Monthly Market Update | November 2022

November 2022

Monthly Market Update

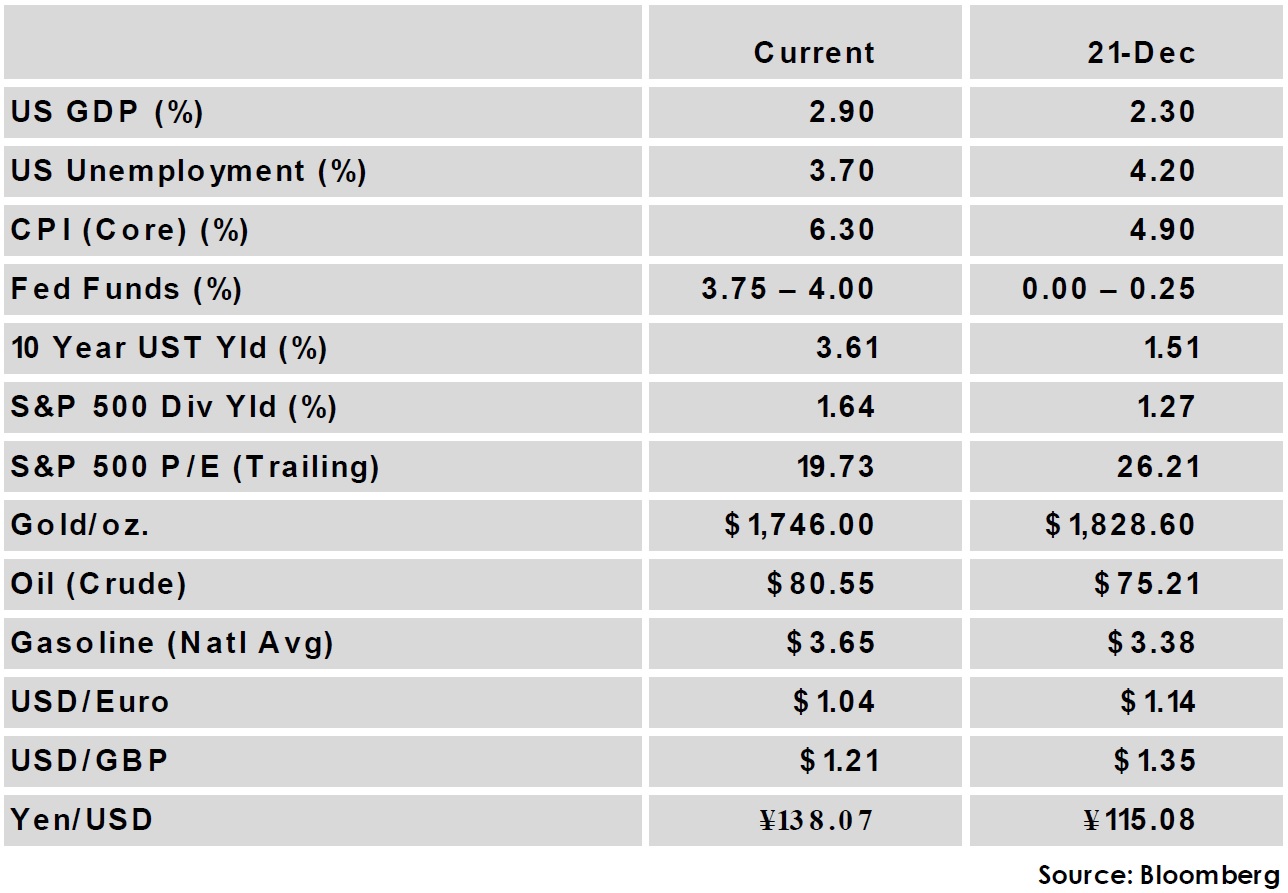

Both rates and risk assets rallied in November as investors increasingly bet that inflation was peaking and the Federal Reserve would soon slow the pace of rate hikes. The month began with another 75 bps hike from the Fed, as expected, but statement language acknowledging the lag between policy and economic impact seemed to open the door for a slower pace of increases. Inflation data lent further support to the notion, with core, headline, and producer price inflation all surprising to the downside.

Other economic data showed signs of continued strength, as US retail sales rose sharply, 3rd quarter GDP was revised higher to 2.9%, and labor market growth remained strong. Sentiment in Non-US markets improved as well, with Eurozone inflation showing signs of cooling and China taking some modest steps towards easing covid restrictions. Speculation around Fed policy will continue to play an outsized role in markets, and while expectations have shifted to a smaller 50 bps rate hike from the Fed, debate is likely to continue up until the mid-December meeting, which sees November’s CPI released just the day before.

