Monthly Market Update | August 2025

August 2025

Monthly Market Update

Macro Update

-

-

Market sentiment was broadly positive in August as momentum for policy easing built in the US and the trade policy outlook stabilized.

-

Fed Chairman Powell’s speech at the annual Jackson Hole symposium was viewed as dovish by markets and cemented expectations for a September rate cut.

-

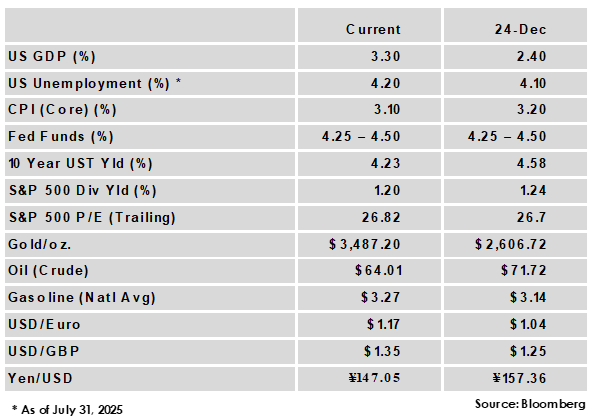

Job growth for July totaled a disappointing 73,000 while unemployment rose to 4.2%. In a further sign of labor market weakness, growth from the prior two months was revised down by 258,000 from previously-announced levels.

-

Inflation continued to edge higher, with core CPI rising from 2.9% to 3.1% and Core PCE from 2.8% to 2.9%. Inflation increases have been relatively benign so far in light of the sharp rise in tariffs, and are not generally viewed as severe enough to prevent a potential September rate cut from the Fed.

-

Higher ‘reciprocal’ tariff rates came into effect on August 7th for countries that had not yet reached a trade deal with the US, and later in the month the US imposed a 50% rate on India in retaliation for Russian oil purchases. The trade truce with China was also extended another 90 days.

-

Global Equity

-

-

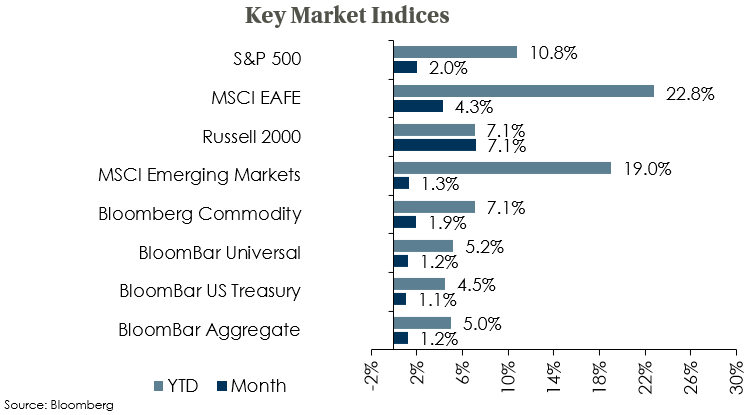

Equities were positive in August following a robust earnings season. US small caps led as the outlook for lower rates provided a boost, while a weaker US dollar helped non-US equity performance.

-

With 2nd quarter earnings season nearly complete, S&P 500 companies have reported a year-over-year growth rate of 11.9%, with 81% of companies reporting a positive earnings surprise. Equity valuations were mostly lower in the month given strong earnings results, but US large caps remain expensive relative to history.

-

The ultimate economic impact of the new global trade regime remains difficult to predict, an environment that reinforces the case for global diversification.

-

Global Fixed Income

-

-

US treasury yields mostly declined in August amid a weaker jobs report and growing expectations of a September rate cut. The yield curve has had a bias towards steepening in recent weeks as the short-end fell on higher odds of a cut while inflation risks keep long-end rates higher.

-

Central bank independence remained in the spotlight as the president attempted to fire Lisa Cook, one of the seven members of the Fed’s board of governors. Overall market response was fairly muted but long-end rates rose somewhat following the news, contributing to curve steepening.

-

IG credit spreads widened slightly as HY yield spreads tightened, and while spreads remain near all-time lows, total income remains attractive. Cash yields look set to fall with high odds of a September rate cut, while absolute return strategies often benefit from volatility and can offer downside protection.

-

Global Real Estate

-

-

Core real estate delivered another quarter of positive returns, however the return was comprised almost entirely of income as price appreciation was flat. All property sectors gained for the second consecutive quarter.

-

Commercial real estate seems to have stabilized overall even as office vacancy rates remain elevated. A resumption of Fed rate cutting could act as a catalyst for transaction volume and price appreciation.

-

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.