Monthly Market Update | December 2023

December 2023

Monthly Market Update

Macro Update

-

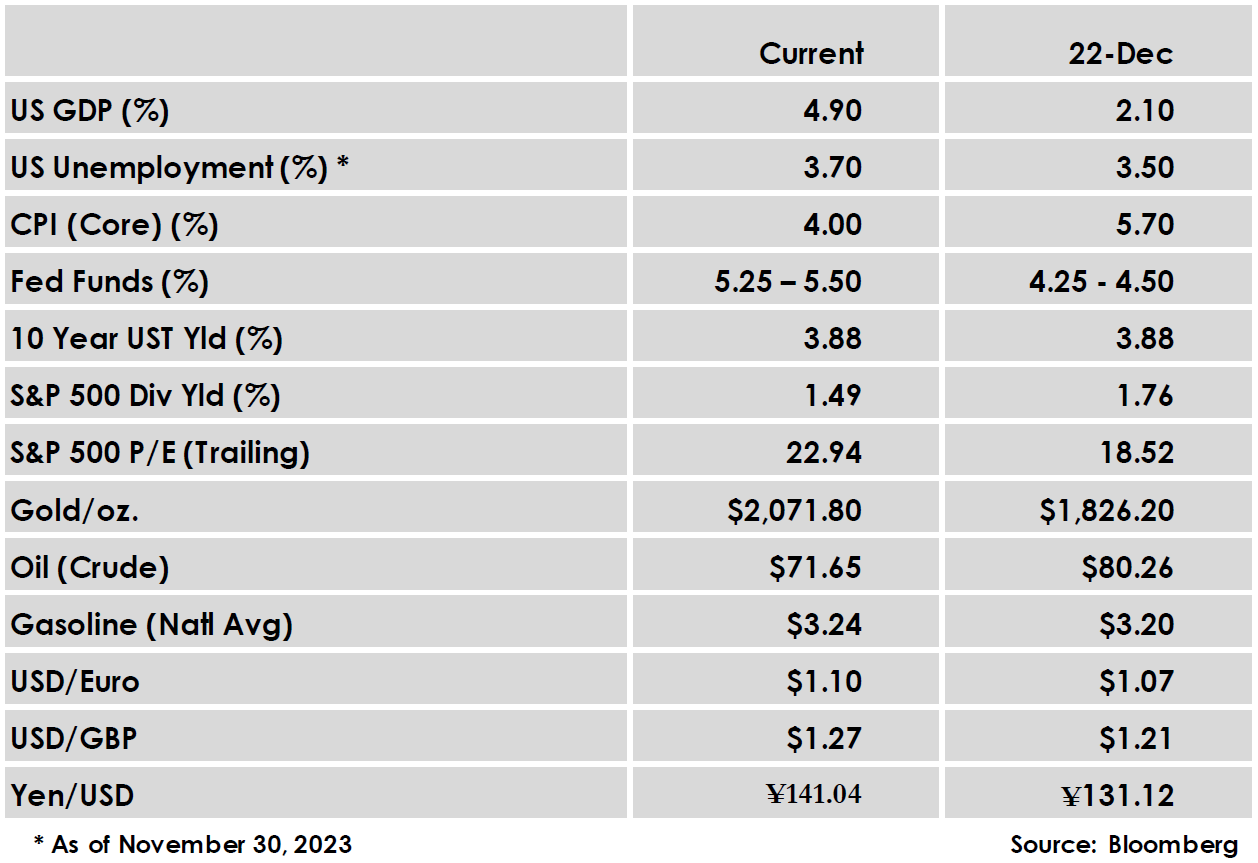

- The US Fed held its benchmark rate steady in December and provided updated projections that drove optimism around the pace of 2024 rate cuts. Declining interest rate expectations fueled a rally in asset prices for a second consecutive month, and stocks and bonds both ended the year on a winning streak.

- The US labor market continued its resilience with payroll growth exceeding expectations and unemployment declining from 3.9% to 3.7%. Wages grew 4% from a year ago, in line with expectations. While the jobs report was positive, it was still consistent with moderating growth and inflation.

- Headline CPI rose 0.1% in November and 3.1% for the trailing one year, in line with expectations and modestly down from the prior month’s 3.2% gain.

- The Eurozone economy failed to gather any momentum to end the year as factory activity there declined for an 18th consecutive month.

- China’s President Xi Jinping acknowledged “headwinds” facing that country’s economy in his annual year-end message, a rare admission of weakness as China continues to face issues such as a prolonged property downturn and high youth unemployment.

- The US Fed held its benchmark rate steady in December and provided updated projections that drove optimism around the pace of 2024 rate cuts. Declining interest rate expectations fueled a rally in asset prices for a second consecutive month, and stocks and bonds both ended the year on a winning streak.

