Monthly Market Update | February 2024

February 2024

Monthly Market Update

Macro Update

-

- Financial markets were dealt a mixed-bag of economic news in February, all of which was largely overshadowed by robust earnings reports out of big-tech that propelled equity markets higher and maintained enthusiasm around artificial intelligence.

- Both CPI and PPI reported higher than expected price increases in February, prompting speculation over whether inflation was reaccelerating or the results were due to one-off seasonal factors.

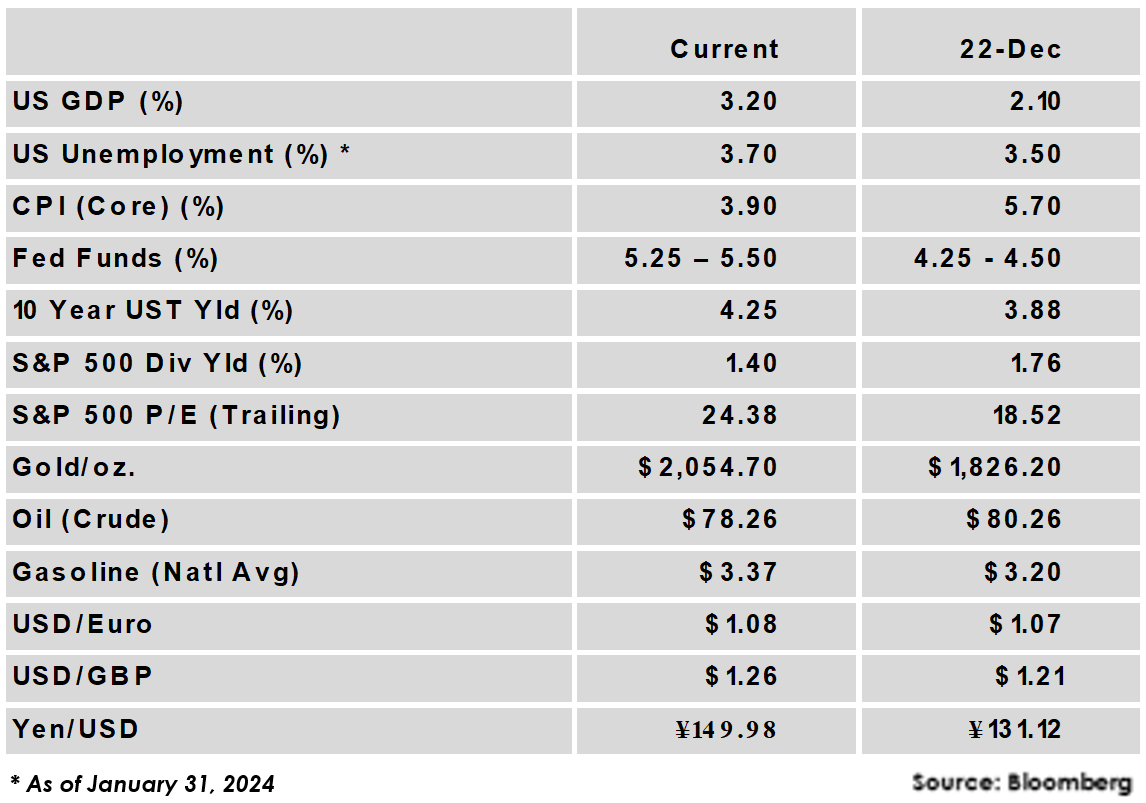

- US Job growth was stronger than expected in January, with 353,000 jobs added vs. 185,000 expected, and the unemployment rate held steady at 3.7%.

- Consumer spending fell 0.1% when adjusted for inflation, the first decline since August 2023.

- Measures of economic activity in the Eurozone improved and suggested the economy there was on a path to recovery, although results remain uneven across countries. Germany in particular continues to lag as its manufacturing sector fell farther into contraction.

- Financial markets were dealt a mixed-bag of economic news in February, all of which was largely overshadowed by robust earnings reports out of big-tech that propelled equity markets higher and maintained enthusiasm around artificial intelligence.

