Monthly Market Update | July 2025

July 2025

Monthly Market Update

Macro Update

-

-

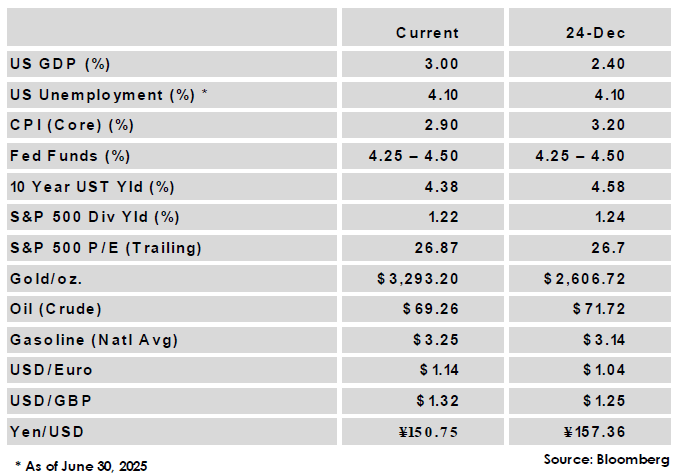

US GDP grew at 3.0% in the 2nd quarter, a sharp rebound from the 1st quarter’s -0.5% decline. Volatility from the trade component continued to skew the headline figure as the 1st quarter’s surge in imports from tariff front running came to an end, and the economy grew at a tepid 1.3% overall in the first half of 2025.

-

The FOMC held rates steady again at 4.25 – 4.50%. Market based odds for the September decision have been volatile as they react to incoming data.

-

The monthly jobs report was mixed in June, with solid headline figures including a decline in unemployment to 4.1%. However underlying data showed some signs of slowing, with weaker private sector job creation and a drop in labor force participation that drove much of the decline in unemployment.

-

Inflation ticked higher in June, with core CPI rising from 2.8% to 2.9% while Core PCE was in-line with May’s upwardly revised 2.8% increase. Goods inflation remains relatively subdued but some tariff-sensitive sectors saw price increases, supporting the Fed’s patience as it evaluates the impact of trade policy.

-

The US agreed to trade deals with key partners Japan and the European Union, with both getting similar 15% rates on most exports. Updated reciprocal tariffs for all countries without trade deals are forthcoming in early August.

-

Global Equity

-

-

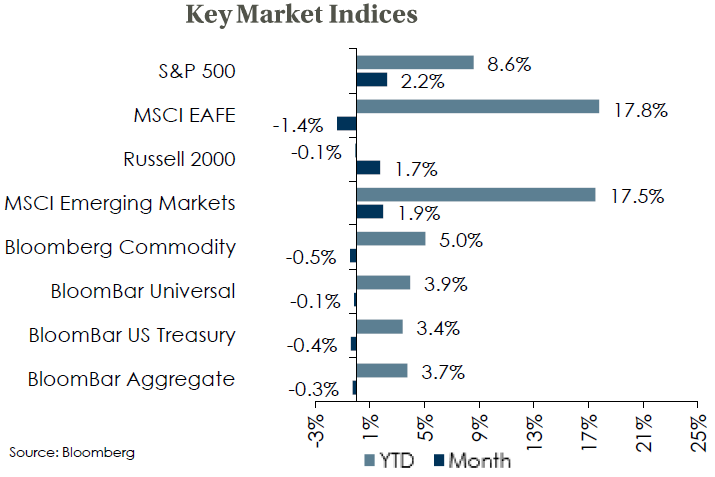

Equity performance was mostly positive in July with the S&P 500 continuing to rise off record highs. International developed stocks were laggards with modestly negative performance as trade deals boosted the US dollar and turned currency into a headwind for many non-US assets.

-

Equity valuations based on trailing PE ratios have risen across indices in recent months, and US large cap valuations are near the top of their historic range.

-

As trade deals continue to be finalized, a more certain trade outlook could stabilize the US dollar, reducing what has been a key YTD tailwind for non-US equities.

-

The ultimate economic impact of the new global trade regime remains difficult to predict, an environment that reinforces the case for global diversification.

-

Global Fixed Income

-

-

US treasury yields rose in July as solid economic data reduced expectations for Fed rate cuts, with the 10-year US treasury yield rising 15 bps to 4.38%.

-

The Fed rate decision was not unanimous, with two members supporting a cut, however market sentiment is still split on whether a cut will happen in September. The pace of global rate cuts is slowing overall, and the ECB is thought to be near the end of its easing cycle, having held its rate steady in July.

-

IG credit spreads reached a new YTD low while HY yield spreads also tightened. Spreads remain low relative to history, but total income remains attractive, while absolute return strategies often benefit from volatility and can offer downside protection in an uncertain environment.

-

Global Real Estate

-

-

Core real estate delivered another quarter of positive returns; however, the return is comprised almost entirely of income as price appreciation remains flat. All property sectors gained for the second consecutive quarter.

-

Commercial real estate seems to have stabilized overall even as office vacancy rates remain elevated. A resumption of Fed rate cutting could act as a catalyst for transaction volume and price appreciation.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.