Monthly Market Update | April 2026

April 2026

Monthly Market Update

Macro Update

-

-

A Mideast ceasefire continues to hold even as the Straight of Hormuz remains closed, leading to a sense of cautious optimism in financial markets. Downside risks from the conflict have largely been priced out as investors anticipate a diplomatic resolution and focus on the still-healthy growth and earnings outlook.

-

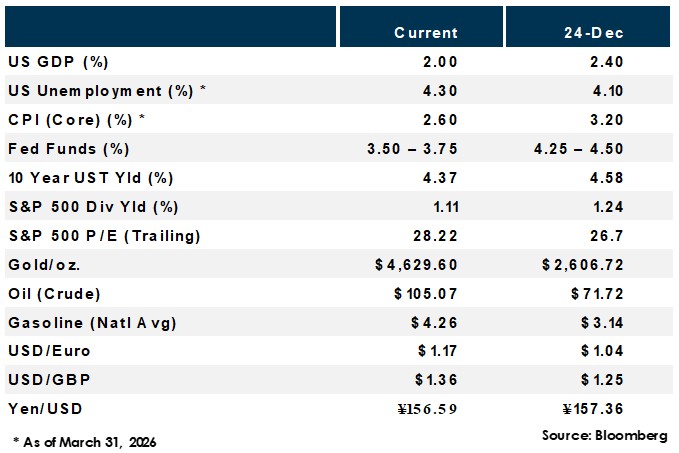

First quarter US GDP growth came in at 2.0% annualized, rebounding from Q4 2025's revised 0.5% rate. Growth was boosted by AI-driven investment and a recovery from the prior quarter's government shutdown. Consumer spending remained supportive but slowed from the prior quarter’s level.

-

The US Fed held rates steady for a third consecutive meeting, with the highest level of dissent since 1992. The meeting was likely Jerome Powell's last as chair, with Kevin Warsh expected to be confirmed as his successor. Market-based expectations continue to price no cuts for the remainder of 2026.

-

The unemployment rate fell to 4.3% in March as nonfarm payrolls surged by 178,000 jobs, well above the consensus estimate of 65,000 and representing a strong rebound from February’s downwardly revised decline of 133,000.

-

Inflation surged to a two-year high as headline CPI rose 3.3% year over year in March, up sharply from 2.4% in February. Higher energy and goods costs tied to the Iran conflict drove the jump.

-

Global Equity

-

-

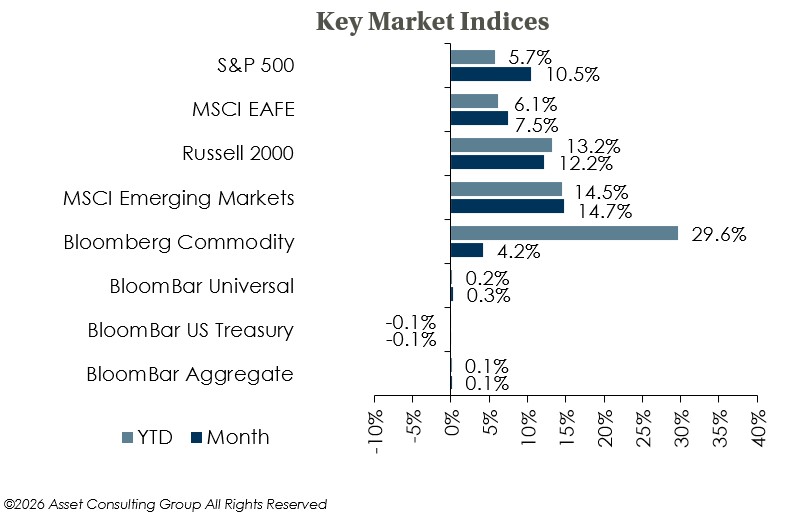

Broad equity indices regained ground lost since the start of the Iran war, with the S&P 500 hitting new record highs in April. Emerging market equities, US small caps and US large caps all enjoyed double digit returns while international developed lagged given lower AI exposure and oil supply concerns.

-

Earnings growth has helped propel the equity rally even as oil prices remain elevated, and forward earnings projections have trended higher across indices.

-

Equity valuations remain elevated, particularly for US large caps, but AI-driven earnings growth continues to support multiples. The key risk remains a reescalation of the Iran conflict that sustains energy price pressures and weighs on corporate margins.

-

Global Fixed Income

-

-

US treasury yields ended the month higher as inflation pressure from oil prices and the Fed’s hawkish hold kept rate expectations elevated.

-

Several key global central banks held meetings in April, with the European Central Bank, Bank of Japan, and Bank of England all matching the US Fed’s rate hold. The BoJ had several dissenters calling for a hike, while the ECB and BoE also signaled the potential for hikes this year as energy prices threaten inflation.

-

Credit spreads were lower following the Iran ceasefire and remain at historically low levels overall given solid credit fundamentals and positive growth outlook. Cash yields look likely to maintain current levels near-term, and absolute return strategies remain attractive as alternatives to duration-heavy portfolios.

-

Global Real Estate

-

-

Core real estate returns stayed consistent in early 2026, with returns continuing to be primarily income-based as appreciation remains flat. The office sector's stabilization from its trough continued as it performed in-line with the broader index.

-

The elimination of near-term rate cut expectations represents a headwind for the sector, as higher-for-longer financing costs weigh on valuations.

-

|

|

Disclosures and Legal Notice | © 2026 Asset Consulting Group. All Rights Reserved.