Monthly Market Update | June 2023

June 2023

Monthly Market Update

Macro Update

-

- Market sentiment was positive in June as the debt ceiling debate was resolved, the banking crisis faded from view, and economic data was largely positive.

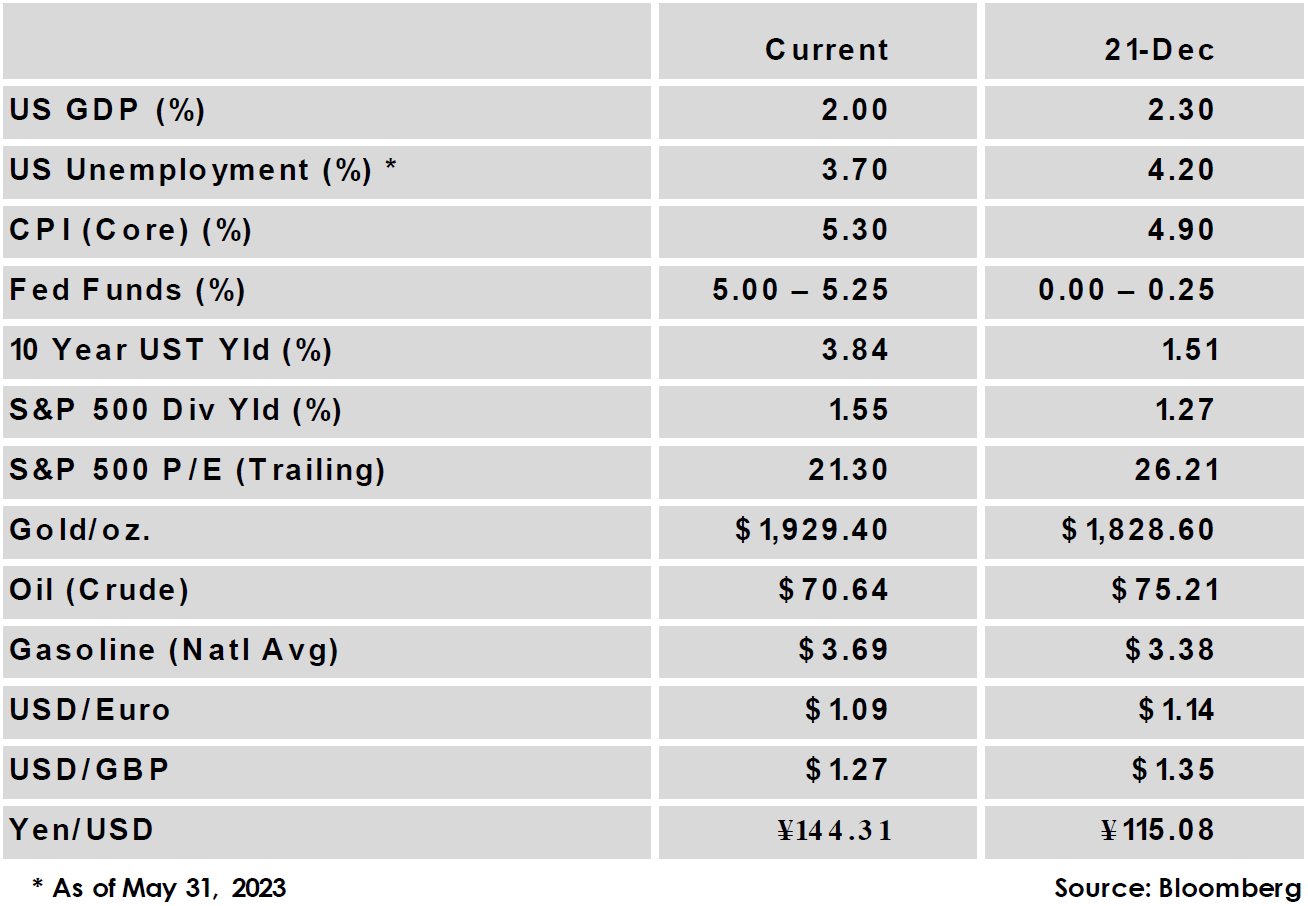

- The Fed paused its rate hiking campaign, as expected. However, anyone hoping for a peak in rates was disappointed as the Fed’s ‘dot plot’ signaled two more hikes ahead.

- Inflation continued to show signs of moderating but remains well above the Fed’s 2.0% goal as headline CPI fell to 4.0% y/y in May – the lowest since March 2021 – while stickier core CPI fell more modestly to 5.3% y/y.

- US GDP growth for the 1st quarter was revised sharply upward from 1.3% to 2.0%.

- Market sentiment was positive in June as the debt ceiling debate was resolved, the banking crisis faded from view, and economic data was largely positive.

