Monthly Market Update | January 2026

January 2026

Monthly Market Update

Macro Update

-

-

January saw a barrage of headlines around geopolitics and domestic policy that financial markets largely shrugged off. Tariff threats over Greenland were an exception, weakening the US dollar and hurting equity sentiment, but a deal “framework” was reached that cooled tempers and helped equities rebound.

-

The US Federal Reserve paused rate cutting in January and signaled that it will likely remain on hold for the next meeting as well. Market expectations are currently for the next cut to occur in June.

-

The FOMC will be under new leadership soon as Chairman Powell’s term ends in May. President Trump nominated Kevin Warsh, a former Fed governor, as his replacement. The transition occurs as Trump administration legal challenges against Fed governor Cook and Chairman Powell threaten Fed independence.

-

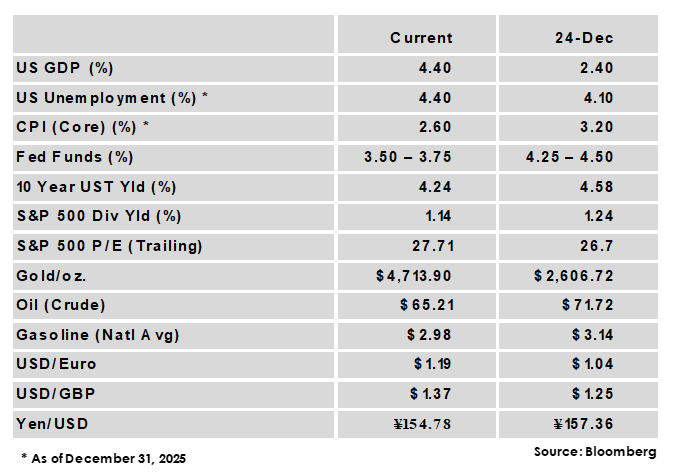

The month’s key economic data releases supported the Fed pause as unemployment fell to 4.4% while the rate of inflation was unchanged from the prior month, with CPI holding at 2.7% and Core CPI at 2.6%.

-

Global Equity

-

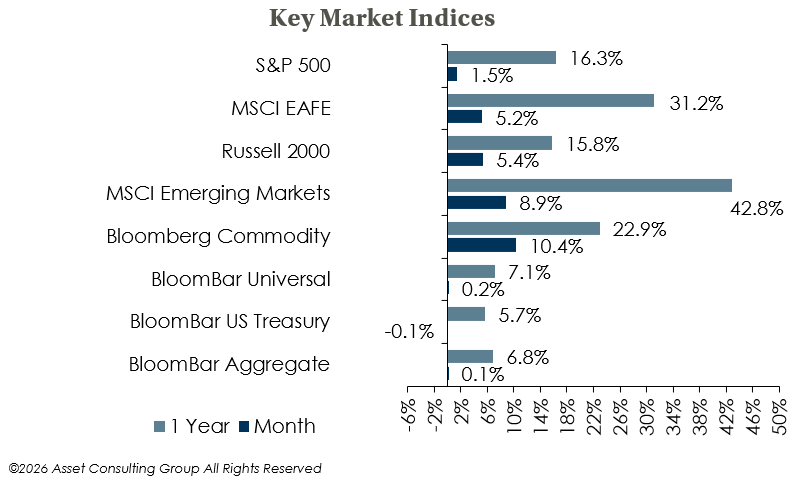

- Equity indices were broadly positive in January, with US large caps lagging both US small caps and Non-US stocks.

-

Quarterly earnings results have been mostly positive so far this quarter, yet the stocks of some tech giants still struggled despite solid earnings, highlighting the challenge of the high expectations currently baked into some equity valuations.

-

The backdrop for equities remains positive overall, with growth expectations trending higher and policy expected to remain easy. A weaker US dollar has been a tailwind for non-US assets.

Global Fixed Income

-

-

US treasury yields were higher in January as solid economic data lowered the market’s expectations for a rate cut in the first half of the year, and the 10-Year US treasury yield rose 7 bps to 4.24%.

-

The choice of Kevin Warsh as Fed chair is viewed as a relatively safe option given his previous experience with the Fed. Warsh has a history of being an inflation hawk and has advocated for a smaller balance sheet, however he likely wouldn’t have been nominated if Trump didn’t feel he would support lower rates.

-

Credit spreads ended the month lower and remain near historically tight levels, but the economic outlook is supportive and all-in yields remain attractive. Cash yields have fallen amid ongoing Fed rate cutting, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate returns were positive for a fifth consecutive quarter. Returns were broad-based as all property sectors were positive, however returns remain largely income based as property price appreciation was again flat.

-

Property transaction volume has improved and the office sector appears to have passed through its trough. Economic uncertainty around tariffs and job growth could impact dealmaking, but additional rate cutting in 2026 would be a positive for the real estate sector.

-

|

|

Disclosures and Legal Notice | © 2026 Asset Consulting Group. All Rights Reserved.