Monthly Market Update | June 2024

June 2024

Monthly Market Update

Macro Update

-

- Several major central banks have initiated easing cycles with Europe and Canada cutting rates in June. They join Sweden and Switzerland among developed market banks which have cut rates in 2024.

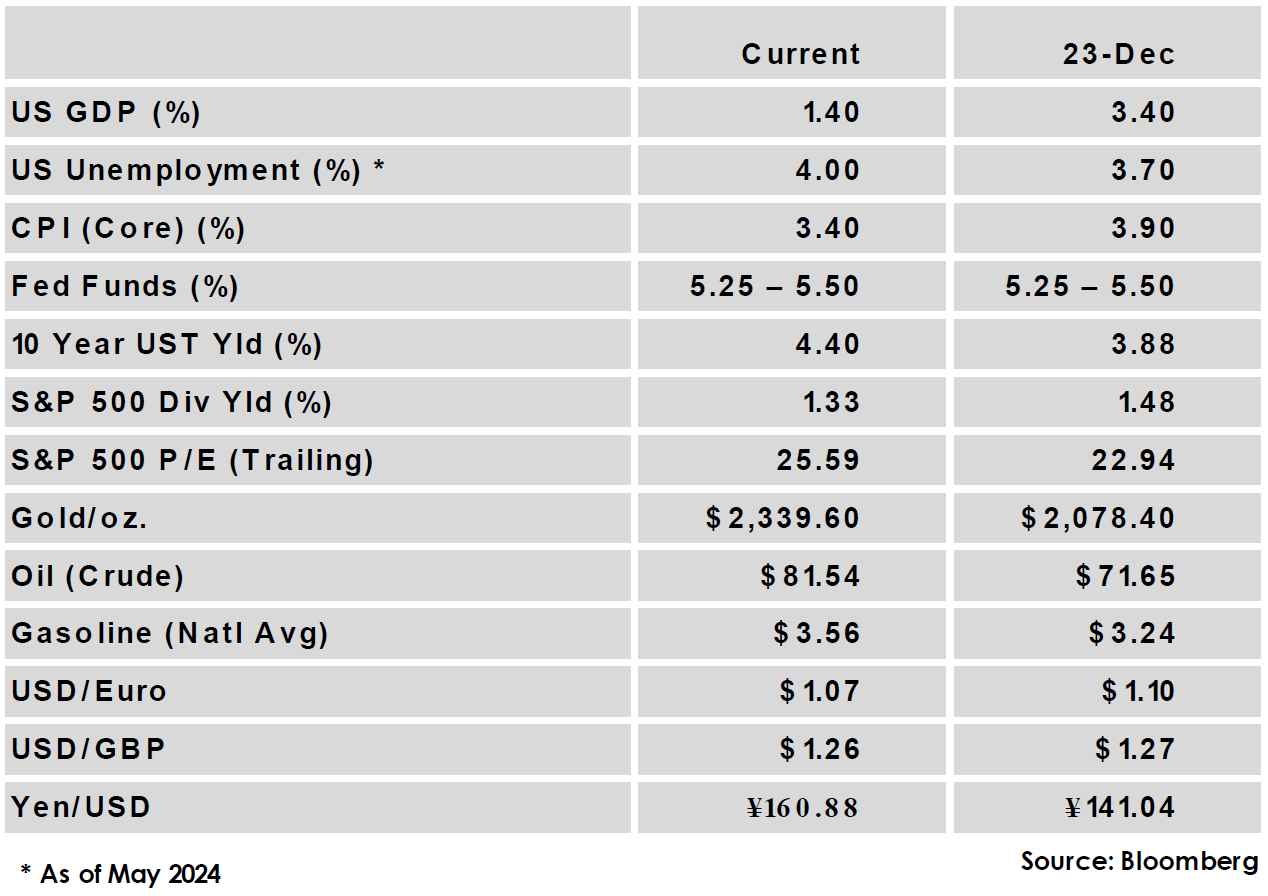

- The FOMC maintained its benchmark rate at 5.25% - 5.50%, as expected. The committee is still expected to cut later this year but is divided on when and how much to cut rates. Projections provided by the committee tilted hawkish, with one cut now expected in 2024, down from three in the previous projection.

- Inflation continued to moderate as core CPI’s year-over-year increase fell from 3.6% to 3.4% while core PCE, the Fed’s preferred gauge, fell from 2.8% to 2.6%.

- Jobs report data was mixed, as the economy added more jobs than expected with a healthy 272,000 while the unemployment rate ticked up from 3.9% to 4.0%. Wage growth, a key driver of inflation, remains stubbornly high, rising 0.4% on the month and 4.1% from a year ago.

- Global elections have seen unexpected results in places like India, Mexico, and the European Union, contributing to volatility in some non-US markets.

- Several major central banks have initiated easing cycles with Europe and Canada cutting rates in June. They join Sweden and Switzerland among developed market banks which have cut rates in 2024.