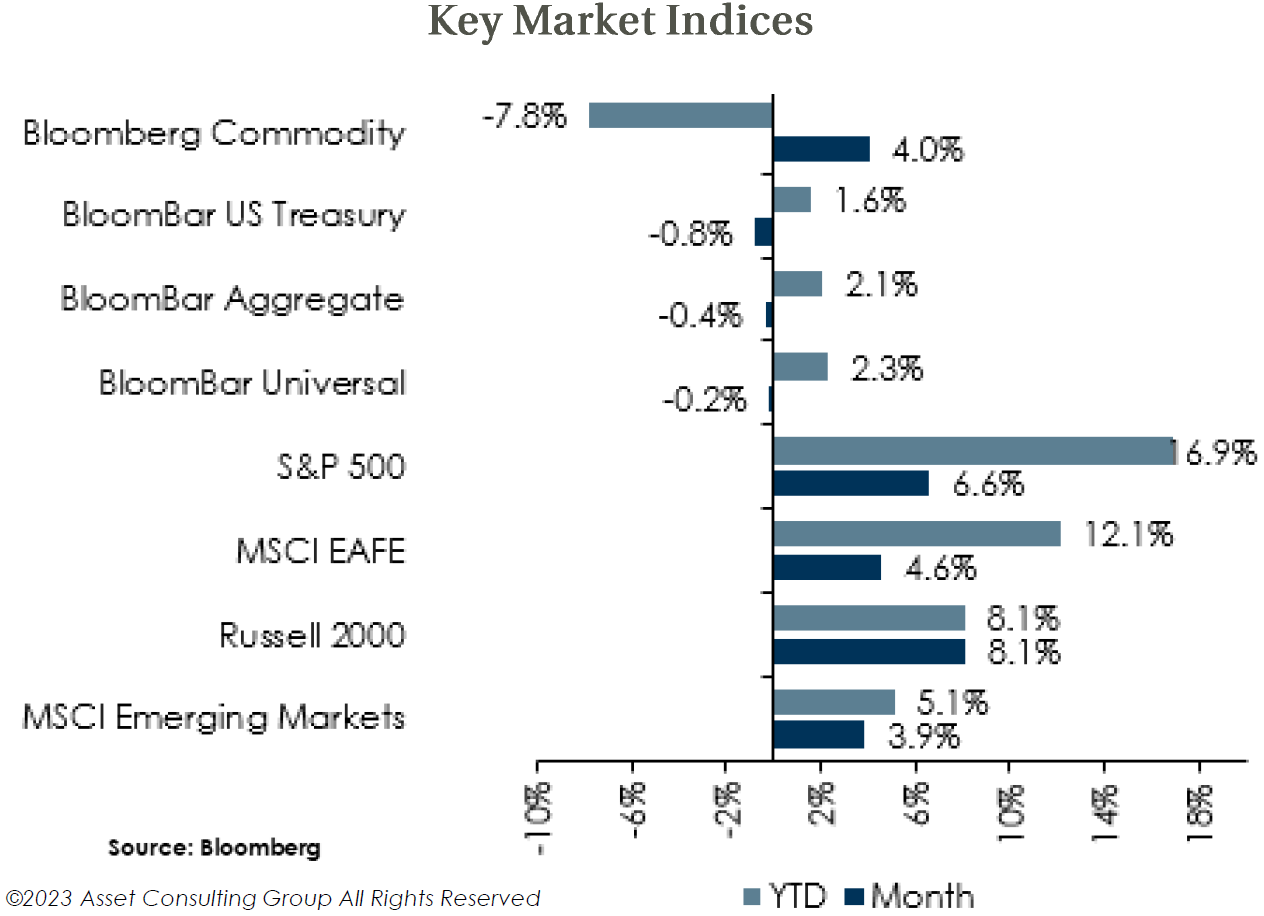

Global Equity

-

- Equity markets moved higher in the month as markets moved past the debt ceiling and banking crises, economic data remained largely positive, and inflation continued to moderate.

- Valuations on forward earnings rose in June and sit near neutral levels, except US Large Caps, which have seen valuations become stretched as economic data has surprised to the upside, and excitement over AI has buoyed tech stocks.

- Forward earnings estimates are relatively flat, aligning with the prevailing view of weak global growth ahead.

- The possibility of additional hikes from the Fed could limit further currency tailwinds for non-US equities in the near-term.

- Equity markets moved higher in the month as markets moved past the debt ceiling and banking crises, economic data remained largely positive, and inflation continued to moderate.

Global Fixed Income

-

- US Treasury yields moved higher as economic data continued to surprise to the upside and hawkish Fed messaging suggested the possibility of two more hikes this year.

- Global central bank policy is starting to show greater divergence, with a pause from the Fed, continued hikes from the ECB and Bank of England, and easing from China’s central bank.

- Credit spreads declined in the month with investment grade falling 15 bps and high yield 69 bps lower.

- US Treasury yields moved higher as economic data continued to surprise to the upside and hawkish Fed messaging suggested the possibility of two more hikes this year.

Global Real Estate

-

- Core real estate returns delivered a second consecutive quarter of negative returns in the first quarter of 2023.

- Real estate returns could continue to be challenged as higher interest rates put upward pressure on cap rates, which currently sit near historic lows.

- Banking industry stress could put further pressure on the commercial real estate market by constraining lending and raising borrowing costs.

- Core real estate returns delivered a second consecutive quarter of negative returns in the first quarter of 2023.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.