Monthly Market Update | June 2025

June 2025

Monthly Market Update

Macro Update

-

-

Market sentiment ended the month upbeat despite ongoing policy and geopolitical uncertainty. The deadline for the 90-day tariff pause looms in July, and while markets seem to have grown accustomed to higher tariffs, a widespread return to “Liberation Day” levels would be an unwelcome development.

-

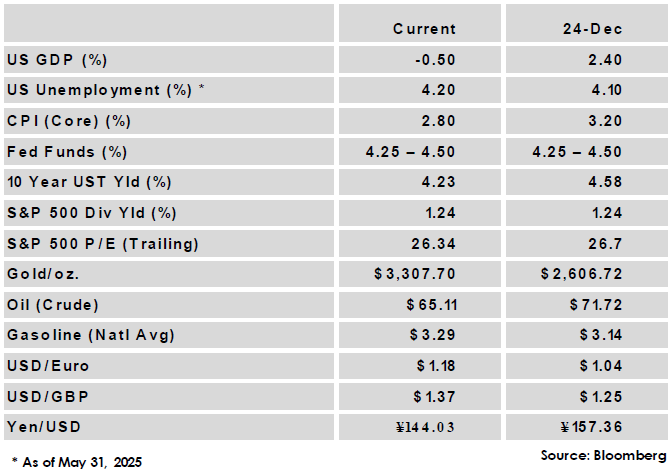

The FOMC held rates steady at 4.25 – 4.50% in a widely anticipated move. Markets largely expect the US Fed to maintain the current rate level again in the July meeting, but a few Fed officials have started to express support for a cut as long as inflation shows minimal response from tariff pressures.

-

The unemployment rate was unchanged at 4.2% and monthly job creation was solid at 139,000 jobs added, but lowered revisions to March and April results show an overall trend of modestly weaker job growth in 2025.

-

Inflation releases were largely uneventful as results were mixed but near expectations, with core CPI tracking sideways at 2.8% while Core PCE rose from 2.6% to 2.7%. Inflation has not yet seen a significant influence from tariffs, but some impact is still anticipated over the summer and fall.

-

Global Equity

-

-

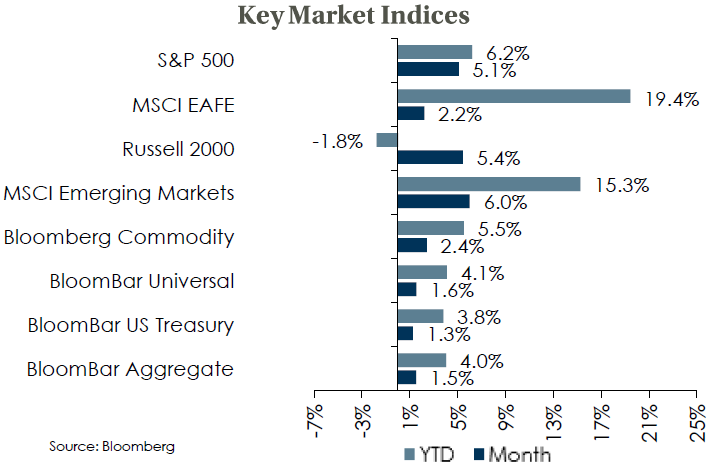

Equity performance was positive in June as investors became increasingly optimistic for trade deals. The S&P 500 reached a new all-time high for the first time since February, while emerging market equities were the top performers in the month.

-

Earnings expectations have rebounded as 12-mo forward analyst’s forecasts are back on an upward trend after weakening post-tariff announcements. However, valuations rose following the 2nd quarter’s solid performance and the US large cap PE ratio remains well above historic norms, potentially limiting additional upside.

-

Recent equity performance is discounting that worst case tariff scenarios have been avoided, but current tariff levels remain the highest in decades. Ongoing negotiations have lowered the risks to growth, but forecasts are still below year-end levels, and uncertainty around the impact of tariffs remains a key risk.

-

Global Fixed Income

-

-

US treasury yields declined in June amid heightened geopolitical risk and a softer labor market as the 10-year US treasury yield fell 17 bps to 4.23%.

-

Pressure from President Trump to reduce rates may be having an impact as support for a cut is growing among some Fed officials. Market pricing has shifted towards a higher chance of a July cut, but such a move still appears unlikely with a majority of Fed officials continuing to endorse patience.

-

Credit spreads continued their recovery from the tariff shock, further tightening below early-April levels. Spreads remain low relative to history, but total income remains attractive, while absolute return strategies often benefit from volatility and can offer downside protection in an uncertain environment.

-

Global Real Estate

-

-

Core real estate returns maintained momentum with a third consecutive quarter of positive returns. All property sectors gained in the quarter as even the much-maligned office sector produced a positive return.

-

Trade policy uncertainty could slow the commercial real estate market as companies put investment and leasing decisions on hold. Potentially higher construction costs raise risks for new developments, but the supply constraint would support valuations on existing properties.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.