Monthly Market Update | January 2024

January 2024

Monthly Market Update

Macro Update

-

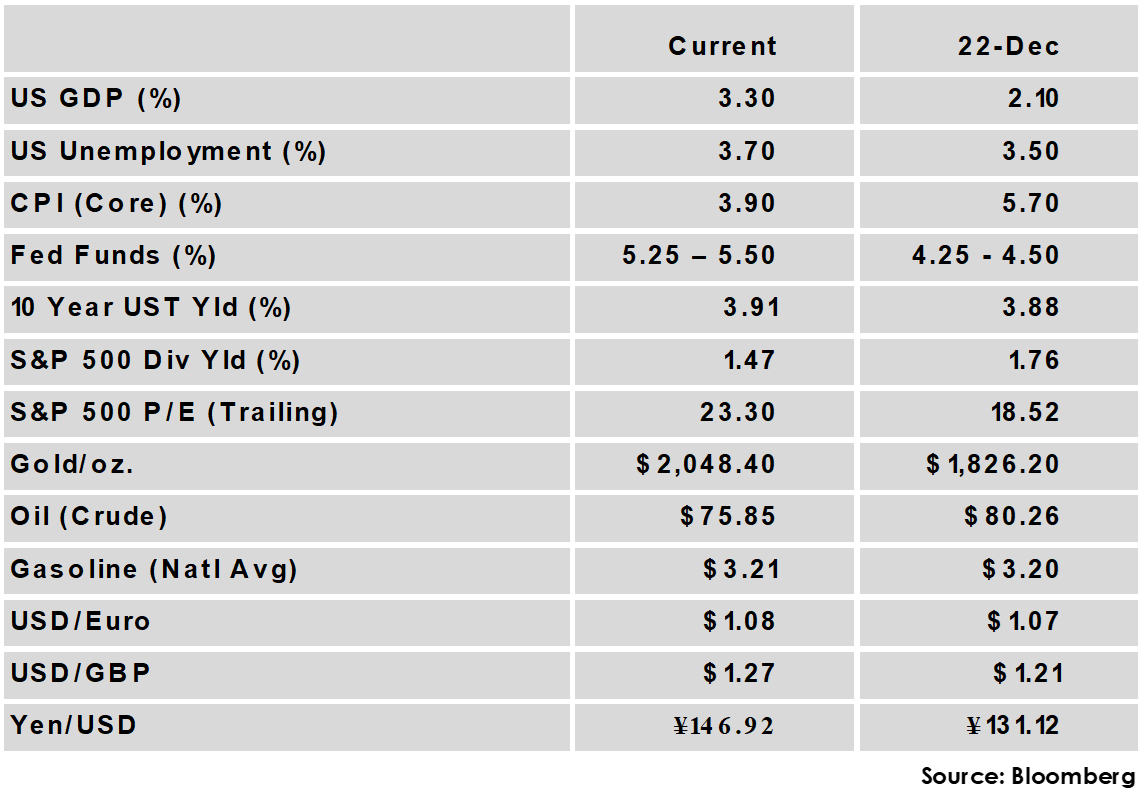

- US economic growth continued to exceed expectations, with GDP growing at a 3.3% annualized pace in the 4th quarter. This marks the 6th straight quarter the economy grew at a 2% or better annualized pace.

- The Federal Reserve held rates steady at 5.25% - 5.5% but also indicated that there are no imminent plans for a rate cut with inflation still running above target.

- Headline CPI rose 3.4% for the trailing one year, up from the prior month’s 3.1% gain. This was higher than expected, with stubbornly elevated shelter costs being a primary contributor. Core PCE, the Fed’s preferred gauge, fell to 2.9% from the prior month’s 3.2% change, and overall inflation trends remain encouraging.

- The Eurozone narrowly avoided a recession but the economy remains stagnant as GDP results showed no growth for the bloc in the 4th quarter.

- Supply chains are under renewed pressure as a drought in Panama and attacks on vessels in the Red Sea divert shipping from key canals to longer routes.

- US economic growth continued to exceed expectations, with GDP growing at a 3.3% annualized pace in the 4th quarter. This marks the 6th straight quarter the economy grew at a 2% or better annualized pace.

