Monthly Market Update | April 2025

April 2025

Monthly Market Update

Macro Update

-

- Trump’s early month “Liberation Day” announcement stunned global markets, pressuring equities and causing significant volatility. The announced tariffs were far larger than expected, with a baseline 10% tariff applied to most countries along with additional “reciprocal” tariffs to countries with large US trade deficits.

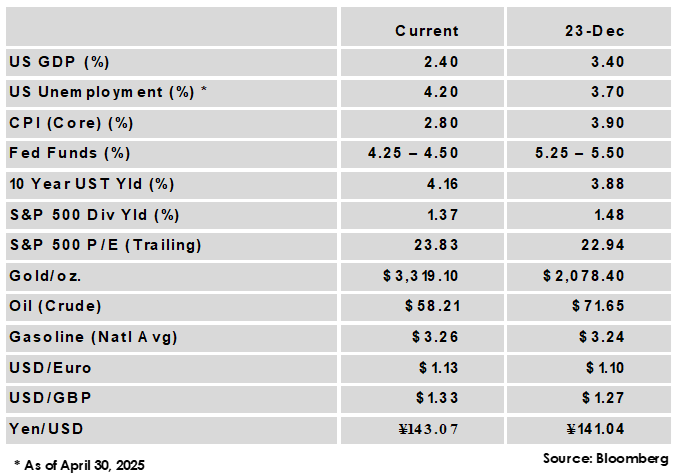

- First quarter US GDP growth fell at a 0.3% annualized pace, largely due to a surge in imports as companies sought to make purchases ahead of tariffs. The contribution to GDP from consumer spending growth remained positive but slowed relative to recent quarters.

- Job creation was robust in March with an increase in payrolls of 228,000 vs. a forecast of 140,000. However the unemployment rate ticked higher from 4.1% to 4.2% as labor force participation increased.

- Inflation cooled in March as core CPI fell from 3.1% to 2.8%, its lowest level in four years, while core PCE slowed to 2.6% from an upwardly revised 3.0% in February.

Global Equity

-

-

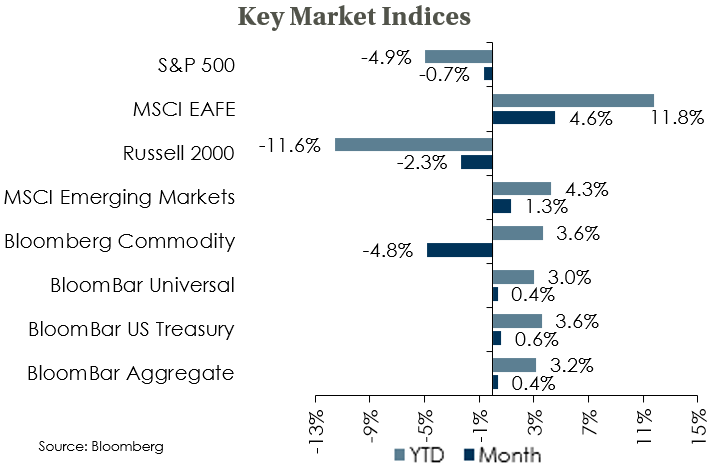

Equity performance was mixed in April as US equities continued to lag non-US markets. Dollar weakness persisted in the month, adding nearly 5% to MSCI EAFE returns for US investors. Despite the lagging performance in recent months, valuations on US large caps are still expensive from a historical perspective.

- With earnings season underway, a majority of S&P 500 companies have beaten estimates so far. However, forward guidance is trending weaker as companies begin to assess the potential impact of tariffs, and forecast downgrades are likely to weigh on equities in the near term.

- Trade uncertainty looks likely to continue as an equity headwind and is becoming a drag on global growth. US growth is still forecast to outpace developed market peers in 2025, but with US forecasts declining and anticipated policy easing in Europe, that gap looks set to narrow.

-

Global Fixed Income

-

- The US treasury yield curve steepened with a high degree of intramonth rate volatility. The 10-year yield peaked at 4.59% before ending the month 5 bps lower at 4.16%, with the volatility variously blamed on a combination of overseas selling, the unwinding of hedge fund trades, or a reduced status as a safe haven.

- Non-US sovereign yields were mostly lower in April as the uncertain global macro backdrop drove a flight to safe haven assets outside of the US. The European Central Bank cut its benchmark rate while other key central banks took a pause as they assess the impact of tariffs to the economy and inflation.

- Credit spreads rose following the tariff announcement before declining later in the month but ended moderately higher. Spreads remain low relative to history but total income remains attractive, while absolute return strategies often benefit from volatility and can offer downside protection in an uncertain environment.

Global Real Estate

-

- Core real estate returns maintained momentum with a 3rd consecutive quarter of positive returns. All property sectors gained in the quarter as even the much-maligned office sector produced a positive return.

- Trade policy uncertainty could slow the commercial real estate market as companies potentially put investment and leasing decisions on hold. Potentially higher construction costs raise risks for new developments, but the supply constraint would support valuations on existing properties.

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.