Global Equity

-

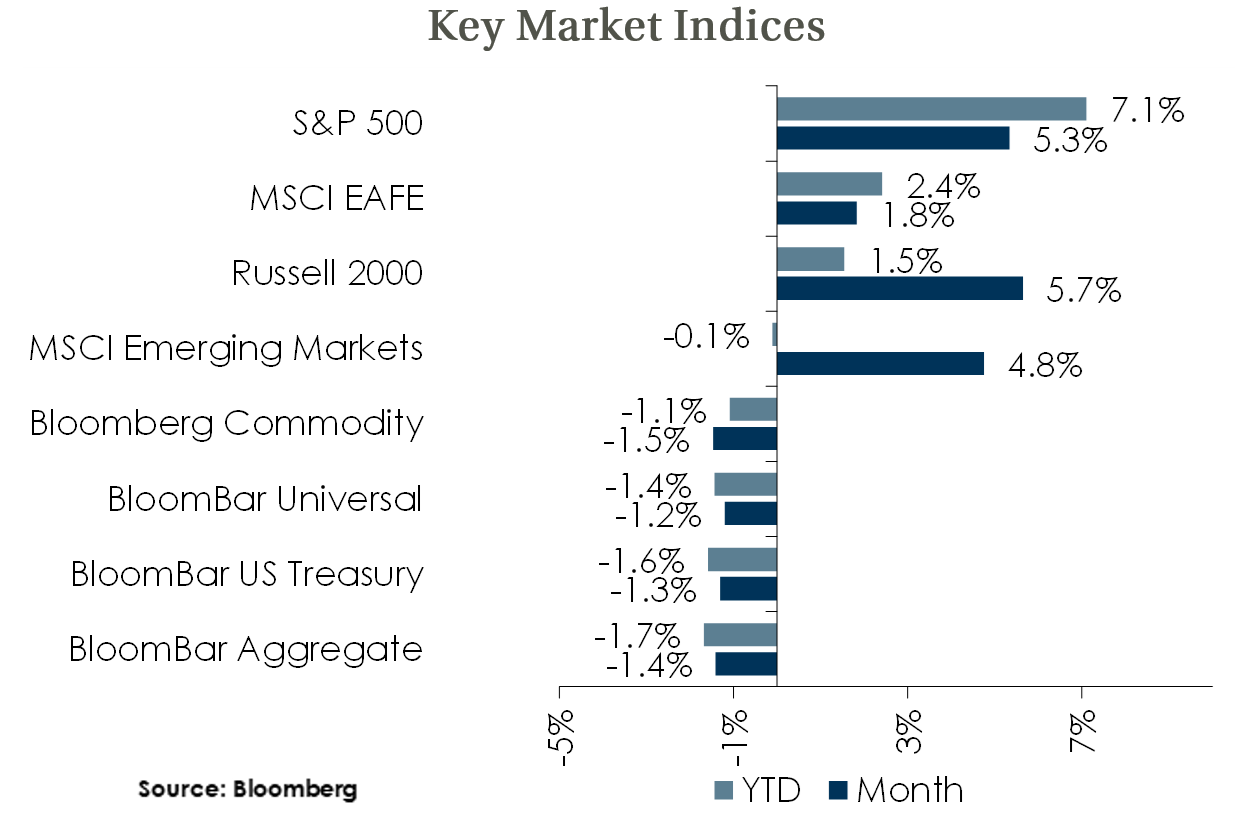

- Equity markets were positive in February with US equities leading non-US. US Small Caps outperformed as the Russell 2000 hit a new one year high.

- Strong earnings from technology companies boosted equity market sentiment overall and lifted stocks globally, with the Japanese Nikkei index hitting a new high for the first time since 1989. In a shift, China equity performance supported overall emerging markets results with a return over 8%.

- Falling inflation and impending central bank policy easing created a favorable backdrop for equities. The US large cap rally may persist while earnings growth looks robust, but stretched valuations leave a thin margin for error and tilts risks towards the downside.

- Equity markets were positive in February with US equities leading non-US. US Small Caps outperformed as the Russell 2000 hit a new one year high.

Global Fixed Income

-

- Bond yields rose across the curve in February, with the 10-year US treasury yield moving 34 bps higher to 4.25%.

- Market expectations for a rate cut have been cooled by recent inflation results, strong jobs data, and Fed minutes which show FOMC members are concerned with cutting rates too soon. Market pricing now indicates June for a first rate cut vs. expectations at the beginning of the year for a March cut.

- Credit spreads were mixed in the month with investment grade credit spreads unchanged and high yield 32 bps tighter. Both measures are near the bottom of their historic ranges, but all-in yields remain attractive and could help weather potential economic deterioration.

- Bond yields rose across the curve in February, with the 10-year US treasury yield moving 34 bps higher to 4.25%.

Global Real Estate

-

- Core real estate performance was negative for a 5th straight quarter to end 2023, with property values declining for a 6th straight quarter. The office sector had by far the worst returns in the quarter, but all sectors were negative with the exception of hotels, which constitutes a very small part of the index.

- Cap rates have risen across property types but can likely rise further as they remain low relative to bond yields. Office continues to be the most troubled sector and the full effect of post-pandemic work arrangements will continue to play out as office leases come up for renewal.

- Core real estate performance was negative for a 5th straight quarter to end 2023, with property values declining for a 6th straight quarter. The office sector had by far the worst returns in the quarter, but all sectors were negative with the exception of hotels, which constitutes a very small part of the index.

|

|

Disclosures and Legal Notice | © 2024 Asset Consulting Group. All Rights Reserved.