Global Equity

-

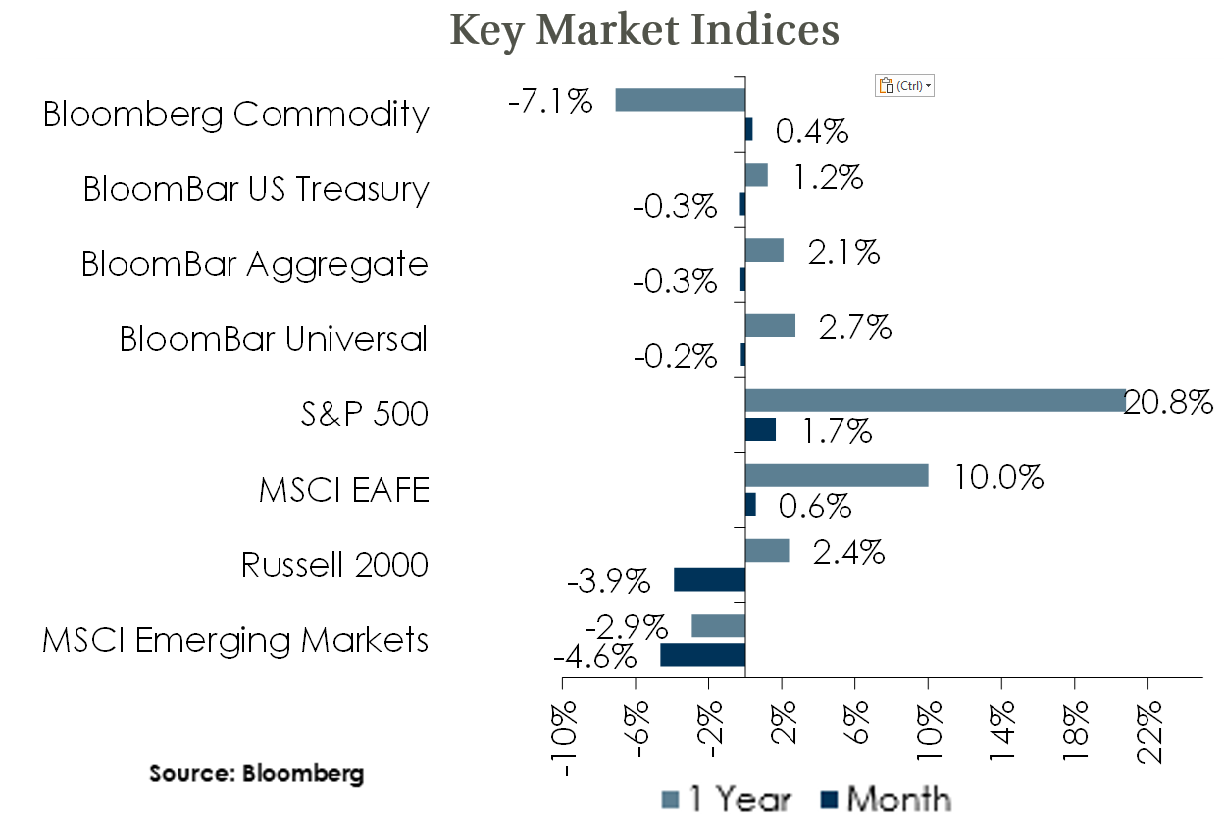

- Equity markets were mixed on the month, with US large caps outperforming and developed non-US also modestly positive.

- Trends from 2023 largely continued to begin the year, with growth leading value, large caps leading small caps, and China still a drag on the EM index.

- 4th quarter earnings results have so far seen positive surprises from a majority of reported S&P 500 companies. Particular attention will be paid to earnings from the big tech companies that have propelled the most recent market rally. Investors will have expectations for results that reflect the current hype around AI.

- Policy easing will be a positive for equities, but markets also face potential headwinds from slowing growth. US equity pricing is discounting a soft landing along with a brisk pace of rate cuts from the Fed, and deviations from that scenario could cause volatility for equities as the market adjusts its forecasts.

- Equity markets were mixed on the month, with US large caps outperforming and developed non-US also modestly positive.

Global Fixed Income

-

- US treasury yields were mixed with longer maturities higher. Rate moves were modest overall as market participants digested the Fed’s month-end guidance.

- Non-US sovereign yields rose in January. Major central banks have held rates steady in recent months, but have also pushed back against market expectations for imminent policy easing.

- Credit spreads were little changed in January with investment grade credit spreads 3 bps lower and high yield 21 bps higher. Both measures are near the bottom of their historic ranges, but all-in yields remain attractive and could help weather potential economic deterioration.

- US treasury yields were mixed with longer maturities higher. Rate moves were modest overall as market participants digested the Fed’s month-end guidance.

Global Real Estate

-

- Core real estate performance was negative for a 5th straight quarter to end 2023, with property values declining for a 6th straight quarter. The office sector had by far the worst returns in the quarter, but all sectors were negative with the exception of hotels, which constitutes a very small part of the index.

- Cap rates have risen across property types but can likely rise further as they remain low relative to bond yields. Office continues to be the most troubled sector and the full effect of post-pandemic work arrangements will continue to play out as office leases come up for renewal.

- Core real estate performance was negative for a 5th straight quarter to end 2023, with property values declining for a 6th straight quarter. The office sector had by far the worst returns in the quarter, but all sectors were negative with the exception of hotels, which constitutes a very small part of the index.

|

|

Disclosures and Legal Notice | © 2024 Asset Consulting Group. All Rights Reserved.