Monthly Market Update | February 2026

February 2026

Monthly Market Update

Macro Update

-

-

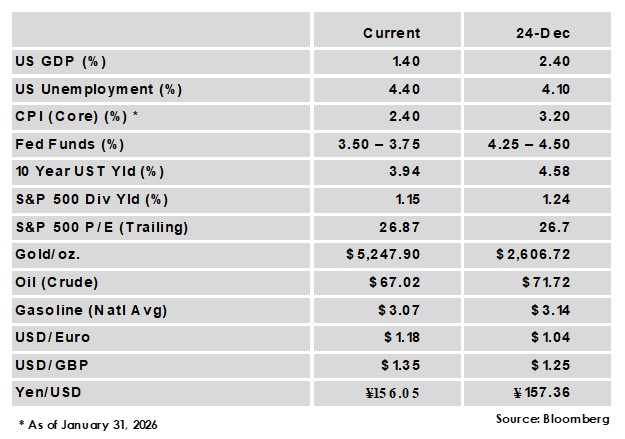

The US Supreme Court ruled tariffs based on the International Emergency Economic Powers Act unconstitutional, creating new uncertainty around tariff policy and raising questions around the status of billions in potential refunds.

-

Fourth quarter GDP undershot expectations, growing at a 1.4% annualized rate. The Commerce Department estimated that the prolonged government shutdown reduced the quarter’s growth by about 1%. For the full year in 2025, the US economy grew at a 2.2% pace, down from the 2.8% increase in 2024.

-

The labor market added more jobs than expected in January, although this came with a downward revision to last year’s hiring figures. Unemployment ticked lower to 4.3% and the report was viewed positively overall following 2025’s string of weak hiring numbers.

-

Inflation continued its course of gradual cooling as January Headline CPI eased to 2.4% year‑over‑year from 2.7% in December.

-

Geopolitical uncertainty remained elevated as the US and Israel launched a joint attack on Iran. The conflict threatens global energy markets, and oil prices moved sharply higher in the aftermath.

-

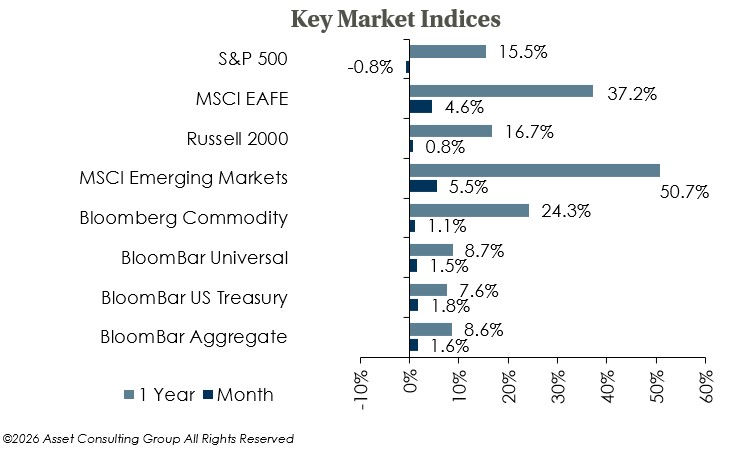

Global Equity

-

-

Equity indices were mixed in February, with US large caps declining while US small caps and non-US markets gained.

-

A sell-off in AI-themed equities has hurt US large caps as investors grow wary of the increasing sums of AI related capex from hyperscalers, while other sectors have drawn down on fears of AI technology disrupting their business model. Rotation into sectors deemed insulated from AI has helped offset the declines.

-

The potential extent of AI disruption is likely to be an ongoing debate, but the backdrop for equities remains positive overall. Growth expectations have trended higher and policy is expected to remain easy, however a prolonged disruption to energy markets could impact consumer spending and be a drag on growth.

-

Global Fixed Income

-

-

US treasury yields fell in February with weaker GDP growth, geopolitical risks, and fatigue over the AI narrative all supporting a rotation into US treasuries.

-

The European Central Bank (ECB) and the Bank of England (BoE) left rates on hold at 2.15% and 3.75%, respectively. The ECB is broadly expected to keep rates on hold for the duration of 2026, while BofE officials gave guidance for at least one cut this year.

-

Credit spreads widened in the month but remain near historically tight levels given the supportive economic outlook, and all-in yields remain attractive. Cash yields have fallen amid ongoing Fed rate cutting, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate returns stayed consistent, earning a modestly positive return for a sixth straight quarter. Returns continue to be primarily income based as appreciation stays flat. All property sectors were positive in the quarter.

-

Property transaction volume has improved, and the office sector appears to have passed through its trough. Economic uncertainty around tariffs and job growth could impact dealmaking, but additional rate cutting in 2026 would be a positive for the real estate sector.

-

|

|

Disclosures and Legal Notice | © 2026 Asset Consulting Group. All Rights Reserved.