Monthly Market Update | February 2023

February 2023

Monthly Market Update

Macro Update

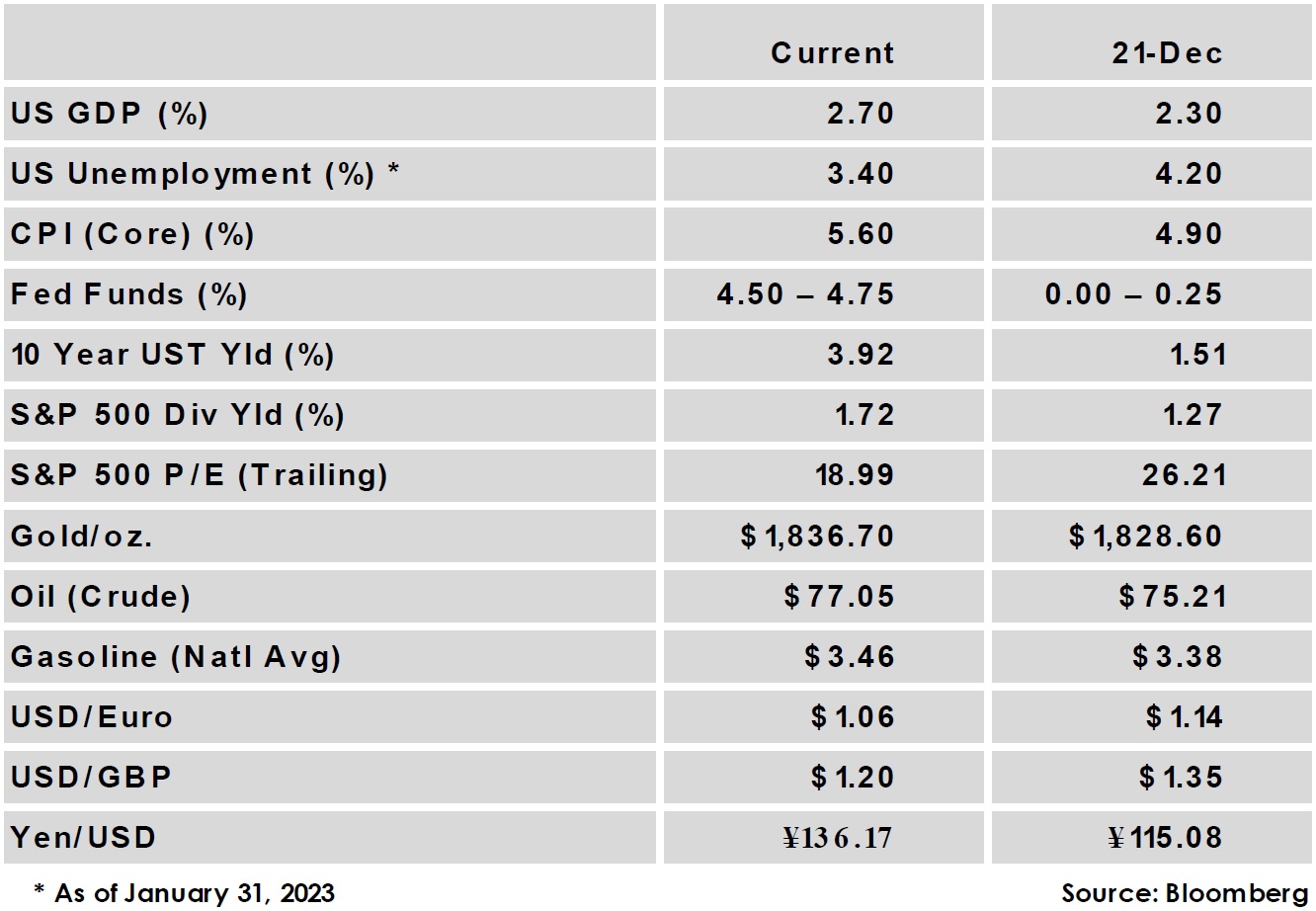

- The US Federal Reserve made a widely expected hike of 25 bps in early February, slowing the pace of tightening from the prior hike of 50 bps.

- January CPI surprised to the upside with a headline rate of 6.4% vs. an expected rate of 6.2%.

- Economic activity as seen through Purchasing Managers Indices improved, with global services and manufacturing activity both rising. For most countries, including the US, manufacturing remains in a moderate decline while the services sector is expanding.

- The US unemployment rate fell to 3.4%, the lowest level since 1969, after surprisingly strong jobs data saw payrolls increase 517,000 vs. estimates of 188,000.