Global Equity

-

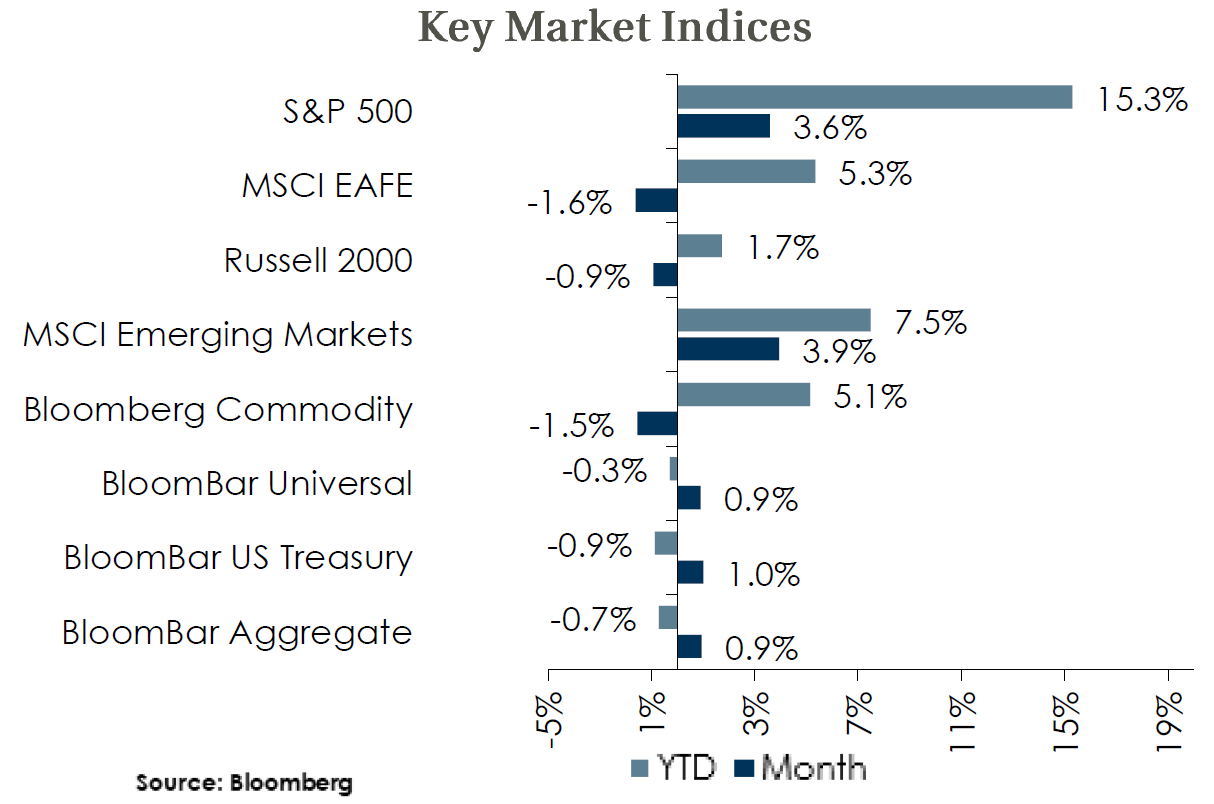

- Equity markets were mixed in June, with emerging market and US large cap equities delivering strong returns while the US small cap and international developed indices declined. European election results weighed on international developed returns, with France’s market in particular suffering a significant drawdown.

- US dollar strength has contributed to non-US underperformance YTD, reducing MSCI EAFE returns for US-based investors by over 500 bps vs. local index returns.

- Solid earnings and momentum continue to drive US large cap returns, but investors are increasingly nervous about elevated valuations for the large cap tech names that have propelled the rally. Central bank policy easing and improving growth in Europe should help support Non-US equities.

- Equity markets were mixed in June, with emerging market and US large cap equities delivering strong returns while the US small cap and international developed indices declined. European election results weighed on international developed returns, with France’s market in particular suffering a significant drawdown.

Global Fixed Income

-

- US treasury yields were marginally lower across the curve in June as inflation continued to cool. The 10-year US Treasury yield fell 10 bps to 4.40%.

- Non-US sovereign yields were mixed as electoral uncertainty and divergent central bank policy have increased volatility in global rates.

- Credit spreads continued to trade in a relatively narrow range, with high yield corporate spreads 1 bps wider and IG spreads 9 bps wider. Both measures are near the bottom of their historic ranges, but the economic backdrop remains supportive of credit and all-in yields are attractive relative to recent history.

- US treasury yields were marginally lower across the curve in June as inflation continued to cool. The 10-year US Treasury yield fell 10 bps to 4.40%.

Global Real Estate

-

- Core real estate continued its losing streak with a 6th straight quarter of negative returns in 1Q. Property values were down across every property type, with Office assets once again the worst performer with -5.0% depreciation.

- Cap rates remain under upward pressure in an environment of increased and sticky bond yields. Office continues to be the most troubled sector, and the full effect of post-pandemic work arrangements will continue to play out as office leases come up for renewal.

- Core real estate continued its losing streak with a 6th straight quarter of negative returns in 1Q. Property values were down across every property type, with Office assets once again the worst performer with -5.0% depreciation.

|

|

Disclosures and Legal Notice | © 2024 Asset Consulting Group. All Rights Reserved.