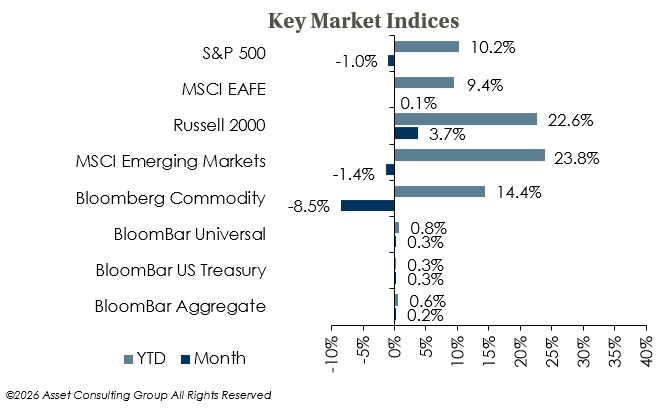

Equities turned choppier in June as a rotation out of crowded AI and technology leaders pressured the major indices. US small caps outperformed while US large caps and emerging markets turned negative, although equities overall wrapped up an exceptional first half of 2026.

-

Equity valuations are elevated, but earnings have been supportive. Earnings estimates have trended higher, with the S&P 500’s second quarter earnings growth rate currently estimated at 23.1%, up from 18.8% on March 31st, though the growth is concentrated in the energy and information technology sectors.

-

AI momentum continues to push equity markets to new highs despite geopolitical turmoil. However, the question remains whether revenue growth will give AI providers a sufficient return on their enormous investments, and increasing signs of AI customer price sensitivity contributed to June’s market swings.

-

Global Fixed Income

-

-

The US Treasury yield curve flattened in June, with the 2-year and 10-year yields increasing by 17 and 3 bps, respectively.

-

Two key global central banks raised interest rates in June as policymakers looked to stay ahead of energy-related price increases. The European Central Bank hiked 25 bps to 2.25%, its first increase in three years, while the Bank of Japan hiked 25 bps to 1.00%, the highest level since 1995.

-

Credit spreads widened amid high issuance but remain near historical tights, supported by a constructive growth outlook and an improving situation in the Mideast. Cash yields look likely to maintain current levels near-term, and absolute return strategies remain attractive as alternatives to duration-heavy portfolios.

-

Global Real Estate

-

-

Core real estate returns stayed consistent in early 2026, with returns continuing to be primarily income-based as appreciation remains flat. The office sector's stabilization from its trough continued as it performed in-line with the broader index.

-

The elimination of near-term rate cut expectations represents a headwind for the sector, as higher-for-longer financing costs weigh on valuations.

-

|

|

Disclosures and Legal Notice | © 2026 Asset Consulting Group. All Rights Reserved.