Monthly Market Update | April 2024

April 2024

Monthly Market Update

Macro Update

-

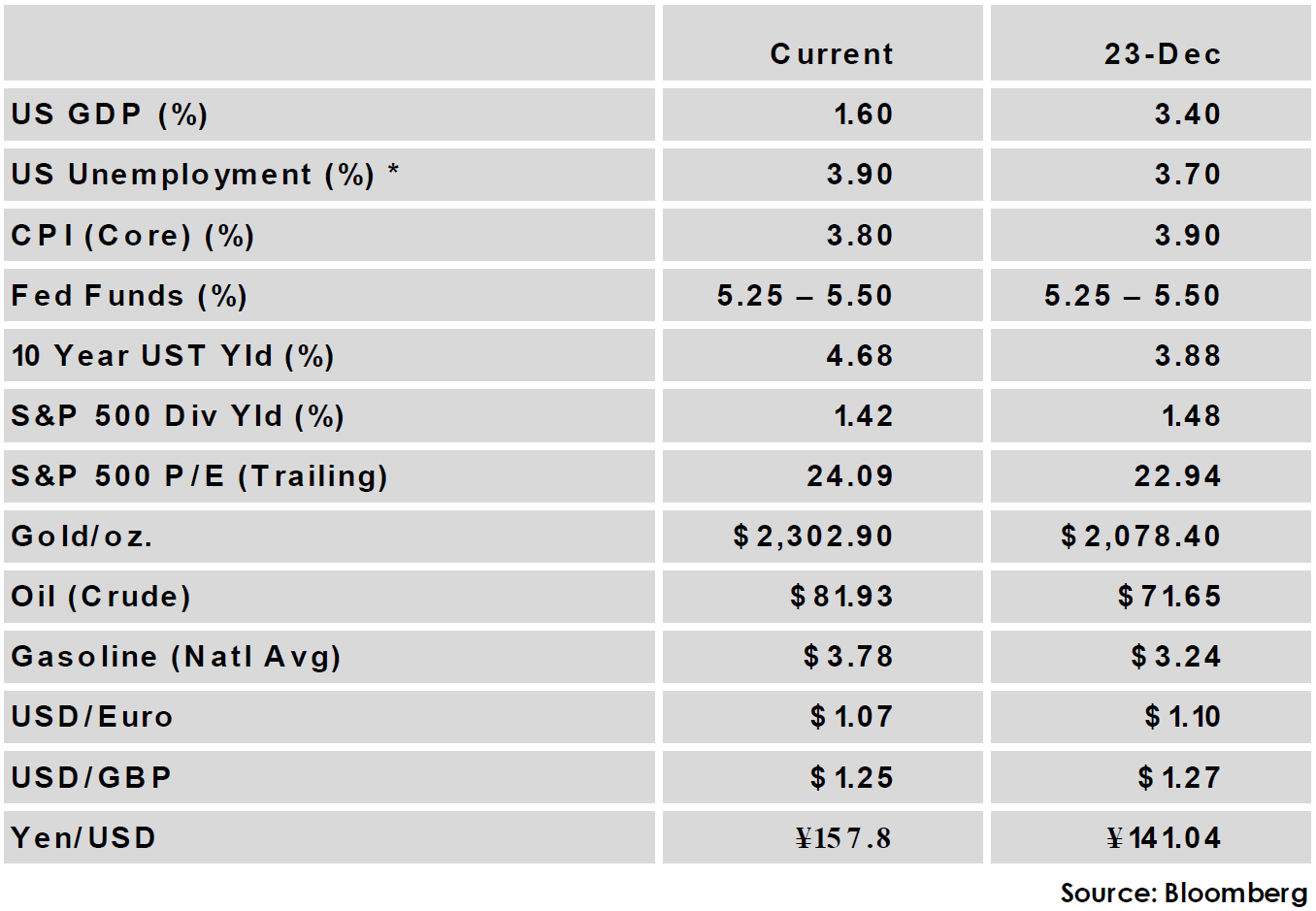

- US real GDP rose 1.6% annualized in the first quarter, well below the consensus forecast of 2.5%. Beneath the surface of the report were reasons for optimism: consumer spending (particularly in services) continued to be strong. A decline in inventories and net import trade position detracted from GDP but reflected the resiliency of the US demand compared to a weaker global economy.

- Inflationary pressures persisted in April. Core CPI’s year-over-year increase remained at 3.8% with annualized headline CPI rising to 3.5% from 3.2%. Core PCE, the Fed’s preferred gauge, held at 2.8%. Wage growth, a key driver of inflation, remains strong and increased 1.2% in the first quarter, up from 0.9% last quarter.

- The April 30 – May 1 FOMC meeting resulted in a widely anticipated decision to hold interest rates at the current target range of 5.25% - 5.50%. The Federal Reserve plans to slow the pace of quantitative tightening in June by reducing the monthly redemption cap on Treasury securities from $60B to $25B.

- US real GDP rose 1.6% annualized in the first quarter, well below the consensus forecast of 2.5%. Beneath the surface of the report were reasons for optimism: consumer spending (particularly in services) continued to be strong. A decline in inventories and net import trade position detracted from GDP but reflected the resiliency of the US demand compared to a weaker global economy.