Global Equity

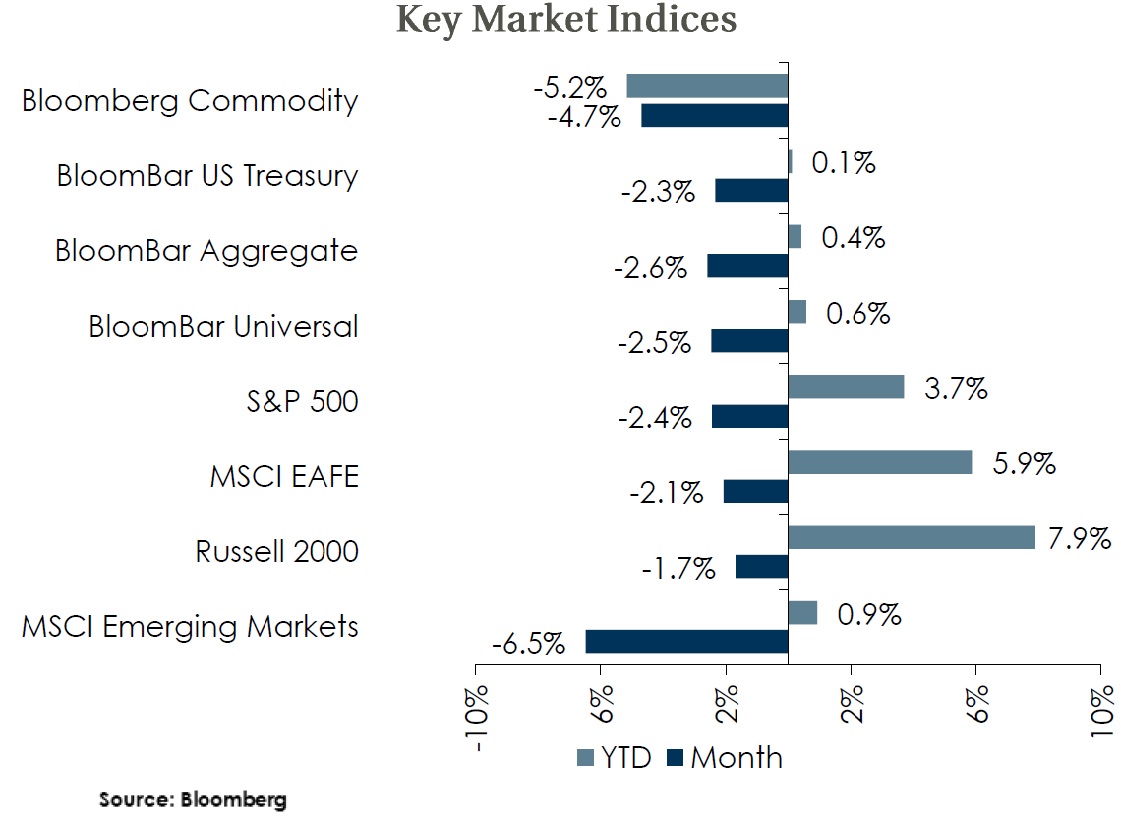

- Market sentiment was driven by the expectation of further interest rate hikes from the Fed, as hawkish Fed messaging and higher than expected January inflation impaired the outlook for risk assets and sent all broad equity indices negative for the month.

- Emerging market performance lagged this month while US Small Caps were the leader. The US dollar halted its recent downward trend, though the Non-US Developed index still narrowly outperformed US Large Caps for the month.

- Valuations on forward earnings narrowly improved or were flat, as negative performance was offset somewhat by lower forward earnings. Forward earnings projections have weakened in recent months across indices, and Non-US Developed currently exhibits the strongest recent trend.

Global Fixed Income

- Hawkish Fed messaging suggesting higher rates for longer sent US treasury yields to 3.92%, a 41 bps increase and the highest point since November.

- Credit spreads were mixed in the month as high yield widened intra-month but finished slightly tighter, while IG spreads are narrowly wider. Both measures now sit below average, but strong fundamentals should help credit weather a slowing economy.

- Sovereign yields were generally higher across the globe, as the ECB and Bank of England both hiked 50 bps in the month.

Global Real Estate

- Core real estate returns continued to decline, turning negative in the 4th quarter for the first time since 2Q 2020.

- Real estate returns could continue to be challenged as higher interest rates put upward pressure on cap rates, which currently sit near historic lows.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.