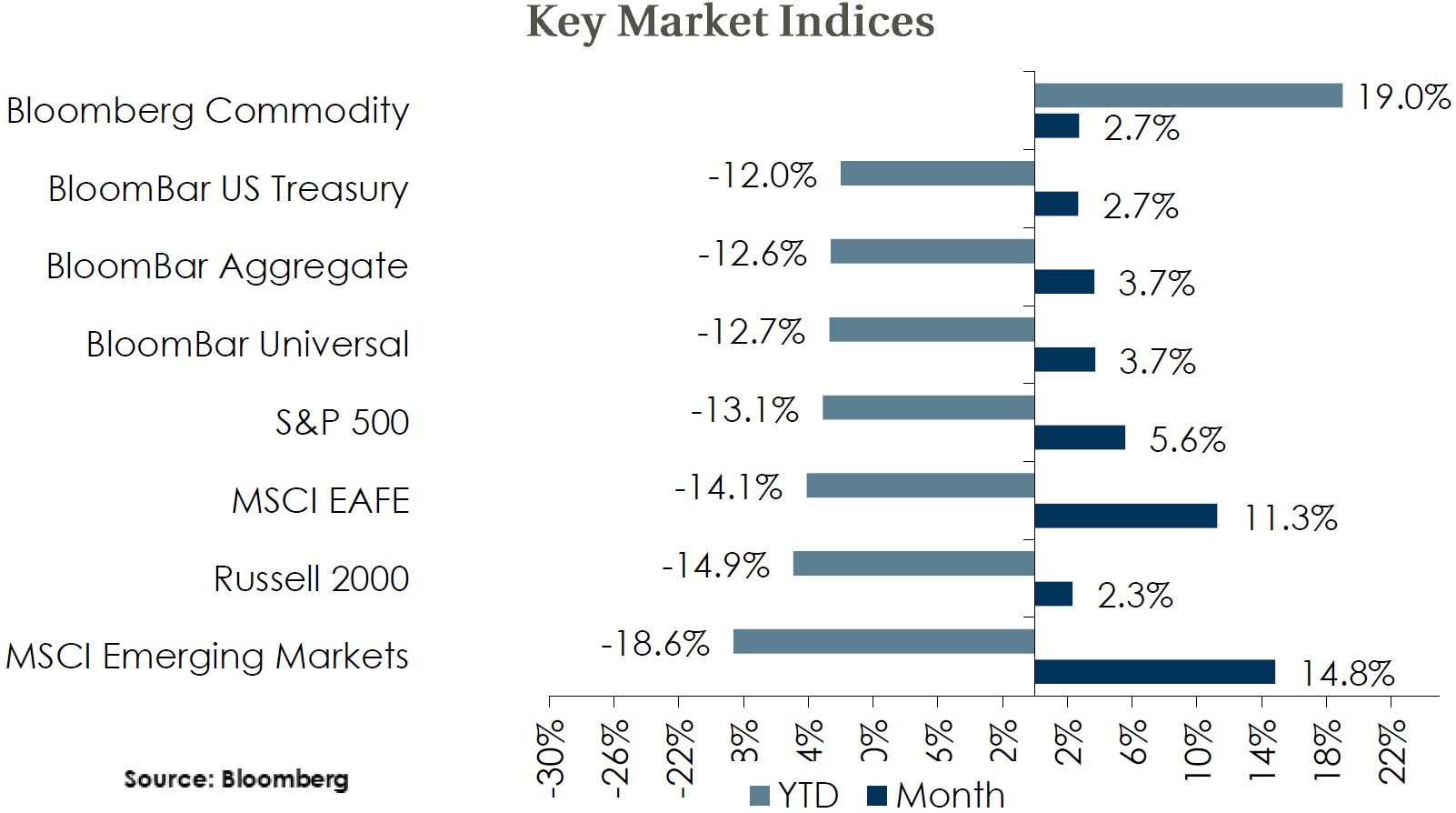

- Global Equity – Equity indices were broadly higher in November, led by emerging markets and international developed markets. Currency movements continue to play a key role in relative performance this month to the benefit of non-US stocks as the US dollar had its largest monthly fall in over a decade. Chinese stocks also rose dramatically on reopening hopes and additional support for the property sector even as citizens there protested lockdowns. Equity market volatility is likely to continue given central bank policy uncertainty, geopolitical conflict, and uncertainty in the Chinese market. Valuations on forward earnings have risen but still sit near neutral levels as recent positive surprises have strengthened the case for an economic soft landing. However ample risks remain both in the US and abroad, and the potential for further growth slowdown could limit near-term equity upside.

- Global Fixed Income – Global bond yields were lower in November amid signs of peaking inflation and slowing central bank hikes. Along with speculation of smaller hikes for the US Fed, several developed market central banks have already reduced their pace, including Australia, Canada, and Norway. Credit spreads tightened in the month with the market’s risk-on posture, as high yield moved 16 bps tighter and IG credit 25 bps tighter. The US rate rally was led by the long-end, leading to further curve inversion. The 10-year UST yield fell 44 bps, but core bond yields remain elevated relative to recent history and the current Fed policy outlook suggests a nearing peak in rates. Spreads could widen in a recession scenario but strong corporate balance sheets should soften the impact to credit of a growth slowdown. Volatility in rates and currency can provide enhanced opportunities for absolute return strategies, but credit exposure and a lower duration could hurt returns relative to cash and core bonds. A cash allocation provides portfolio flexibility while higher yields have improved the asset’s return potential.

- Global Real Assets & Private Markets – Core real estate returns cooled significantly from recent quarterly performance, but maintained a modestly positive return. In a change, Hotels replaced Industrials as the top performing sector in the quarter, and Office was the only sector with negative performance. New deal activity in private equity continues to slow from 2021’s elevated rate but overall remains at healthy levels. The broad commodities index was positive in November, helped by hopes of easing covid restrictions in China and a weaker dollar. Oil was sharply down however, as traders assessed the likelihood of additional OPEC+ cuts in their December meeting. Core CPI rose +6.3% year-over-year, below expectations and a 0.3% decline from last month. Measures of future inflation expectations were lower in the month, with the 10-year inflation breakeven down 14 bps to 2.37%.

|

|

Disclosures and Legal Notice | © 2022 Asset Consulting Group. All Rights Reserved.