Global Equity

-

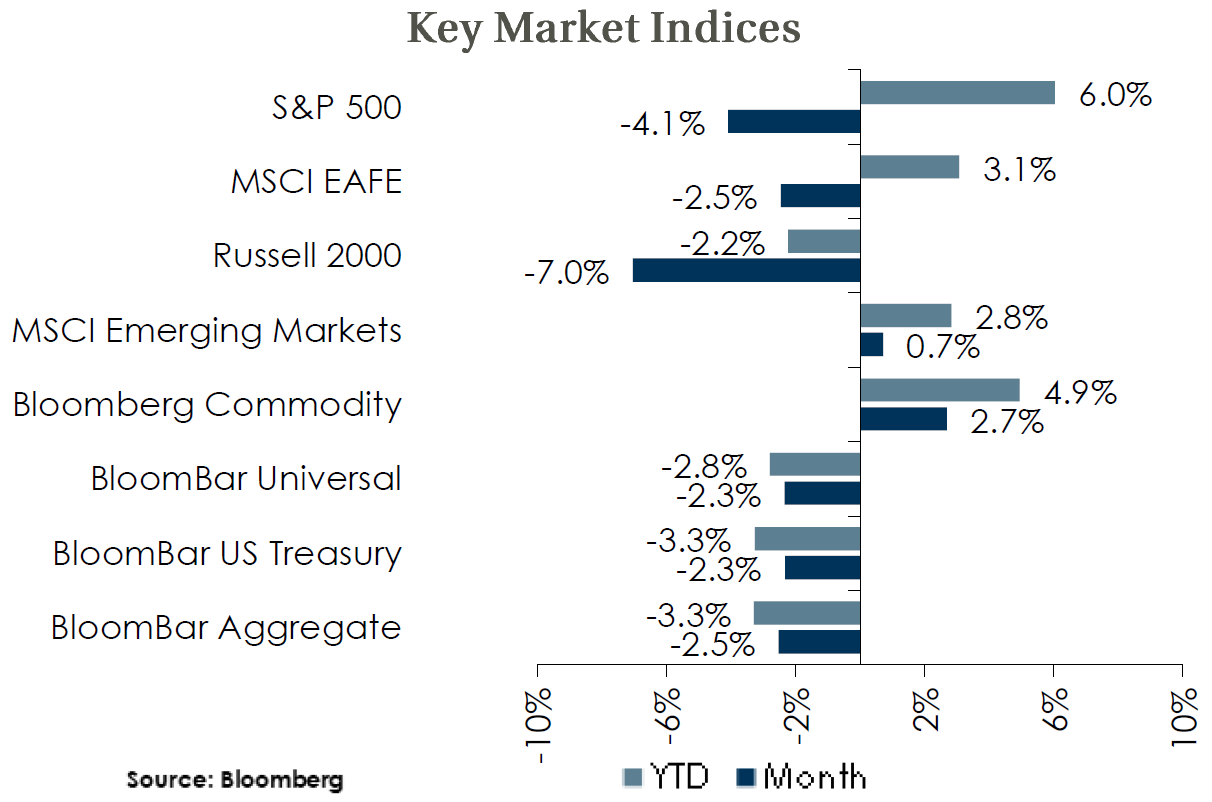

- Equity market winning streaks came to an end in April with most major indices down during the month. The exception was Emerging Markets, which was broadly supported by a positive month from China. The S&P 500 declined by 4%, its first negative month since October, reducing the YTD return to 6%.

- 10 of 11 S&P 500 sectors declined during the month, with Utilities being the lone sector to contribute a positive return.

- Rising yields and sticky inflation combined to create instability in the markets but generally strong earnings have prevented a deeper downturn. Markets seemed to react to each new data point with the VIX increasing during the month. Stretched valuations leave a thin margin for error and tilt risks towards the downside.

- Equity market winning streaks came to an end in April with most major indices down during the month. The exception was Emerging Markets, which was broadly supported by a positive month from China. The S&P 500 declined by 4%, its first negative month since October, reducing the YTD return to 6%.

Global Fixed Income

-

- US Treasury yields rose across the curve in April with many tenors touching 2024 highs intra-month. The 10-year US Treasury yield increased 48 bps to 4.68% and the 2-year US Treasury exceeded 5% for the first time since November, ending the month at 5.04%.

- Inflation results and resilient economic growth have further reduced rate cut expectations. Futures market pricing now implies only one rate cut in 2024, removing two projected cuts from forecasts this month. The European Central Bank and Bank of England appear to remain on track to start easing by mid-year.

- Strong demand for credit led to both investment grade and high yield corporate spreads finishing close to unchanged during the month. Both measures are near the bottom of their historic ranges, but the economic backdrop remains supportive of credit and all-in yields are attractive relative to recent history.

- US Treasury yields rose across the curve in April with many tenors touching 2024 highs intra-month. The 10-year US Treasury yield increased 48 bps to 4.68% and the 2-year US Treasury exceeded 5% for the first time since November, ending the month at 5.04%.

Global Real Estate

-

- Core real estate continued its losing streak with a 6th straight quarter of negative returns in 1Q. Property values were down across every property type, with Office assets once again the worst performer with -5.0% depreciation.

- Cap rates remain under upward pressure in an environment of increased and sticky bond yields. Office continues to be the most troubled sector and the full effect of post-pandemic work arrangements will continue to play out as office leases come up for renewal.

- Core real estate continued its losing streak with a 6th straight quarter of negative returns in 1Q. Property values were down across every property type, with Office assets once again the worst performer with -5.0% depreciation.

|

|

Disclosures and Legal Notice | © 2024 Asset Consulting Group. All Rights Reserved.