Monthly Market Update | December 2025

December 2025

Monthly Market Update

Macro Update

-

-

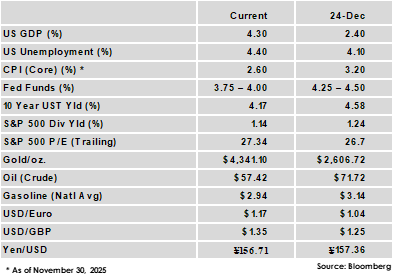

The long-delayed initial estimate of 3rd quarter US GDP growth showed the US economy expanded at an annualized rate of 4.3% vs. a 3.2% consensus forecast. This was the fastest pace in two years, following 3.8% growth in the 2nd quarter and a 0.6% contraction in the 1st quarter.

-

The FOMC approved a 3rd rate cut of 2025 in December, lowering the Federal Funds rate target range to 3.50% - 3.75%. The committee vote was 9-3 with both hawkish and dovish dissents, while the committee’s closely watched “dot plot” of individual officials’ rate expectations indicated just one cut in 2026.

-

The US unemployment rate rose to 4.6% in November, the highest rate since September 2021. The shutdown-affected labor report combined November and October results, showing a decline in job creation for October followed by modest gains in November.

-

Consumer prices rose at a 2.7% yearly rate last month, a decline from September’s 3.0% rate. The rate was well below expectations, however the government shutdown limited data collection, potentially impacting the reliability of the results.

-

Global Equity

-

-

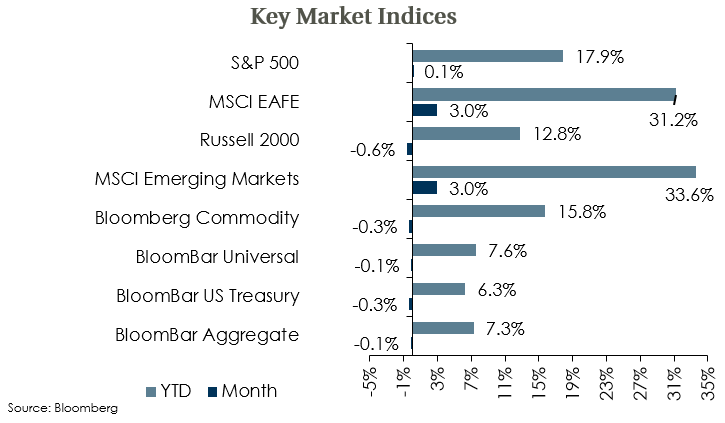

Global equities were mixed in December with non-US equities positive, US large caps roughly flat, and US small caps down.

-

Optimism around the AI theme continues to support equity markets. US technology giants have largely been the beneficiaries, but performance has broadened across a wider range of companies, sectors, and regions.

-

Equity valuations are elevated by historical standards, particularly for US large caps. Expectations are for solid earnings growth in 2026, but valuation levels suggest strong growth results are already priced into markets, potentially limiting the scope for further gains.

-

Global Fixed Income

-

-

US treasury yields were mixed in December with a steeper yield curve. Short-term rates fell as the Fed delivered another rate cut and announced $40 billion in treasury bill purchases, while longer-term rates rose as investors weighed the economic outlook and prospects for further rate cutting in 2026.

-

The Bank of England made its 4th policy rate cut of 2025 in December, reducing its rate 25 bps to 3.75%. As with the Fed, economists expect only 1-2 additional cuts from the Bank of England in 2026, and the next 12 months is expected to be a slower year overall for rate changes from key global central banks.

-

Credit spreads ended the month slightly lower, and both high yield and investment grade credit spreads are near historically tight levels. Cash yields look set to fall if rate cuts continue as expected, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate returns were positive for a 5th consecutive quarter. Returns were broad-based as all property sectors were positive, however returns remain largely income based as property price appreciation was again flat.

-

Property transaction volume has improved and the office sector appears to have passed through its trough. Economic uncertainty around tariffs and job growth could impact dealmaking, but additional rate cutting in 2026 would be a positive for the real estate sector.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.