Global Equity

-

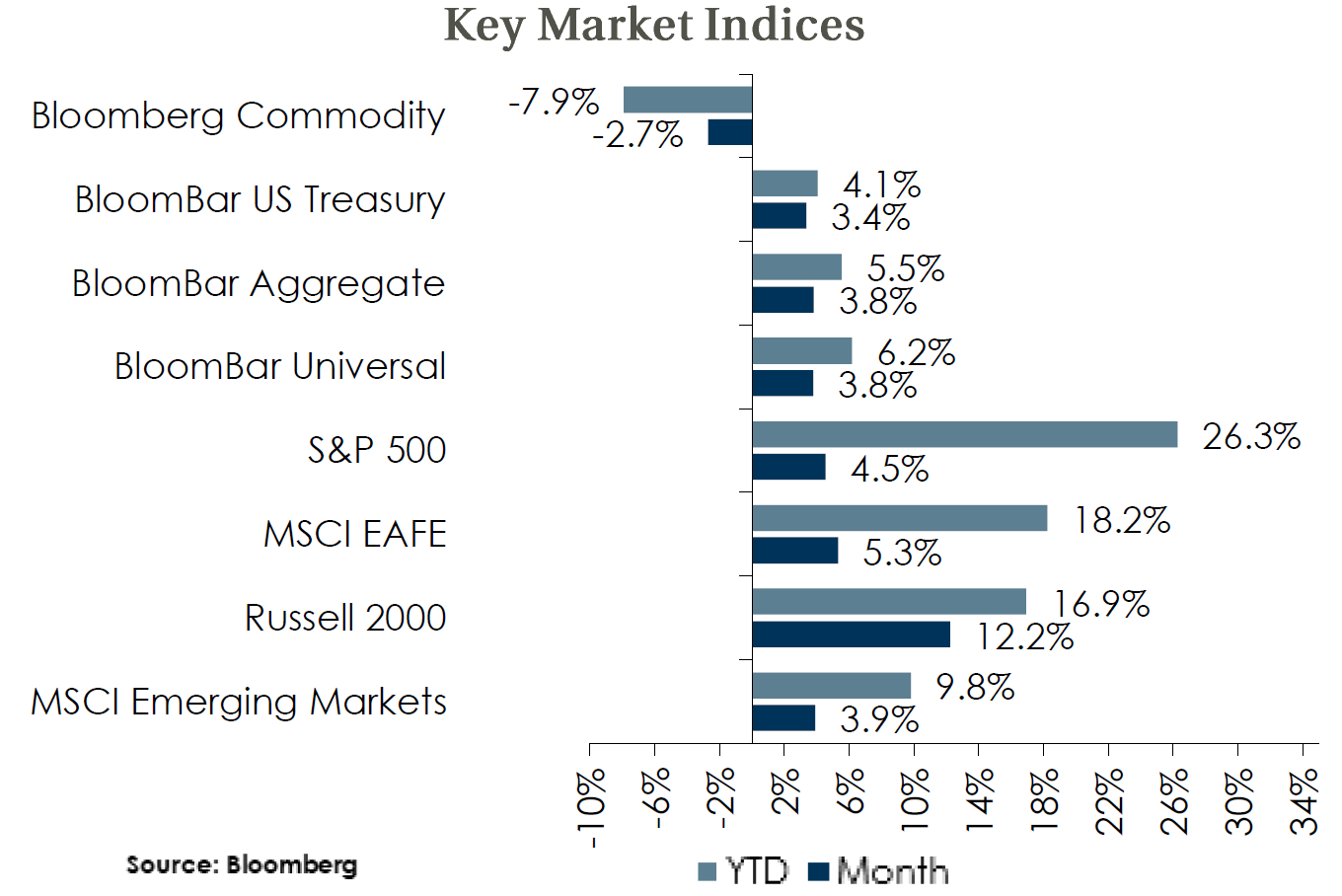

- Equity markets continued to be heavily influenced by interest rate expectations, and the outlook for lower rates sustained a rally for a second month.

- Small caps, generally more rate-sensitive, were clear outperformers in the month while emerging markets lagged due to China’s disappointing performance.

- Valuations on forward earnings rose in the last two months of the year and now sit near their historic average, except US Large Caps which are well above.

- Equity pricing is discounting a soft landing and relatively brisk pace of cuts from the Fed, with the futures market currently projecting six rate cuts in 2024 vs. Fed guidance for three cuts. Potential disappointment over the path of rates will be a key risk to equity prices in 2024.

- Equity markets continued to be heavily influenced by interest rate expectations, and the outlook for lower rates sustained a rally for a second month.

Global Fixed Income

-

- Shifting expectations for Fed rate cuts helped push treasury yields downward, and the 10-year yield fell 45 bps in December to 3.88%. Most of the yield curve fell a similar amount, but very short yields (6-mo and shorter) were relatively unchanged and still yield well over 5%.

- Non-US sovereign yields also declined in December as most other central banks have begun to pivot policy, including rate-pauses from the ECB and BofE.

- Credit spreads narrowed in December, with investment grade falling 5 bps and high yield falling 47 bps. Both measures are near the bottom of their historic ranges, but all-in yields remain attractive and could help weather potential economic deterioration.

- Shifting expectations for Fed rate cuts helped push treasury yields downward, and the 10-year yield fell 45 bps in December to 3.88%. Most of the yield curve fell a similar amount, but very short yields (6-mo and shorter) were relatively unchanged and still yield well over 5%.

Global Real Estate

-

- Core real estate returns delivered a fourth consecutive quarter of negative returns in Q3. The office sector continues to be by far the worst performer, as the space suffers from work-at-home trends.

- While cap rates have risen from recent lows, real estate returns could continue to be challenged amid higher interest rates, tighter lending conditions, and reduced demand for office space.

- Core real estate returns delivered a fourth consecutive quarter of negative returns in Q3. The office sector continues to be by far the worst performer, as the space suffers from work-at-home trends.

|

|

Disclosures and Legal Notice | © 2023 Asset Consulting Group. All Rights Reserved.